Introduction

Credit profile requirements for gig workers applying for credit cards are different from those faced by salaried employees, even when annual income levels are similar. The difference comes down to how credit card issuers assess risk. For salaried workers, approval hinges largely on a steady paycheck and clean payment history. For gig workers, delivery drivers, rideshare operators, freelancers, and task-platform workers the conversation becomes more complicated. Different gig income types, such as app-based earnings versus tip-driven income, can also affect how lenders evaluate consistency and repayment capacity. Lenders must account for income variability, multiple earning sources, and the absence of traditional employment documentation.

This doesn’t mean gig workers cannot qualify for credit cards. Rather, they need to understand what lenders actually scrutinize in a gig worker’s credit profile and how to present themselves strategically. A strong credit profile matters more than ever for this population, because it compensates for the very unpredictability that makes lenders nervous in the first place.

On This Page

- Introduction

- What Credit Card Issuers Mean by “Credit Profile”

- Core Credit Profile Requirements for Gig Workers

- Minimum Credit Score Gig Workers Typically Need

- Payment History: The Most Important Requirement

- Credit Utilization and Existing Debt

- Credit History Length and Thin Credit Files

- Income Stability vs. Credit Strength

- When Gig Worker Applications Face Extra Scrutiny

- Common Reasons Gig Workers Get Denied

- How Gig Workers Can Strengthen Their Credit Profile

- Frequently Asked Questions

- Conclusion

- Disclaimer

What Credit Card Issuers Mean by “Credit Profile”

When lenders speak of a “credit profile,” they are not referring to a credit score alone. A credit profile is the complete financial narrative that emerges from your credit report, payment patterns, income documentation, existing debt, and application details. It tells the story of how you have managed credit over time and signals how likely you are to repay a new card balance. Consumer credit reports and scores are designed to help lenders evaluate repayment risk across different borrower types, including those with irregular income.

Credit profile differs from credit score. A credit score is a single three-digit number typically ranging from 300 to 850 calculated from specific data points on your credit report. Your credit profile encompasses everything: the age of your oldest account, the consistency of your monthly deposits, patterns in how you use existing credit, recent applications for new credit, and any negative marks like late payments.

For gig workers specifically, lenders look beyond income stability. They examine whether you have demonstrated responsibility managing credit during periods of financial uncertainty. They assess whether your actual deposits and spending patterns align with what you have declared on your application. They evaluate whether you have a long enough credit history to establish a pattern of behavior. Each of these elements contributes to a holistic risk assessment that extends well beyond your credit score number.

Core Credit Profile Requirements for Gig Workers

Lenders use several key pillars when evaluating whether to approve a gig worker for a credit card. Understanding these requirements gives you a roadmap for strengthening your profile before you apply.

| Credit Factor | Why It Matters for Gig Workers | Impact on Approval |

|---|---|---|

| Payment History | Shows whether you consistently pay obligations on time, regardless of income swings | Most influential (35-40% of score); one missed payment can significantly damage approval odds |

| Credit Utilization | Demonstrates how much of your available credit you actually use; high utilization signals financial stress | Important (20-30% of score); keep below 30% for approval advantagebajajhousingfinance+1 |

| Credit History Length | Longer history shows lenders you have managed credit responsibly over time | Meaningful (15-20% of score); thin files make approval harder |

| Income Verification | Proof that your income, while variable, is real and traceable through legitimate channels | Critical for gig workers; must align with bank deposits and bank deposit records patterns |

| Recent Applications | Multiple recent credit applications suggest desperation or financial trouble | Each hard inquiry has small impact (~2-5 points) but multiple inquiries signal risk |

The most important principle: lenders care more about what your bank account reveals than what you declare on paper. If your stated income doesn’t match your actual deposits, or if your spending patterns suggest higher expenses than you claim to earn, approval becomes unlikely.

