Introduction

How credit cards work is confusing for many beginners, especially when interest, billing cycles, and payments aren’t clearly explained. Swipe it, walk away with something new, and worry about paying later. But that simplicity hides a system that confuses millions of people every year—and costs those who don’t understand it thousands of dollars in unnecessary interest and fees.

The truth is, credit cards aren’t magic. They’re tools. And like any tool, they work best when you understand how they’re built and what they’re actually doing. Understanding how credit cards work before using one helps beginners avoid interest charges, late fees, and long‑term debt.

This guide explains how credit cards work from the moment you swipe to the moment you pay—and everything the card company does in between. We’ll skip the jargon and focus on what actually matters: how to use a credit card responsibly, avoid expensive mistakes, and build credit without going into debt. At UncoverCards, we focus on helping beginners, freelancers, and gig workers understand credit cards and build credit the right way.

On This Page

- Introduction

- What a Credit Card Is (In Simple Terms)

- How Credit Cards Work During a Transaction

- The Credit Card Billing Cycle Explained

- Statement Balance vs. Current Balance

- How Credit Card Interest Works

- Minimum Payment: What It Is and Why It’s Dangerous

- Credit Utilization and Why It Matters

- How Credit Cards Affect Your Credit Score

- How Credit Cards Specifically Impact Your Score

- Credit Card Rewards (Basics Only)

- Common Credit Card Fees Beginners Face

- Common Myths About Credit Cards

- Smart Rules for First-Time Credit Card Users

- Frequently Asked Questions

- Conclusion

- Disclaimer

What a Credit Card Is (In Simple Terms)

Credit vs. Debit—What’s the Real Difference?

Let’s start with the basics. When you use a debit card, you’re spending money that’s already yours. The bank transfers it directly from your account to the seller. It’s immediate, it’s gone.

A credit card works differently. When you use a credit card, you’re not spending your own money—you’re borrowing money from the card issuer (the bank that issued your card). The bank pays the merchant on your behalf. You’re taking out a short-term loan, and you’ll pay that loan back later, usually within a month. For a basic definition of how credit cards work, beginners can also refer to this consumer education resource from the Consumer Financial Protection Bureau.

Your Credit Limit: The Borrowing Boundary

When you open a credit card account, the issuer assigns you a credit limit. This is the maximum amount of money you can borrow at any time. If your limit is $1,000, you can’t spend more than $1,000 across all your purchases until you pay some of it back.

The credit limit is set based on factors like your income, credit history (if you have one), and overall financial situation. As you use your card responsibly and pay on time, that limit can increase.

Why It’s Called “Revolving” Credit

Credit cards are called “revolving” credit because the credit replenishes as you pay. Use your $1,000 limit to buy something for $300, and you now have $700 available. Pay back that $300, and your full $1,000 limit returns. You can borrow again and again within that same limit—hence “revolving.”

How Credit Cards Work During a Transaction

Every time you use your credit card, several things happen behind the scenes, usually in seconds. Understanding this process removes a lot of the mystery.

You swipe, tap, or insert your card at a merchant. The card reader captures your information and sends it to the card issuer’s system. The issuer checks: Do you have enough available credit? Is the card active? Are there any fraud flags?

If everything looks good, the issuer approves the transaction and sends a message back to the merchant: “Yes, this purchase is approved.” This is authorization.

Step 2: The Merchant Gets Paid

The issuer transfers the money to the merchant’s bank account. From the merchant’s perspective, they’ve been paid. From your perspective, you just owe the issuer.

Step 3: Posting to Your Account

The transaction is recorded in your credit card account. This happens within 1-3 business days, depending on the merchant and the card issuer. Once it posts, the amount is added to your balance—the total amount you owe.

Step 4: Pending vs. Posted

Until a transaction posts, it appears as “pending” on your account. Pending transactions count against your available credit, but they’re not yet permanent. Once they post, they’re final.

