Freelancing offers independence and flexibility, but it also introduces a layer of complexity when applying for everyday financial products—especially credit cards. Unlike salaried employees who can easily produce a recent pay stub, freelancers often find themselves uncertain about what income to report and what happens if they’re asked to prove it. This confusion is understandable.

The application process feels straightforward, yet the rules around income documentation remain murky for anyone without a traditional employer. Many freelancers ask a common question: do freelancers need income documents for credit card applications, especially when income changes month to month.

The short answer is straightforward: most of the time, no—freelancers do not need to provide income documentation to get approved for a credit card. But the long answer matters far more, because there are specific situations where lenders will request proof, and understanding those scenarios can save you from unexpected application delays, rejections, or worse, account closures down the line.

On This Page

- Do Freelancers Need Income Documents for Credit Card Applications?

- How Credit Card Applications Are Evaluated for Freelancers

- What Counts as Income for Freelancers and Gig Workers

- When Income Proof May Be Requested

- Types of Income Proof Freelancers Can Use (If Asked)

- How Income Inconsistency Affects Approval Outcomes

- How Freelancers Should Estimate Annual Income

- Frequently Asked Questions

- Conclusion

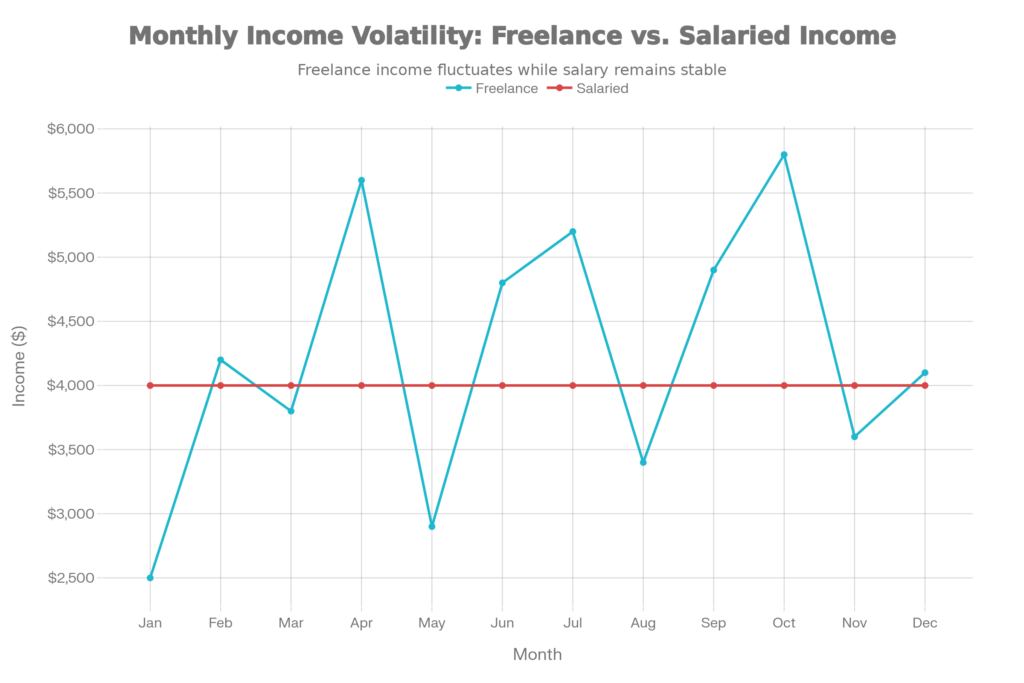

Freelancers often experience significant month-to-month income fluctuations, while salaried employees receive consistent income, a factor credit card issuers consider when evaluating approval and credit limits

Do Freelancers Need Income Documents for Credit Card Applications?

This confusion exists because do freelancers need income documents for credit card applications is not always clearly explained during the application process, especially for people with variable freelance income.