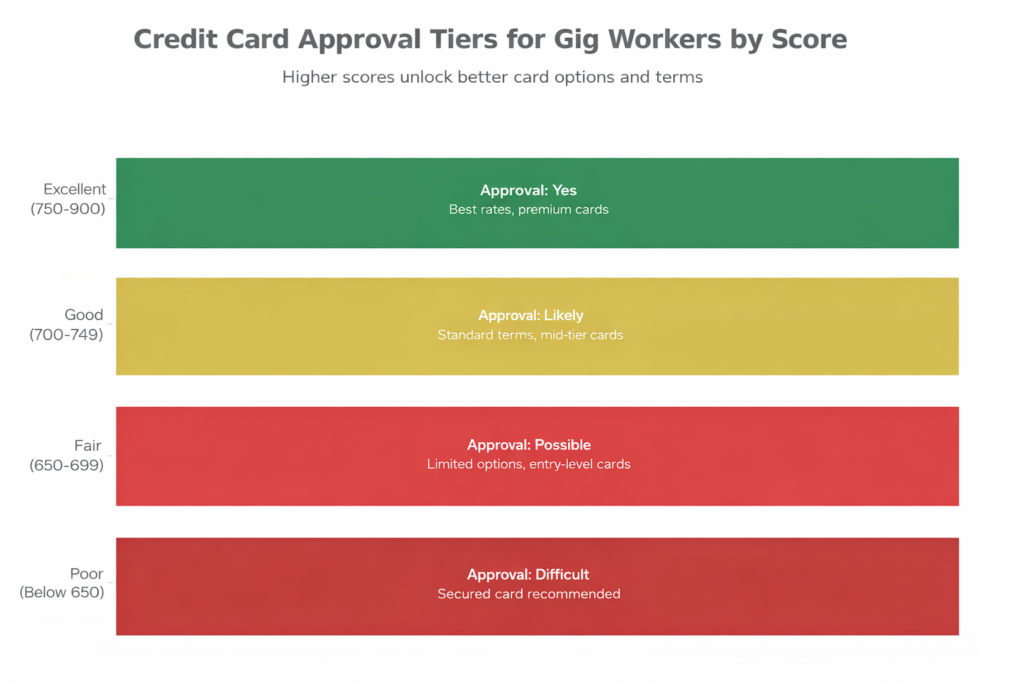

Minimum Credit Score Gig Workers Typically Need

Credit score expectations for gig workers are not dramatically different from salaried workers, but the context matters. A borderline score that might generate a marginal approval for a stable employee often results in outright rejection for someone with irregular income.

Entry-level cards: These typically require a score of 650 or above. Many entry-level offerings target consumers rebuilding credit or those new to credit entirely. However, for gig workers with scores in this range, approval is not guarantee depends heavily on other factors like payment history consistency and income documentation.

Mid-tier cards: Cards with better rewards or moderate annual fees usually require a score of 700 or above. This is where most gig workers who have built reasonable credit find success. A 700-750 score, combined with clean payment history and verifiable income, often results in approval for standard card offerings.

Premium cards: Cards offering significant rewards, travel benefits, or concierge services typically require a score of 750 or higher. Approval at this level usually includes lower interest rates and higher credit limits. Few gig workers pursue these cards, and those who do need not only strong credit scores but also documented income stability.

Why gig workers may need slightly higher scores: Lenders know that gig income introduces uncertainty. Even with identical credit scores, a gig worker and a salaried worker may face different approval odds. To offset this perceived risk, gig workers benefit from scores at the higher end of any given range. A score of 710 presents gig workers more competitively than a salaried employee at 710, as the gig worker must overcome additional scrutiny. Aim for 720 or above if possible. Understanding the credit profile requirements for gig workers helps applicants avoid unnecessary rejections and apply for cards they are realistically eligible for.

Credit Score Ranges and Card Approval Tiers for Gig Workers

Payment History: The Most Important Requirement

Payment history is the single most influential component of any credit profile accounting for 35 to 40 percent of your overall credit score. For gig workers, it carries even more weight, because consistent on-time payments demonstrate reliability despite income fluctuations. Payment history and credit utilization together form the foundation of most credit scoring models used by lenders.