This is why you might see a charge disappear if a merchant never actually completed the transaction—it was still pending and never posted.

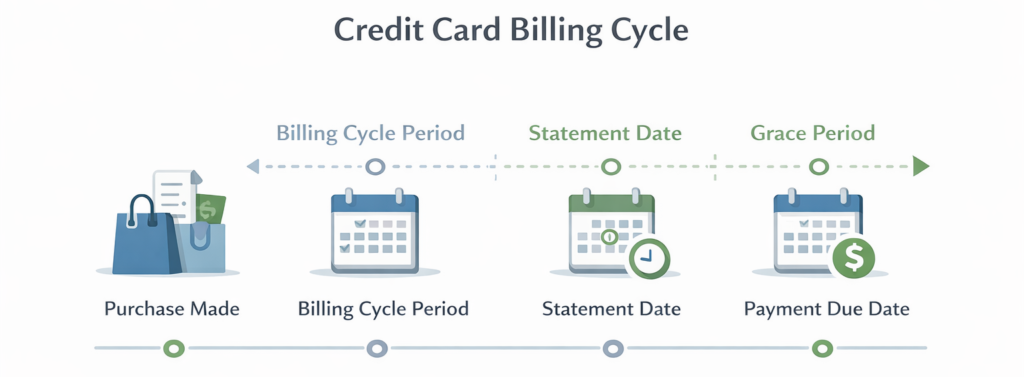

The Credit Card Billing Cycle Explained

The billing cycle is the foundation of how credit cards work, and understanding it is crucial to avoiding unnecessary interest charges. This is one of the most important parts of understanding how credit cards work in real life.

What a Billing Cycle Is

A billing cycle is a regular period—usually between 25 and 31 days—during which your card issuer tracks all your transactions. Every purchase, payment, and fee made during that period gets grouped together. At the end of the cycle, the issuer generates a statement.

Think of it like a monthly report card for your spending.

Key Dates in Your Billing Cycle

| Term | What It Means | Why It Matters |

|---|---|---|

| Statement Date | The day your billing cycle ends and your statement is generated (also called the “closing date”) | This marks the end of the period you’re being billed for. Purchases after this date roll into the next month’s statement. |

| Due Date | The last day to pay at least part of your bill without penalties | Missing this date triggers late fees and can damage your credit. |

| Grace Period | The interest-free period between your purchase and the due date (typically 15–25 days) | If you pay your full statement balance by the due date, no interest is charged on purchases. |

| Billing Cycle | The span of days between two statement dates (typically 28–31 days) | All transactions during this period appear on one statement. |

| Minimum Payment | The smallest amount you’re required to pay to keep your account in good standing | Paying only the minimum keeps you in debt much longer. |

A Real-World Example

Let’s say your billing cycle runs from the 5th to the 4th of each month.

- March 5 – April 4: Your billing cycle. Every purchase during this period appears on your April statement.

- April 4: Your statement is generated. It shows everything you spent, your total balance, your minimum payment, and your due date.

- April 24: Your payment due date (about 20 days after the statement).

- April 1–4: Purchases you make on these dates appear in your May statement, not April’s.

Once you understand the billing cycle, how credit cards work becomes much easier to manage.

Statement Balance vs. Current Balance

This is where many beginners get confused, and it’s a critical distinction.

The Difference

Your statement balance is the total amount you owe as of your last statement date. It’s the amount used to determine your interest charges and minimum payment.

Your current balance is what you owe right now, including any new purchases you’ve made since your statement was generated. New transactions haven’t been billed yet—they’ll appear on your next statement.

Why This Matters

The statement balance is what you should pay to avoid all interest charges. If you pay your full statement balance by the due date, the card issuer won’t charge you any interest, even if you use the card again after the statement closes.

This is the grace period in action: the issuer is giving you a free loan from your purchase date until your payment due date.