Credit card issuers are legally required to assess your ability to repay borrowed funds before issuing you a card. The federal regulations passed in 2009 mandate that lenders verify that cardholders can make at least the minimum monthly payment. However, this legal requirement does not mean the issuer must collect documents from you immediately.

In practice, most credit card applications operate on a system of stated income, where you simply report what you earn on the application form. Issuers accept your word for it—at least initially. They don’t call your clients, contact the IRS, or automatically request proof. For the vast majority of cardholders with moderate credit limits and clean credit histories, stated income is sufficient.

The distinction matters because there are two pathways in credit card applications:

Stated Income Applications are the standard approach. You provide your annual income on the form, and the issuer evaluates it alongside your credit score, credit history, and existing debt obligations. The issuer is unlikely to request documentation unless something in your application triggers additional scrutiny.

Verified Income Applications occur when an issuer asks for proof. This typically happens only under specific circumstances—a credit limit increase request, unusually high reported income, suspicious spending patterns, or after account opening if the issuer runs a financial review. At that point, you might be asked to submit pay stubs, tax returns, or bank statements.

| Application Factor | Stated Income | Verified Income |

|---|---|---|

| When typically used | Initial credit card application | Credit limit increases, financial reviews |

| Documents required | None (on application) | Tax returns, pay stubs, bank statements |

| Approval speed | Faster (often immediate or 1-2 days) | Slower (5-10+ business days) |

| Common triggers | Routine approval process | High credit request, income discrepancy, spending alerts |

How Credit Card Applications Are Evaluated for Freelancers

When you submit a credit card application, issuers use a mental checklist. They’re looking for confidence that you can pay at least the minimum monthly payment. For freelancers, the calculation is slightly different than it is for salaried employees, but not dramatically so. Approval decisions are also influenced by how credit card companies evaluate freelancer income across multiple months, not just a single high‑earning period.

The core principle is your ability to repay. Issuers examine your income relative to your existing debts—your housing payment, car loan, other credit card balances, and the proposed new credit card. This calculation, called your debt-to-income ratio, reveals what percentage of your income is already spoken for by obligations. If you’re using 50% or more of your income to pay existing debts, approval becomes harder. If you’re only using 20%, approval becomes easier. Federal consumer credit rules require lenders to consider an applicant’s ability to repay requirements for credit cards before approving a new account.

For freelancers, income trends often matter more than a single month of high earnings. An issuer might see that you reported $8,000 in income one month and only $2,000 the next month. Your average over a longer period—say six months or a year—paints a more realistic picture of your sustainable earning capacity. This is why your credit history as a freelancer can become an asset. If you have existing credit accounts and a demonstrated pattern of on-time payments despite variable income, lenders use that as evidence that you manage irregular paychecks responsibly.