Lenders understand that gig workers face genuine cash-flow challenges. They also understand that some gig workers manage these challenges through discipline and planning. When a gig worker with variable income makes every payment on time bills, existing credit card balances, loans, and other obligations that behavior sends a powerful signal: this person prioritizes their financial commitments regardless of earning circumstances.

The cost of late payments for gig workers is higher. A salaried employee who misses a single payment and then recovers may receive some leniency from underwriters, who might attribute the miss to a temporary lapse in attention. A gig worker who misses payment is often interpreted as a sign of genuine financial distress, because income variability is already seen as a risk factor. Even a 30-day late payment one that stays on your credit report can reduce your approval odds significantly.

Common mistakes gig workers make: Some gig workers delay payments during low-earning months, planning to catch up later. While understandable, this behavior damages credit profiles and significantly lowers approval odds. If you cannot meet an obligation in a slow month, contact your lender proactively before the payment due date. Many creditors offer hardship programs or temporary deferrals if you communicate before missing a deadline.

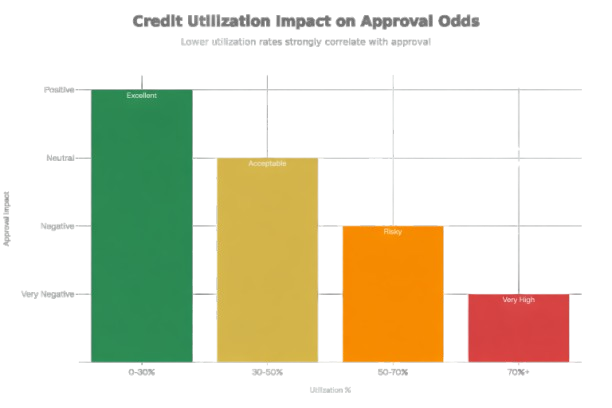

Credit Utilization and Existing Debt

Credit utilization the percentage of your available credit that you are actively using typically accounts for 20 to 30 percent of your credit score. For a gig worker, this metric becomes especially important because it directly reflects your financial stress level.

If you have a credit card with a $5,000 limit and you carry a $2,000 balance, your utilization is 40 percent. Lenders view this as moderate credit use and neutral to slightly concerning. If you carry $4,500 on the same card (90% utilization), lenders read this as a sign that you are heavily dependent on credit a red flag for someone with already-uncertain income.

The ideal range: Financial experts consistently recommend keeping utilization below 30 percent. This threshold demonstrates to lenders that you have available credit but choose to use only a portion of it, suggesting financial stability and discipline. Gig workers who maintain low utilization on existing cards significantly improve their approval odds for new cards.

High utilization signals financial stress, but it carries greater weight for gig workers. Lenders worry that variable income combined with high balances may lead to repayment problems during slower earning months, making additional credit riskier.

Credit Utilization Ratio Impact on Approval Odds

Managing balances with variable income: The practical challenge for gig workers is that cash flow varies month to month. A strategy that works: prioritize paying down balances during high-earning months rather than spending the extra income. This creates a buffer that helps you maintain lower utilization during slower months. Requesting credit limit increases as your profile improves can also lower utilization and strengthen future approval odds.

Credit History Length and Thin Credit Files

Credit history length how long you have been using credit accounts for 15 to 20 percent of credit scores depending on the scoring model. The logic is straightforward: a longer track record of consistent, on-time payments is a stronger signal of reliability than a short track record.

What “thin file” means: A thin credit file is a situation where someone has very little credit history perhaps only one or two accounts, or accounts that have been open for less than a year. Lenders struggle with thin files because they lack sufficient data to reliably assess credit behavior patterns. Someone with one perfect year of payment history might default in year two; lenders simply don’t know.