Common Beginner Mistakes

Many new cardholders make this mistake: they look at their current balance, see it’s small, and assume they’re only using a little credit. But if new purchases have posted since the statement, the current balance doesn’t reflect what’s coming on next month’s bill.

The safe approach: always pay at least your full statement balance by the due date.

How Credit Card Interest Works

To truly understand how credit cards work, you must understand interest.

APR in Plain Language

APR stands for Annual Percentage Rate. It’s the annual cost of borrowing money expressed as a percentage. If a card has an APR of 18%, you’d pay 18% per year in interest if you carried a $1,000 balance for the entire year. APR is a standardized way lenders express borrowing costs, and understanding it is essential to learning how credit cards work responsibly.

But interest doesn’t wait a year to be calculated—it compounds daily.

How Daily Interest is Calculated

To find the daily interest rate, the card issuer divides your APR by 365:

Daily rate = APR ÷ 365

So if your APR is 18%, your daily rate is 18% ÷ 365 = 0.0493% per day.

Each day you carry a balance, this daily rate is applied to your outstanding balance. The amount of interest you owe grows a little bit each day. This is why even a small balance can cost more than you expect over several months. This is where many beginners misunderstand how credit cards work and end up paying more than expected.

When Interest Applies—and When It Doesn’t

Interest does NOT apply if:

- You pay your full statement balance by the due date

- You have no balance carried over from the previous month

Interest DOES apply if:

- You pay less than your full statement balance

- Your payment is late

- You make a cash advance (interest usually starts immediately)

The Danger of Carrying a Balance

Let’s say you carry a $500 balance on a card with a 20% APR. If you make only minimum payments (around 2–3% of your balance), here’s what happens:

- Month 1 interest: ~$8.33

- Month 2 interest: ~$8.15 (slightly less, since you paid down a tiny bit of principal)

- …and so on

But because most of your minimum payment goes to interest and barely touches the principal, you could spend 5+ years paying off that $500 purchase. And you might pay $150 or more in interest alone—30% more than you originally spent.

That’s why the minimum payment is often called a debt trap. Interest is the main reason why learning how credit cards work early is so important.

Minimum Payment: What It Is and Why It’s Dangerous

The minimum payment is the smallest amount the card issuer requires you to pay each month to keep your account in good standing and avoid late fees. It sounds helpful. It’s not.

How Minimum Payments Are Calculated

Minimum payments are typically set at 2–3% of your total balance. On a $500 balance, that’s just $10–15. It seems manageable.

The problem is that most of that payment goes to interest, not to paying down what you actually owe. Only a tiny fraction reduces your principal—the amount you actually borrowed.

Why Paying Only the Minimum Hurts

When you pay only the minimum:

- You stay in debt for years. A $500 purchase could take 5–10 years to pay off if you only pay the minimum.

- Interest costs spiral. Over that time, you might pay $200+ in interest—potentially doubling the cost of what you bought.

- Your credit utilization stays high. Because your balance decreases so slowly, your utilization ratio (the percentage of credit you’re using) stays elevated, which hurts your credit score.

- You’re vulnerable. Carrying high debt with little progress toward paying it off leaves you with little financial flexibility if an emergency arises.

The Math: Minimum Payment vs. Full Payment

| Scenario | Monthly Payment | Time to Pay Off | Total Interest Paid |

|---|---|---|---|

| Pay Minimum Only (2.5%) | $12.50 (starting) | 36+ months | $120+ |

| Pay Fixed $50/month | $50 | 11 months | $20 |

| Pay Full Balance Each Month | Varies with spending | 1 month | $0 |

As you can see, paying just $50 instead of the minimum saves you months of payments and over $100 in interest. Paying the full balance each month eliminates interest entirely.

