Client based income vs contract work credit cards is an important distinction credit card issuers consider when reviewing non‑salary applications. When you work for yourself—whether as a freelancer, contractor, or small-business owner—answering the income question on a credit card application can feel ambiguous. Should you report your gross revenue or your net earnings? Does the type of work you do matter as much as the amount? And more importantly, do credit card issuers actually care whether your income comes from ongoing client relationships versus one-off project contracts?

The answer is more nuanced than a simple yes or no, but the distinction does matter to lenders. However, what matters even more is stability, consistency, and the ability to document your income truthfully. Understanding how credit card issuers evaluate these different income streams can improve your odds of approval and help you avoid costly mistakes.

On This Page

- What Is Client-Based Income?

- What Is Contract Work Income?

- How Credit Card Issuers Evaluate Non-Salary Income

- Client Based Income vs Contract Work Credit Cards: Key Differences

- Which Income Type Do Credit Card Issuers Prefer?

- How Income Patterns Affect Approval and Credit Limits

- How Applicants Should Report Each Income Type

- Common Mistakes Freelancers and Contractors Make

- Frequently Asked Questions

- Conclusion

- Disclaimer

What Is Client-Based Income?

Client-based income refers to earnings from ongoing, recurring relationships with one or more clients. You might think of it as a quasi-retainer arrangement or steady stream of work that you can reasonably expect to continue over a predictable timeframe.

Examples include:

- A freelance writer who has signed a contract to produce three articles per month for a publication

- A consultant with a few long-term clients who retain their services on a monthly basis

- A web designer who maintains websites for multiple businesses on retainer agreements

- A contractor hired for ongoing project management work with expected continuity

The key characteristic is predictability. Your income may fluctuate slightly month to month, but you have documented evidence—usually in the form of a contract or established payment history—that this income will likely continue. Clients have committed to working with you beyond a single project, and you have visibility into what next month or next quarter will look like financially.

What Is Contract Work Income?

Contract work income typically comes from projects with defined start and end dates. Each engagement is finite and separate, even if you work with the same client multiple times.

Examples include:

- A software developer hired to build a custom application with a six-month timeline

- A marketing consultant brought in for a three-month campaign launch

- A construction worker hired for specific renovation projects

- A graphic designer creating a one-time brand identity project for a client

The defining feature is the project boundary. Payment is tied to project completion, and when the work ends, so does that income stream. There may be weeks or months between projects during which you have no revenue from that client. You might have multiple projects stacked throughout the year, but each one has an end date and a gap before the next one begins.

How Credit Card Issuers Evaluate Non-Salary Income

Credit card issuers don’t use a single formula when evaluating your eligibility. Instead, they apply a framework commonly known as the “Five Cs of Credit”: Character, Capacity, Capital, Conditions, and Collateral. For most credit card applicants, two of these matter most: Character (your payment history and credit score) and Capacity (your ability to repay).

Capacity is where income stability enters the equation. Issuers assess capacity by looking at your ability to service debt. This typically involves calculating your debt-to-income ratio—the percentage of your gross monthly income that goes toward existing debt payments. The lower your DTI, the more capacity you have to take on a new credit card payment. Credit card issuers are required to assess an applicant’s ability to repay before approving a credit card.

The critical insight is that issuers want to identify a “sustainable source of cash.” They’re not just asking how much you earned last month; they’re asking how much you can reasonably be expected to earn next month and the month after that. This is especially true for mortgage lenders and other large credit products, but it also applies to credit card approval, though to a lesser degree.

For self-employed individuals and contractors, issuers also consider employment and income stability. How long have you been doing this work? Do you have documented evidence of continuing income? Have you maintained a consistent income level or demonstrated an upward trend? These questions shape the issuer’s confidence in approving you. Banks use a structured review process to understand self‑employed income before approving credit cards.