Why many gig workers have limited credit history: Gig work is often a career transition. Many gig workers are either newly self-employed or supplementing another income source. They may have few credit accounts open, or accounts that are relatively recent. Additionally, gig workers from immigrant backgrounds or younger gig workers starting their first independent work may literally be new to credit-using institutions in their country. This concentration of thin-file gig workers creates a structural disadvantage in traditional credit scoring systems.

| Credit History Length | Lender Confidence Level | Approval Likelihood |

|---|---|---|

| Less than 1 year | Very Low | Difficult; secured card recommended |

| 1-3 years | Low to Moderate | Possible; entry-level cards or cards with lower limits |

| 3-7 years | Moderate to Good | Likely; mid-tier cards achievable with fair/good scores |

| 7+ years | Good to Excellent | Strong approval odds; access to broader card selection |

How time builds trust: The fundamental principle is simple: if you make on-time payments consistently for three years, four years, and beyond, you become a lower-risk borrower in lenders’ eyes. The longer your account ages, the more powerful that signal becomes. Closing old accounts works against you even if they are paid off because it removes positive history from your profile.

For gig workers building credit from thin-file status: keep all old accounts open, even if you do not use them. Each active account with a long history strengthens your profile. Make small purchases on older cards occasionally and pay them in full to keep accounts active and visible to lenders.

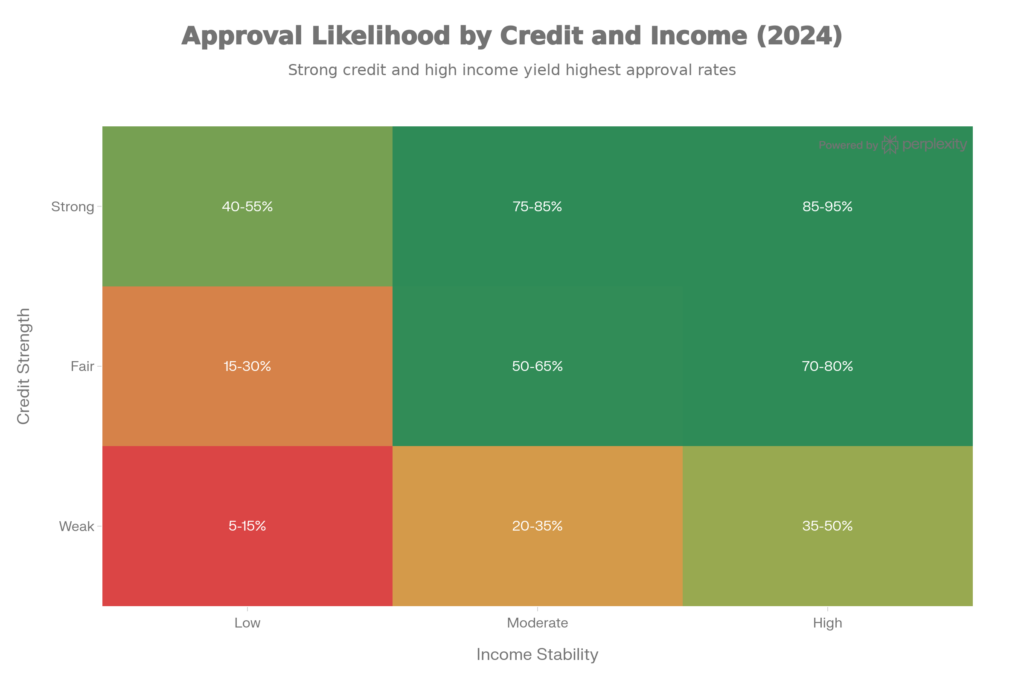

Income Stability vs. Credit Strength

A common misconception among gig workers is that high declared income guarantees approval. It does not. Lenders weigh credit strength and income stability separately, and a strong credit profile can often compensate for lower or more variable income. Banks follow specific income verification processes when reviewing gig worker applications, especially when income patterns are irregular. Self-employed and gig workers are often evaluated differently because income verification and consistency play a larger role in underwriting decisions.

Consider two applicants:

- Applicant A: Earns $5,000 per month in consistent salaried income, but has a 620 credit score due to a past default and high existing debt.