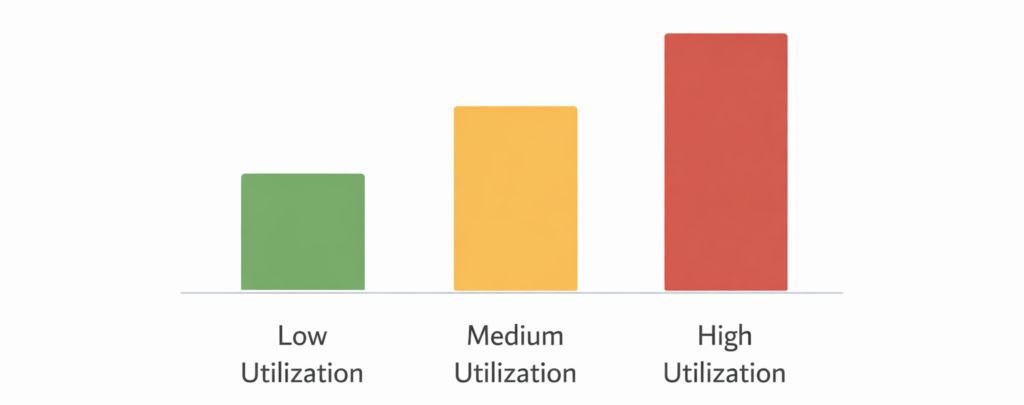

Credit Utilization and Why It Matters

Credit utilization is a metric that most beginners have never heard of, but lenders pay close attention to it. It makes up 30% of your credit score.

What Is Credit Utilization?

Credit utilization is the percentage of your available credit that you’re currently using. It’s calculated by dividing your balance by your credit limit.

Example:

- Your credit limit: $1,000

- Your current balance: $300

- Your utilization: 300 ÷ 1,000 = 30%

Why Under 30% Matters

Lenders view credit utilization as a sign of financial health. A low utilization ratio suggests you’re using credit responsibly—you borrow, but you also have plenty of available credit for emergencies. A high utilization ratio suggests you might be struggling financially or are relying too heavily on credit.

- 0–10% utilization: Excellent for your score. Shows strong financial management.

- 11–30% utilization: Good, but slightly riskier than 0–10%.

- 31–50% utilization: Okay, but may start to negatively affect your score.

- Above 50% utilization: High and significantly damaging to your score.

Why Under 10% Is Ideal

Financial experts recommend keeping your utilization below 10% for optimal credit score benefits. If your limit is $1,000, that means keeping your balance below $100.

This doesn’t mean you shouldn’t spend. It means if you spend $500, you should pay it down before your statement closes so that only a small amount appears on your statement.

How Credit Cards Affect Your Credit Score

Your credit score is a three-digit number (typically ranging from 300 to 850) that represents your creditworthiness. It’s calculated from information on your credit report, and credit cards play a major role. For self‑employed professionals, understanding how credit scores affect credit card approval for freelancers is an important part of using credit responsibly.

The Five Factors in Your Credit Score

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | Do you pay your bills on time? |

| Amounts Owed | 30% | How much credit are you using? (Utilization ratio) |

| Length of Credit History | 15% | How long have your accounts been open? |

| Credit Mix | 10% | Do you have different types of credit (cards, loans, mortgage)? |

| New Credit Inquiries | 10% | How many new accounts or credit applications recently? |

How Credit Cards Specifically Impact Your Score

Payment History (35%)

This is the most important factor. Every time you pay on time, it’s recorded. Every missed payment is also recorded and damages your score. A 30-day late payment can drop your score significantly. The further behind you fall (60 days, 90 days, or more), the worse the damage.

Amounts Owed (30%)

This is primarily your credit utilization ratio. If you use a lot of your available credit, your score drops. If you use very little, your score benefits.

Length of Credit History (15%)

The longer you’ve had a credit account open, the better. Beginners with brand-new cards have a short history, which is why their scores may fluctuate more initially.

Credit Mix (10%)

Credit bureaus like to see that you can handle different types of credit: credit cards, installment loans, mortgages, etc. As a beginner, you might only have a credit card, and that’s fine.