Client Based Income vs Contract Work Credit Cards: Key Differences

| Factor | Client-Based Income | Contract Work Income |

|---|---|---|

| Income Stability | Ongoing, predictable, recurring | Project-based, episodic, with gaps |

| Visibility Into Future | Months or quarters ahead (usually documented) | Usually only one project at a time clearly defined |

| Income Continuity | Expected to continue; no defined end date | Ends on project completion; must find new work |

| Documentation | Retainer agreements, service contracts, invoice history | Project contracts, completion dates, invoices |

| Risk Perception | Lower perceived risk—predictable cash flow | Higher perceived risk—income gaps between projects |

| Ease of Verification | Straightforward (contract + payment history) | Requires more analysis (project timeline + gaps) |

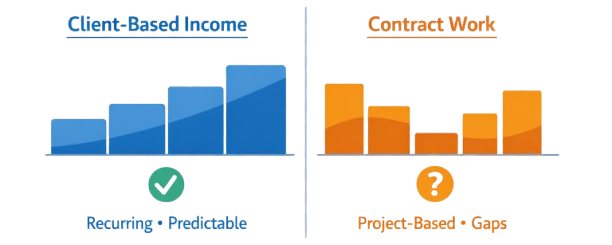

The fundamental difference from an issuer’s perspective is predictability. Recurring client income reduces the lender’s uncertainty about your ability to repay. Contract work introduces the question: What happens between projects? Will you land another one immediately? Is there a gap you need to cover?

This doesn’t mean contract workers can’t get approved for credit cards. It means the evaluation may require more scrutiny of your income history and employment consistency.

Which Income Type Do Credit Card Issuers Prefer?

The short answer: Recurring client-based income is generally perceived as more favorable than episodic contract work. For many freelancers, client based income vs contract work credit cards decisions depend more on income consistency than on how the work is labeled.

Why? Because recurring revenue provides visibility and consistency. From the lender’s perspective, a freelancer with three established clients paying them $3,000 per month each is lower risk than a contract worker who completes a $30,000 project, has two months off, then lands another contract. Both earn the same annually, but their cash flows look different. Many freelancers also ask whether income documents are required during the credit card application process.

However, the reality is more forgiving than it might initially seem. Credit card issuers don’t have uniform policies, and in practice, many contract workers are approved regularly. Here’s why:

- Most issuers don’t verify income for routine approvals. They rely on your stated income and cross-check it against your credit profile. If your credit history is strong and you’re not applying for an unusually large credit limit, many issuers won’t dig into the details of your employment structure.

- Income documentation isn’t always required. Unlike mortgage lenders, credit card companies often approve applications without asking for tax returns, contracts, or proof of income unless they suspect fraud or your application raises red flags (e.g., claiming $500,000 income with no credit utilization history).

- Your credit score matters more than income source. If you have a solid credit history, on-time payments, and reasonable credit utilization, the type of income becomes less central to the approval decision.

- Multiple income sources can strengthen your application. If you have some contract work combined with other income streams (even a part-time job, rental income, or freelance income from multiple clients), combining these strengthens your overall picture.

That said, issuers will care about income type in specific scenarios: when they ask for verification, when your application is flagged for manual review, or when you’re applying for a premium credit card with high credit limits that suggest substantial purchasing power.

How Income Patterns Affect Approval and Credit Limits

Initial Approval

For initial approval, income consistency matters more than the specific amount. An issuer reviewing your application wants to see that you’re employed and earning income—any income. Your credit score, payment history, and debt-to-income ratio typically dominate the approval decision for standard credit cards.

Contract workers are denied not because they work on projects but because of missing credit history, high existing debt, or low credit scores. Self-employed individuals with strong credit profiles are approved regularly, regardless of whether their income is recurring or project-based.

Credit Limit Sizing

Your credit limit is influenced by several factors: your credit score, credit history length, DTI ratio, and stated income. Higher income generally supports higher limits, all else being equal. But so does stability.

If you report $50,000 in annual income from a retainer client and the issuer can verify this through a contract or consistent payment history, you might receive a $5,000 limit. If you report the same $50,000 from project-based work but show a nine-month gap between projects the previous year, the issuer might offer a $3,000 limit—hedging against income uncertainty.

Credit Limit Increase Reviews

Issuers periodically review accounts for credit limit increases. During these reviews, they re-examine your income, credit score, payment behavior, and account utilization. An applicant with stable, documented, recurring income is more likely to receive a larger increase than someone with volatile or undocumented income.

Additionally, if you’ve shown a pattern of growing income—moving from contract work to some retainer clients, for instance—issuers may view this positively.