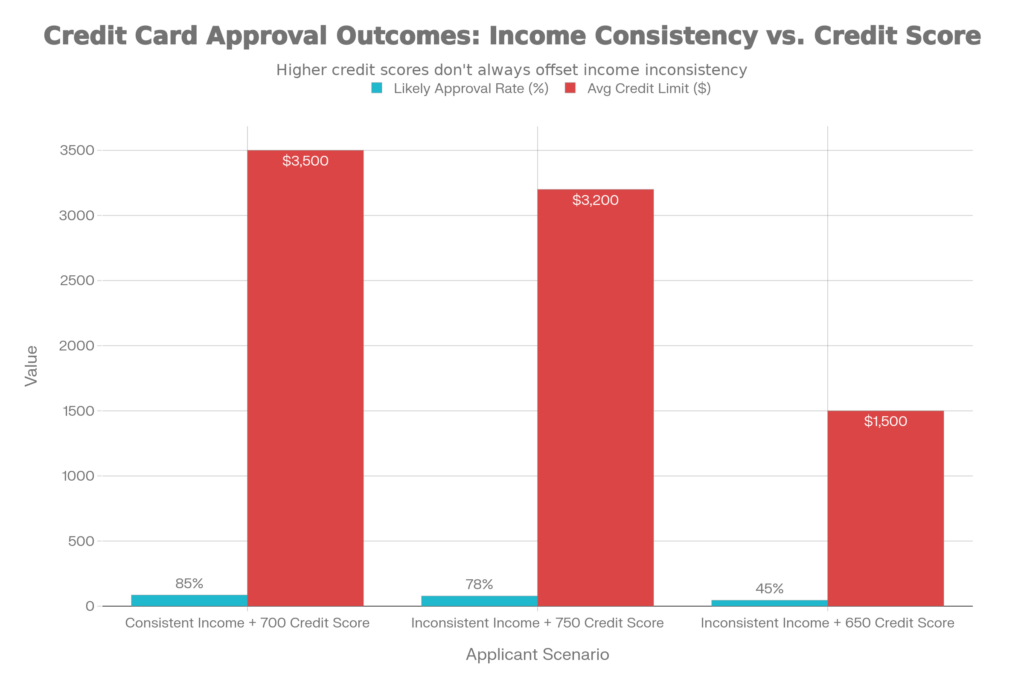

While credit scores matter significantly, income consistency combined with a moderate credit score often produces comparable approval outcomes to inconsistent income with a stronger credit score, showing how lenders weigh multiple factors

Your credit score typically carries more weight than your stated income in the initial approval decision. Someone with a credit score of 750 and inconsistent freelance income often gets approved more readily than someone with a 650 credit score and perfectly stable income. However, the combination of both factors—stable income and good credit—produces the best outcome.

What Counts as Income for Freelancers and Gig Workers

One of the biggest misconceptions among freelancers is that income must come from a single, verifiable source to count toward a credit card application. In reality, credit card issuers are quite flexible about what they’ll accept as income.

Self-employment income from your freelance work counts in full. If you earn $5,000 from client projects in a month, that’s reportable income. Unlike mortgage lenders who want to see two years of tax returns proving consistent self-employment income, credit card issuers take a more relaxed approach initially. You state it, they record it.

Multiple income sources can be combined. If you do freelance writing for $3,000 one month but also pick up a part-time job earning $1,500, you can report $4,500 total. Issuers specifically allow applicants to combine income from different sources. This flexibility particularly helps gig workers who cobble together income from multiple platforms or clients.

Household income is available to you if you’re 21 or older. If your spouse or partner has income and you have reasonable access to it (meaning it’s used to pay household expenses, or you have joint accounts), you can include that in your application. A freelancer married to a salaried employee earning $60,000 per year can legitimately include that spouse’s income when applying for a credit card—as long as the issuer allows household income on their application (some issuers moved away from household income after regulatory guidance in 2011, so check the application form).

What doesn’t count: borrowed money like student loans, money you don’t actually have access to, or income you expect to earn but haven’t started earning yet. Be conservative. If you’re starting a new freelance client next month but haven’t received payment yet, don’t count that income.

| Income Type | Gross Income Reported | Net Usable Income | Stability Perception | Documentation (if requested) |

|---|---|---|---|---|

| W-2 Salary (part-time) | Full amount | Similar to reported | High | Recent pay stubs |

| 1099 Freelance Income | Annual average or past 12 months | After expenses (sometimes) | Medium to Low | Tax returns, bank statements |

| Spouse/Household Income | Spouse’s income (if over 21) | Varies | Depends on visibility | Spouse’s pay stubs or tax returns |

| Investment/Dividend Income | Annual average | Full amount | High | Account statements |

| Gig Platform Income (Uber, DoorDash, etc.) | Annual or recent month average | After expenses | Low to Medium | Bank deposits, app earning statements |

When Income Proof May Be Requested

Understanding the triggers that cause an issuer to shift from stated income to verified income helps you anticipate what might happen with your application. Several scenarios are red flags for issuers.