New Credit Inquiries (10%)

When you apply for new credit, the lender checks your credit report. Too many inquiries in a short time can lower your score slightly.

Why Beginner Scores Fluctuate

When you first get a credit card, your score might fluctuate from month to month. This is normal. You’re building credit history, so your score is adjusting as new data comes in. Once you establish a pattern of on-time payments and low utilization, your score will stabilize and improve.

Credit Card Rewards (Basics Only)

Credit card rewards exist to make spending feel rewarding. But they can also be a trap for beginners who chase rewards without understanding the fundamentals.

Cash Back vs. Points

Cash Back: You earn a percentage of every dollar spent back as actual money. Common rates are 1–2.5% cash back on all purchases. Some cards offer higher rates in specific categories (grocery stores, gas stations, restaurants).

Points or Miles: You earn points on every purchase, which you can redeem for travel, merchandise, gift cards, or other rewards.

Why Beginners Shouldn’t Chase Rewards

Here’s the truth: if you don’t pay off your credit card balance in full each month, rewards don’t matter. If you carry a $500 balance and pay 20% APR in interest, even earning 2% cash back doesn’t offset the interest charges. You’re losing money overall.

Focus on these priorities first:

- Understand how your card works

- Always pay your full balance by the due date

- Keep utilization low

- Build a strong payment history

Only after you’ve mastered those should you think about maximizing rewards.

When Rewards Actually Matter

Rewards are genuinely useful once you:

- Have a reliable income and budget

- Consistently pay your full balance every month

- Understand the card’s terms and don’t overspend to earn rewards

At that point, earning 1–2% cash back on everyday purchases is a real benefit. If you spend $10,000 a year and earn 2% cash back, that’s $200 in rewards with zero cost. That’s free money—but only if you don’t carry a balance.

Common Credit Card Fees Beginners Face

Interest is just one cost. Credit cards come with several potential fees, and beginners often don’t see them coming.

Annual Fees

Some credit cards charge an annual fee (typically $50–$500+ depending on the card’s rewards and benefits). Many beginner-friendly cards have zero annual fees, so there’s no reason to pay.

Late Fees

If you miss your payment due date, the issuer charges a late fee. These vary but can be $25–$40+. Late fees also come with interest charges on the unpaid balance.

More importantly, a payment 30+ days late is reported to credit bureaus and can significantly damage your credit score.

Foreign Transaction Fees

If you use your credit card overseas or make purchases in a foreign currency, you’ll typically pay a foreign transaction fee (1–3.5% of the transaction). This applies to:

- In-person purchases abroad

- Online purchases from foreign merchants in foreign currencies

- ATM cash withdrawals overseas

Cash Advance Fees

If you withdraw cash from an ATM using your credit card, you’ll pay a cash advance fee (typically 2–5% of the amount withdrawn). Additionally, interest on cash advances usually starts immediately—there’s no grace period. The interest rate for cash advances is often higher than the purchase APR.

Other Potential Fees

- Over-limit fees: If you spend above your credit limit (though most modern cards don’t allow this)

- Balance transfer fees: If you transfer a balance from another card (usually 3–5%)

Common Myths About Credit Cards

The credit card industry has some pervasive myths attached to it. Let’s bust the three most costly ones.

Myth 1: Carrying a Balance Builds Credit

The Truth: Carrying a balance does not build credit. This myth probably exists because credit bureaus like to see a balance reported on your statement, but that’s different from “carrying” a balance.

Here’s the distinction: A balance on your statement is the amount showing as of the statement date. A carried balance is what you don’t pay off—what rolls into the next month with interest charges.

You can have a balance on your statement and still pay zero interest. Just pay the full statement balance by the due date.

Carrying a balance does not improve your score. It increases your utilization (hurting your score), costs you money in interest, and shows lenders you’re struggling to pay what you owe.