How Applicants Should Report Each Income Type

Accurate Income Averaging

The standard practice in lending is to average income over time. For self-employed individuals and contractors, lenders typically use either a 12-month or 24-month average:

- 12-month average: Used when income is stable or rising. This method is most favorable to borrowers with strong recent performance.

- 24-month average: Used when income is declining or highly inconsistent. This protects the lender by using a more conservative figure.

To calculate your averaged monthly income, For credit card applications, self‑employed applicants typically report net business income after expenses but before personal income taxes. Understanding client based income vs contract work credit cards helps applicants report income accurately and avoid verification issues later.

Example: If you earned $48,000 in net self-employment income over the past 12 months, your averaged monthly income is $4,000. If you earned $84,000 over 24 months, your 24-month average is $3,500 per month. The issuer may use whichever figure is lower or more conservative.

When reporting on a credit card application, you typically report annual income. Use your averaged income multiplied by 12 for consistency. Self-employed individuals report business income through federal tax filings, which lenders may reference when verifying income history.

Combining Multiple Income Sources

You can—and should—combine all qualifying income sources when applying for a credit card. This is especially valuable for contract workers or those with variable income.

Qualifying income sources include:

- Self-employment or freelance income (net earnings after business expenses)

- Salary from any employment (W-2 wages)

- Income from rental properties or investments

- Alimony or child support (if you receive it)

- Disability income or pension payments

- Spouse’s or partner’s income (if you’re 21 or older and have reasonable access to it)

Do not include loan proceeds, gifts, or one-time payments. These aren’t income.

If you earn $18,000 per year from retainer clients and work a part-time job earning $12,000 annually, report $30,000 total. This strengthens your application and increases your likelihood of approval and a higher credit limit.

Honest and Realistic Reporting

This cannot be overstated: report your income honestly. Lying on a credit card application is fraud, and the consequences are serious.

Many people believe they can “get away with” slightly inflating their income. While small discrepancies (a few hundred dollars on a $50,000+ income) are unlikely to trigger immediate consequences, the risk grows as the exaggeration grows. Moreover, if an issuer requests income verification and discovers significant discrepancies, they can:

- Close your account immediately

- Report you to fraud databases

- Blacklist you from future applications with that issuer

- Take legal action or report you to authorities

Importantly, credit card issuers can and do request income verification. This is especially common with premium cards, large credit limit increases, or when an account shows unusual spending patterns. If verification is requested, you’ll typically need to provide tax returns, W-2s, or bank statements. If your reported income doesn’t match these documents, you’re in trouble.

Common Mistakes Freelancers and Contractors Make

1. Mixing Income Types Incorrectly

Some self-employed individuals report their gross business revenue instead of net income. This inflates their stated earnings. If you earned $100,000 in revenue but paid $50,000 in business expenses, your net income is $50,000—that’s what you should report, not $100,000.

Lenders want to know what you actually have available to spend after business costs. This distinction is especially important for credit card applications that might later require verification.

2. Using Best Month Instead of Averages

It’s tempting to report your highest-earning month projected as annual income. But lenders look for consistency. If you made $8,000 in December (your best month) and averaged $3,000 the other 11 months, reporting $96,000 as annual income ($8,000 × 12) is misleading.

Use proper averaging: Add 12 months of earnings, divide by 12. If your income is highly variable or declining, expect the issuer to use a 24-month average, which will be even more conservative.

3. Applying With Short or Unclear Income History

Lenders prefer to see at least one to two years of self-employment income history. If you’re a new freelancer or just started contract work, you have limited track record. This doesn’t disqualify you, but it makes approval harder.

If you’re in your first year of self-employment, consider waiting until you have at least 12 months of documented earnings before applying. Alternatively, if you have other income sources (a part-time job, spouse’s income), include those to strengthen your application.

4. Inconsistent Income Reporting Across Applications

Don’t report different income figures to different issuers in a short time period. If you apply to three credit cards over two months and report $35,000, $42,000, and $38,000, and then one issuer requests verification, discrepancies raise red flags.

Report your actual, averaged income consistently. If your income genuinely increased (because you landed a new client or completed a high-value project), that’s a different story—just be prepared to document the change.