High reported income often triggers verification requests. If you reported $25,000 in annual income on your last credit card application two years ago, and now you’re applying for a new card claiming $80,000, that dramatic jump raises questions. The issuer might ask: “Is this sustainable? Did your business genuinely grow this much, or are you inflating the number?” When the increase seems unrealistic relative to your credit history, verification becomes likely.

Credit limit increase requests are a common verification trigger. Unlike the initial application (where stated income suffices), when you ask an issuer to increase your credit limit—moving from $2,000 to $5,000, for example—the issuer may ask for updated income documentation to ensure you can handle the higher limit. This is especially true if your account age is long or if you’ve had the card for a while without updating income information.

Sudden changes in spending patterns can prompt financial reviews. If your issuer notices you’re spending dramatically more than you have in the past, or if you’re hitting your credit limit repeatedly, they may launch what’s called a financial review. This is where they request pay stubs, tax returns, or proof of income to verify that your reported income can actually support your spending. Financial reviews are expensive and rare for most cardholders, but they happen more frequently with premium cards that offer higher limits (such as those with limits above $25,000).

Multiple card applications in a short timeframe can invite scrutiny. If you apply for five credit cards in three months, issuers may flag this behavior as risky and request income verification to make sure you’re not opening accounts you can’t afford.

Types of Income Proof Freelancers Can Use (If Asked)

Should an issuer request documentation, freelancers have several options for proving income. The key is understanding what each document communicates to the lender.

Tax returns are the gold standard for proving self-employment income. Your most recent federal income tax return (specifically, the Schedule C form if you’re a sole proprietor) shows your net business income—essentially, what you actually earned after business expenses. Lenders like tax returns because they’re official documents filed with the government, making them hard to fake. The downside: they’re historical. Your last tax return might be a year old, so it doesn’t reflect your current earnings if business has significantly changed.

Bank statements provide a real-time window into your income. When you upload three to six months of bank statements, an issuer can see deposits from clients, track the consistency of your income, and assess your ability to cover expenses. For freelancers whose income varies wildly month-to-month, bank statements actually tell a better story than tax returns, because they show the full picture of deposits rather than just the annual total after expenses.

Profit and loss statements are useful if you maintain detailed business records. A P&L statement shows your revenue, expenses, and net income—basically, a simplified version of what appears on your tax return but created on your own schedule (you don’t have to wait for tax season). These are less formal than tax returns but more detailed than bank statements, and some issuers will accept them.

Business registration or professional license documents (if applicable) can support your application, though they don’t prove income directly. They establish legitimacy and show that you operate as a real business.

What won’t work: screenshots of earnings dashboards from gig platforms, invoices alone without bank statement proof of receipt, or estimates of future earnings. Issuers want documents that show money you’ve already earned, not money you expect to earn.

How Income Inconsistency Affects Approval Outcomes

The variability of freelance income influences your credit card application in several ways. First, it can slow down the approval decision. An issuer might approve a salaried applicant in minutes, but with a freelancer, especially one with high income fluctuation, the review process might take a few extra days while the issuer’s algorithm or a human analyst digs deeper into your profile.

Second, inconsistency can result in a lower initial credit limit. If you’re approved for a credit card as a salaried employee with a $4,000 monthly income, you might get a $3,500 credit limit. As a freelancer with an average monthly income of $4,000 but a range from $2,000 to $7,000, the issuer might only grant a $2,000 limit. They’re accounting for the possibility that you’ll hit a low month and need credit to cover basics—they want to ensure you can repay that amount.

Third, inconsistent income may trigger additional review steps. Some issuers use income-modeling algorithms that try to estimate your “true” income by looking at your credit profile, account history, and spending patterns. These algorithms aren’t perfect, and sometimes they flag freelancers for manual review simply because the algorithms struggle with non-traditional income patterns.

However, if your credit score is strong (above 750) and your payment history across existing accounts is spotless, many issuers will overlook income inconsistency and approve you with a reasonable credit limit. Your track record of responsible borrowing can outweigh the uncertainty of variable income.