Myth 2: Using Your Card Daily Hurts Your Credit Score

The Truth: Using your credit card frequently does not hurt your score if you pay it off in full each month. What matters is:

- Do you pay on time?

- What percentage of your limit are you using at statement time?

Use your card for everyday purchases if it helps you track spending or earn rewards. Just ensure you’re paying the full balance before interest kicks in.

Myth 3: Closing Old Credit Cards Helps Your Score

The Truth: Closing old accounts typically hurts your score, not helps it. Here’s why:

- It reduces your total available credit, increasing your utilization ratio on any remaining balances

- It shortens your average account age, which is a factor in your score

- It reduces credit diversity

If you want to close an account because of an annual fee, that’s reasonable. But if you’re trying to improve your score, keeping old accounts open (even with zero balance) is actually beneficial.

Smart Rules for First-Time Credit Card Users

If you’re getting your first credit card, follow these guidelines to use it wisely. Many beginners start with limited experience, and this guide on getting a credit card with low or no credit history explains how to approach credit safely.

How Much to Spend

Only charge what you can afford to pay back in full by the due date. A good rule: treat your credit card like a debit card. Don’t spend money on your credit card that you haven’t already earned.

When to Pay

Set a calendar reminder for a few days before your due date to make your payment. Even better, set up automatic payments to pay at least the minimum (ideally the full statement balance) automatically. This removes the risk of forgetting and incurring late fees.

What Never to Do

- Never take out a cash advance unless it’s a genuine emergency. The fees and interest are brutal.

- Never spend above your limit intentionally. It signals financial desperation to credit bureaus.

- Never open a credit card just for rewards. A card you don’t use responsibly is a liability.

- Never assume promotional rates are permanent. Many new cards offer 0% APR for 6–12 months, but the regular rate kicks in eventually.

- Never ignore your statement. Review it monthly for unauthorized charges and errors.

Frequently Asked Questions

How Do Credit Cards Work for Beginners?

You use the card to borrow money for purchases. The card issuer sends you a monthly statement with the amount owed. You have a grace period to pay the full balance interest-free. If you pay in full by the due date, no interest is charged. If you don’t, interest accumulates at the card’s APR, and the unpaid balance carries over to the next month.

When Do I Pay Interest?

You pay interest only if you don’t pay your full statement balance by the due date. Interest is calculated daily based on your APR and outstanding balance.

Is Minimum Payment Really That Bad?

Yes. Minimum payments are designed to keep you in debt as long as possible. Most of your payment goes to interest, barely touching the principal. Carrying a $500 balance can take years to pay off and cost hundreds in interest.

How Much of My Credit Card Should I Use Each Month?

Keep your balance below 30% of your credit limit at statement time. Ideally, keep it below 10%. If your limit is $1,000, that means keeping your statement balance under $100.

Do Credit Cards Automatically Build Credit?

No, but they can help you build credit through responsible use. Using a card and paying it on time demonstrates creditworthiness to lenders. However, just having a card and using it carelessly won’t build credit—you must pay on time consistently and keep utilization low.

Conclusion

A credit card is a tool, not free money. The card issuer is lending you their money with the expectation that you’ll pay it back—ideally quickly and in full. When you understand the system and use the card responsibly, it can be genuinely useful: you earn rewards, build credit history, and have a backup payment method.

But understanding beats rushing. Before you get a credit card, know:

- How your billing cycle works

- Why paying your full statement balance matters

- Why minimum payments are a trap

- How credit utilization affects your score

- Why carrying a balance costs money without building credit

Understanding how credit cards work before using one is the single most effective way to avoid long‑term debt. Take the time to learn now. The difference between a cardholder who understands credit and one who doesn’t can be thousands of dollars over a lifetime.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Credit card terms, interest rates, fees, and rewards vary significantly by card issuer and your individual profile. Before opening a credit card account, review the card’s specific terms and conditions. If you’re struggling with credit card debt, consider speaking with a financial advisor or credit counselor.