- Applicant B: Earns $3,000 to $6,000 per month from gig work, but has a 740 credit score with zero late payments and low utilization.

Applicant B is significantly more likely to be approved despite lower average income, because credit profile is the primary risk signal.

Credit Card Approval Matrix: Income Stability vs. Credit Strength

This distinction is critical for gig workers to understand. If you have modest income but pristine payment history and a thin credit file that you are actively building, you are in a stronger position than someone who earns well but has damaged credit. Focus on credit quality first, knowing that income can be variable.

When Gig Worker Applications Face Extra Scrutiny

Credit card applications from gig workers sometimes trigger additional review beyond the automated approval process. Understanding when and why this happens helps you prepare for potential follow-up questions or requests.

Manual reviews are common for gig workers when application details raise questions. If you declare $4,000 monthly income but your most recent tax return shows much lower annual earnings, a human reviewer will notice the discrepancy. If you apply for a card with a requested credit limit that seems disproportionately high relative to your declared income, manual review follows. Many gig workers also wonder whether traditional pay stubs are required during this review process, which is not always the case.

High stated income without corresponding financial documents often triggers scrutiny. Gig workers sometimes overstate earnings in hopes of qualifying for higher credit limits. Lenders can cross-check stated income against tax filings, bank deposit patterns, and payment app records. Income that appears inflated even moderately creates red flags and often leads to manual review that may ultimately result in denial or a lower limit than requested.

Credit limit increase requests from gig workers are more likely to be reviewed manually than automatic increases for salaried employees. When you request an increase, card issuers want to verify that your income can support the higher limit. Be prepared to provide current income documentation or bank statements showing increased deposits if you request a meaningful limit increase.

Inconsistent application data creates additional scrutiny. If the address on your application differs from your current address, or if employment details seem unclear, manual review may occur. Keep all information current and consistent across applications and with your credit file.

Common Reasons Gig Workers Get Denied

Understanding denial reasons helps you address vulnerabilities before applying. Here are the patterns that lead to rejection for gig worker applicants:

| Denial Reason | Why It Happens to Gig Workers | Better Approach |

|---|---|---|

| Thin credit profile | New to credit or limited account history; insufficient data for lenders | Open entry-level accounts; build history systematically over 1-2 years |

| High utilization | Variable income leads to high balances relative to limits during slow months | Pay down balances aggressively; request limit increases to lower utilization |

| Recent negative marks | Late payments or collections are highly visible on gig worker profiles due to already-elevated risk perception | Wait 6-12 months after resolving negative items; show clean payment pattern before applying |

| Too many recent applications | Multiple inquiries suggest financial desperation or credit-seeking behavior | Space applications 3-6 months apart; apply only when truly needed |

| Income not verifiable | Declared income doesn’t match actual deposits, bank deposit records, or tax filings | Provide tax returns, bank statements, or platform earning summaries proving income |

| High debt-to-income ratio | typically ranging from 300 to 850 Existing monthly debt payments or credit obligations are too large relative to stated income | Pay down existing debt before applying for new credit |

| Stated income mismatch | Most common: declaring only high-earning months as typical monthly income | Calculate actual average monthly income; disclose honestly |

How Gig Workers Can Strengthen Their Credit Profile

Building a strong credit profile as a gig worker is a systematic process. It requires patience but yields compounding rewards over time.

Build credit deliberately if you are starting from scratch: If you have no credit history, start with entry-level accounts. Many lenders offer secured credit cards (backed by a cash deposit) specifically for credit building. Open a secured card, use it for small purchases, pay in full each month, and keep it active for 12-24 months. Once you have established history with that card, you become eligible for unsecured cards with better terms.

Manage variable cash flow proactively: The challenge for gig workers is that disciplined payment timing becomes harder with irregular income. One strategy: establish a separate savings account specifically for credit obligations. When you earn above your average, deposit the surplus into this account. During low-earning months, draw from this account to make payments on time. This buffer approach decouples your payments from month-to-month volatility.