5. Failing to Document Contract Continuity

If you have retainer clients or ongoing project work, keep your contracts and invoices organized. These documents prove income continuity. If an issuer asks for verification, you’ll need to show:

- Service agreements or retainer contracts

- Recent invoices (showing work performed and payment terms)

- Bank statements showing deposits

- Tax returns (the ultimate proof of income)

Contract workers should maintain a similar paper trail, noting project timelines and completion dates to show they typically have overlap or quick turnaround between engagements.

Frequently Asked Questions

Is client-based income actually better than contract work for credit cards?

Generally yes, from a lender’s perspective. Recurring income is perceived as more stable and predictable, which reduces risk. However, credit card approval depends far more on your credit score, credit history, and debt-to-income ratio than on whether your income is recurring or project-based. Strong credit history can overcome the disadvantage of project-based work.

Do banks prefer recurring clients over project contracts?

Yes, all else being equal. But the advantage is modest. Both income types are acceptable for credit card approval. The difference becomes more pronounced in mortgage lending or other large credit products where income verification is mandatory and employment stability is heavily weighted.

Can client-based and contract income be combined on an application?

Absolutely, and you should. If you earn money from both ongoing clients and project work, add them together. This strengthens your application by increasing your total stated income and demonstrating income diversification.

Does income type matter more than credit score?

No. Your credit score and credit history matter far more than your income type. A contract worker with a 750 credit score will be approved more easily than a client-based freelancer with a 620 score. Credit history demonstrates your reliability as a borrower; income type is secondary.

How long should I have client income before applying for a credit card?

Ideally, at least 12 months of documented history. Some lenders will approve with less if you have strong credit or multiple income sources. However, the longer your track record, the easier approval becomes.

Do short-term contracts hurt approval chances?

Not inherently. What matters is whether you can document that contracts typically continue or that you regularly land new ones. If your recent history shows 3-4 months between projects with no explanation, an issuer might perceive higher risk. If you consistently move from one project to another with minimal gaps, you look stable.

How do issuers view income gaps between contracts?

As a risk factor, but not a dealbreaker. An issuer will ask: Is the gap typical for your industry? How do you cover expenses during gaps? Have you demonstrated the ability to find new work reliably?

If you can show a track record of quick turnaround or overlapping contracts, gaps are less concerning. If gaps are extended and unexplained, they raise questions about income stability.

Should freelancers report gross or average income?

report your average usable self‑employment income after business expenses (before personal taxes). Don’t deduct personal income taxes—lenders understand these come out of your earnings. However, do deduct business expenses to arrive at net self-employment income.

The confusion often arises because W-2 employees report gross salary (before taxes), while self-employed individuals report net self-employment income (after business costs). This difference is normal and expected.

Can new freelancers with established clients still get approved?

Yes. If you’re brand new to freelancing but have signed contracts with established clients and can provide these contracts as proof, you can apply immediately. You don’t need 12 months of history if you have documented evidence of ongoing work.

However, if you’re self-employed with no formal contracts and no payment history yet, approval is much harder. Build three to six months of payment history before applying.

Does switching from contract work to recurring clients affect approval?

Not negatively, assuming your income remains stable or increases. In fact, transitioning from project-based to retainer work demonstrates business maturity and stability, which issuers view favorably.

Just report your income consistently and honestly. If an issuer asks about recent changes in your employment, explain that you’ve moved to more stable, recurring work. This is a positive development.

Conclusion

Credit card issuers do prefer recurring, client-based income over episodic contract work, but this preference is far less critical than your credit history, credit score, and debt-to-income ratio. Both income types are acceptable for approval.

The real lesson is that consistency and honesty matter more than labels. An issuer wants to see that you earn money reliably and can document it truthfully. Whether that money comes from ongoing retainer clients or a series of well-managed contracts is secondary.

For freelancers and contractors applying for credit cards, focus on these three priorities: (1) maintain a strong credit history with on-time payments, (2) report income accurately using proper averaging methods, and (3) keep documentation organized in case verification is requested. Do these things, and income type becomes a minor consideration.

If you’re transitioning between income types or have highly variable earnings, consider combining multiple income sources on your application and waiting until you have at least 12 months of documented history. This approach significantly improves your odds of approval and often results in higher credit limits.

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, or tax advice. Credit card approval and income verification policies vary by issuer and applicant profile and may change without notice. Readers should seek advice from a qualified professional before making credit decisions or reporting income. Providing inaccurate information on a credit application may result in adverse consequences.