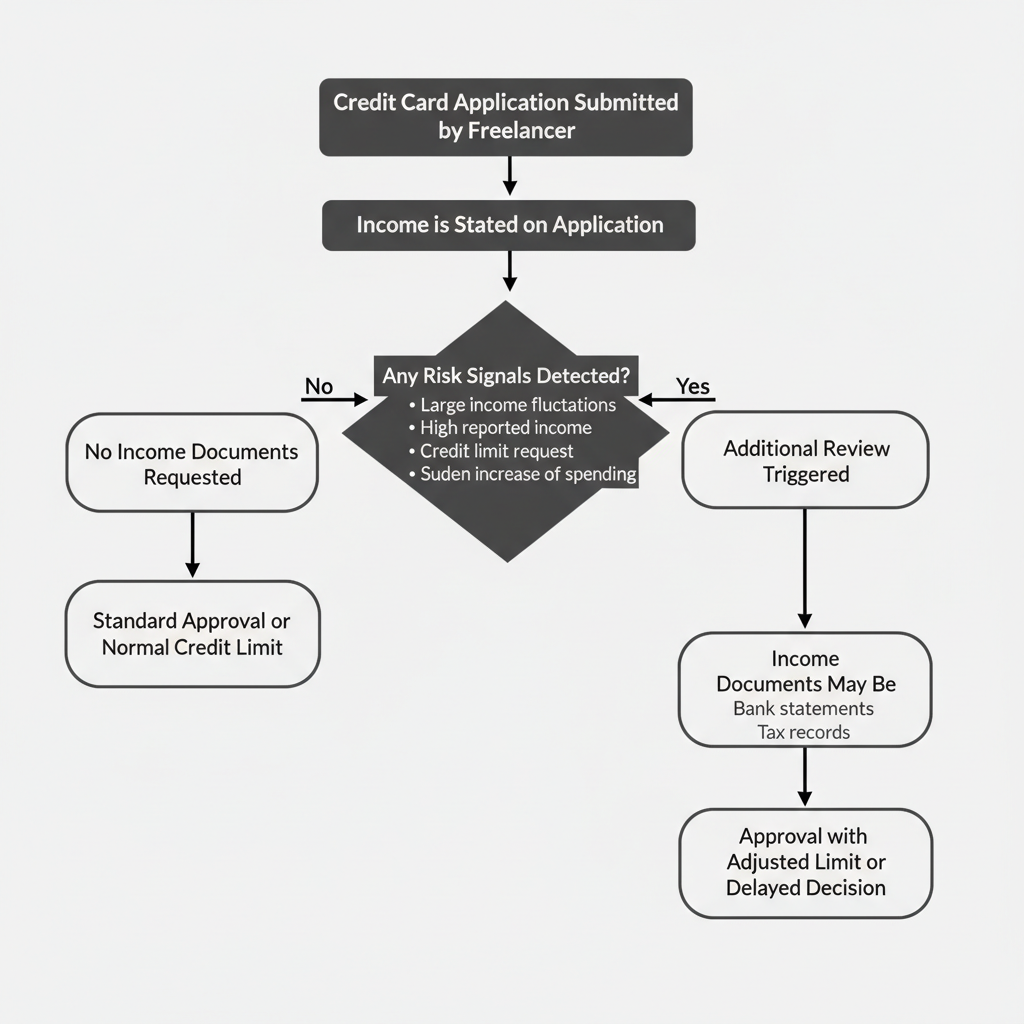

Decision‑flow showing when income documents may or may not be requested for freelancers

How Freelancers Should Estimate Annual Income

The challenge for most freelancers is deciding what number to put on the application. You can’t just write down your best month. You can’t ignore your worst month either. The goal is to be honest while presenting yourself in the best reasonable light.