Use income documentation strategically: Many modern lenders accept alternative income documentation beyond traditional salary slips. Bank statements showing 6-12 months of deposits, tax returns, platform-generated earning summaries, and bank deposit records, transaction records are all credible proof of gig income. When applying, provide documentation that clearly shows you earn what you claim.

Apply strategically, not frequently: Space applications out over several months. Each application triggers a hard inquiry, and multiple inquiries in short periods signal financial desperation. Plan your applications: if you need a card in Q1, don’t also apply in Q1 and Q2. Wait until Q3.

Monitor your credit report regularly: Errors on your credit report are more common than people realize. Check your report quarterly for inaccuracies incorrectly reported late payments, accounts you did not open, or closed accounts that still appear active. Dispute errors immediately; correcting them can meaningfully improve your score.

Frequently Asked Questions

What credit profile do gig workers need for credit cards?

Most lenders approve gig worker applications with a credit score of 700 or above, combined with verifiable income, clean payment history, and utilization below 30%. Entry-level cards may be available at 650-700 scores if other profile elements are strong. The key is not the score alone but the complete narrative: demonstrating that you manage credit responsibly despite earning variability.

Do gig workers need higher credit scores than salaried workers?

In practice, yes gig workers benefit from aiming for scores at the higher end of any approval range. A 730 score gives a gig worker roughly the approval odds of a 700 score for a salaried employee. This is an unavoidable reality of how lenders evaluate risk. However, this gap closes when gig workers have very long, clean payment histories and can document income clearly.

Does gig income hurt approval chances?

Gig income itself is not a rejection reason; rather, the variability and difficulty in verification create higher underwriting caution. A lender cares less about the label “gig” and more about whether your actual deposits prove stable earning power. If you can document steady gig earnings over time, you are in a reasonable position for approval.

How long should gig workers wait after a denial before reapplying?

If denied due to low score, thin file, or recent negative marks, wait 6-12 months before reapplying. Use that time to build positive history: make every payment on time, reduce balances, and let time work in your favor. If denied due to too many recent inquiries, wait at least 3 months. If denied due to income verification issues, gather better documentation and reapply after 30-60 days.

Can gig workers qualify for credit cards with a thin credit file?

Yes, gig workers with limited credit history can still qualify, but options may be restricted. Lenders usually prefer to see at least one active credit account with a consistent payment record. A thin file often results in lower credit limits or entry‑level approvals until more history is built.

Conclusion

The credit profile requirements for gig workers are not fundamentally different from those for salaried employees yet the practical barriers are higher. Lenders approach gig-worker applications with justified caution about income variability, and that caution manifests in tighter underwriting standards, slightly higher score expectations, and heightened scrutiny of every application detail.

The path forward is not to dismiss these standards as unfair but to understand them and work within them strategically. Gig workers can and do get approved for credit cards at attractive terms. The keys are: maintain disciplined on-time payments regardless of income swings; keep credit utilization low by managing balances actively; build credit history length by keeping accounts open and in good standing; document income clearly using whatever proof lenders accept; and apply thoughtfully rather than frequently.

Your credit profile matters far more than your job title. A gig worker with strong credit behavior and verified income will beat a salaried employee with damaged credit every time. Focus on credit strength, manage income variability with intention, and the approval will follow. Meeting the core credit profile requirements for gig workers takes time, consistency, and disciplined credit behavior rather than perfect income stability. At UncoverCards, we focus on explaining how credit card approval really works for gig workers, freelancers, and independent earners navigating non-traditional income.

Disclaimer

This content is educational and informational in nature. It is not financial, legal, or tax advice. Credit card approval criteria vary significantly by card issuer, your specific credit profile, and underwriting guidelines that change over time. Consult with lenders directly regarding specific approval requirements for the cards you are considering. Your credit score is calculated differently by different bureaus, and scoring models vary by issuer. Always review your credit report for accuracy before applying for credit.