Use a twelve-month average. Look back at the past year of income (or however long you’ve been freelancing) and calculate the average. If you earned $3,000 one month, $5,000 the next, $2,500 the following month, and so on, add them all up and divide by twelve. That’s your sustainable income. Report this number on your application. It’s defensible because it’s based on actual earnings, and if an issuer ever asks for verification, you can back it up with tax returns or bank statements.

Account for growth or decline. If you’re in your first year of freelancing and income is climbing—$1,000 in month one, $2,000 in month two, $3,500 in month three—you’re not in a steady state yet. For the application, use a number that feels sustainable for the immediate future, not your best recent month. If you’re confident that income will stabilize at $4,000 per month going forward, reporting $4,000 is reasonable. Freelancers often rely on self-employed income reporting basics when estimating annual income for credit card applications.

Household income is your safety valve. If your solo freelance income averages $3,000 per month and your spouse earns $50,000 per year (roughly $4,200 per month), and you’re 21 or older, you can report $7,200 total household income on the application. This is perfectly legal and helps offset concerns about income volatility.

What not to do: Don’t inflate your number significantly beyond what you can reasonably sustain. A $5,000 annual overestimate on a $36,000 income is negligible and unlikely to trigger verification. A $50,000 overestimate is conspicuous and likely will. If you’re ever caught in a serious mismatch—claiming $100,000 when you actually earned $30,000—the issuer can close your account and demand repayment. Beyond that, intentionally lying about income constitutes fraud, though prosecutors rarely pursue credit card applicants over income misstatements unless the fraud is part of a larger scheme.

Frequently Asked Questions

Can a freelancer apply for a credit card?

Yes, absolutely. Freelancers apply for and receive credit cards all the time. Credit card issuers don’t require employment; they require income. Whether that income comes from an employer, clients, investments, or a combination of sources is largely irrelevant to the issuer’s decision-making process.

Is income proof required for a credit card?

Not for the initial application. Most applicants, including freelancers, simply state their income and move forward without submitting documentation. However, an issuer can request proof later—when you ask for a credit limit increase, when they conduct a financial review due to spending patterns, or when an application is flagged for additional review. Many freelancers also explore credit cards for freelancers without proof of income when applying without traditional income documents.

Do I need to prove income for a credit card application?

The short answer is probably not. Most credit card applications don’t require proof at the time of submission. You might not encounter a document request unless you’re applying for a very high credit limit, requesting a significant increase, or have a credit history that triggers additional scrutiny. But it’s wise to have documentation ready (recent tax returns or bank statements) in case you’re asked.

Can I apply for a credit card without any income?

If you have no income at all, approval becomes much harder. You’d need to either report household income (if you’re 21 or older and have reasonable access to a spouse’s or partner’s income), use a co-signer, or apply for a secured credit card that requires a cash deposit instead of income qualification. However, if you’re a freelancer with even modest client income, you have reportable income and can apply for standard credit cards.

Conclusion

The reality for freelancers is more nuanced than the simple question suggests. You don’t need income documents to apply for a credit card in most cases—stated income is standard practice across the industry. However, you should understand that income documentation can become relevant later, whether during a credit limit increase request, a financial review triggered by your spending patterns, or if you make dramatic claims about your earnings.

The best approach is straightforward: report your income honestly using a realistic average of your recent earnings, be prepared to support that number with tax returns or bank statements if asked, and remember that your credit score and payment history often matter more than perfect income consistency. Understanding whether do freelancers need income documents for credit card applications helps freelancers apply with confidence and avoid unnecessary surprises.

For freelancers building their credit profile, maintaining clean payment history on existing accounts is your strongest asset. Issuers will overlook income volatility for applicants who demonstrate responsibility. Focus on paying all bills on time, keeping credit card balances low, and building a track record of reliable borrowing—these factors compound over time and make future applications easier, regardless of whether your freelance income fluctuates.

Disclaimer: This content is for educational purposes only and does not constitute financial, legal, or tax advice. Consult with a financial advisor or tax professional regarding your specific situation.