Introduction

Do gig workers need pay stubs for credit cards? If you drive for a rideshare service, deliver food, provide freelance services, or earn income through any non-traditional arrangement, you’ve likely encountered a frustrating assumption: that income verification for credit cards requires a traditional pay stub. This creates confusion and anxiety before even submitting an application.

The truth is simpler than you might think: most gig workers do not need pay stubs to qualify for credit cards. Credit card issuers operate under different rules than mortgage lenders or auto loan providers. They typically rely on what you state about your income rather than demand immediate proof.

However, understanding when documentation might be requested—and knowing how to present your income accurately—can significantly improve your approval chances. This guide explains what credit card companies actually look for, when they ask for verification, and how to position your gig income for the strongest application possible.

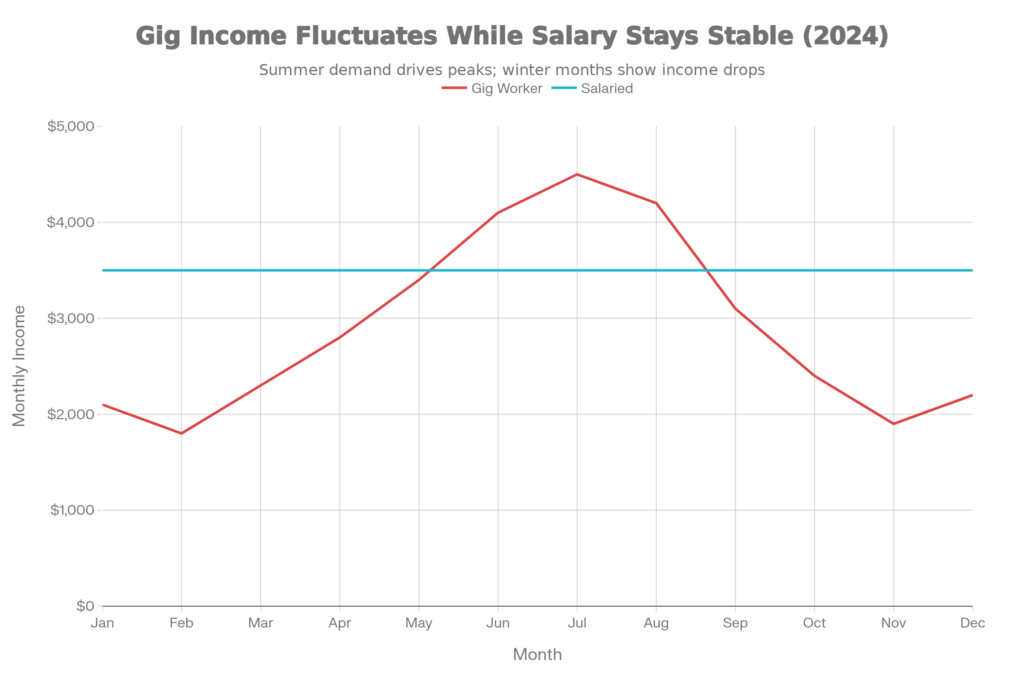

Monthly Income Volatility: Gig Workers vs. Salaried Employees

The chart above illustrates why traditional pay stubs don’t apply to gig work. Salaried employees receive consistent income every month—something lenders can easily verify through a single pay stub. Gig workers, by contrast, experience natural income volatility. Some months bring $4,500; others bring $1,800. This isn’t a sign of financial unreliability; it’s simply how flexible work operates. Credit card companies recognize this reality and evaluate gig worker applications differently.

On This Page

- Introduction

- Do Gig Workers Need Pay Stubs for Credit Cards?

- Why the Difference?

- How Credit Card Applications Are Evaluated for Gig Workers

- Why Income Consistency Matters (But Less Than You’d Think)

- What Counts as Income for Gig Workers

- Types of Income You Can Report

- Gross vs. Net Income

- When Income Proof May Be Requested

- Common Triggers for Documentation Requests

- Types of Income Proof Gig Workers Can Use (If Asked)

- Bank Statements

- Tax Returns and Transcripts

- Income Summaries from Platforms

- Invoices and Contracts

- What NOT to Use

- How Income Inconsistency Affects Credit Card Approval

- What Happens When Income Is Irregular

- How to Improve Approval Chances With Irregular Income

- How Gig Workers Should Estimate Income on Applications

- Calculate an Honest Average

- Account for Significant, Predictable Expenses

- Handle Seasonal Income Honestly

- Include All Legitimate Income Sources

- Never Overstate

- Frequently Asked Questions

- Conclusion

Do Gig Workers Need Pay Stubs for Credit Cards?

The direct answer: No.

Federal law and industry practice work in your favor here.

Credit card issuers are required by the Credit Card Accountability, Responsibility, and Disclosure (CARD) Act of 2009 to evaluate your ability to pay before extending credit. This does not mean they must verify your stated income before approval. In fact, most credit card companies rely on stated income—the amount you report on your application—without immediate verification.

This is fundamentally different from mortgages or auto loans, where lenders typically verify income upfront using pay stubs, W-2 forms, or tax returns. Credit cards are often approved within minutes based on your credit report and the income you provide, without any supporting documentation.

For related guidance, you can also read whether gig workers can get credit cards without proof of income.

Why the Difference?

Several factors explain why credit cards operate this way:

- Credit cards are unsecured debt. Unlike mortgages (backed by a house) or auto loans (backed by a vehicle), credit cards have no collateral. Lenders rely more heavily on your credit history and less on income verification.

- Federal rules encourage faster approvals. The CARD Act mandates ability-to-pay assessment, but lenders can use income estimation models and credit profile analysis to make that determination without requesting documents.

- Technology enables risk assessment. Credit card companies use sophisticated algorithms that cross-reference your stated income against your credit report, existing debts, and account behavior. Red flags trigger manual review, not routine documentation requests.

- Applicants expect quick decisions. The credit card industry has built approval processes around same-day or instant decisions. Immediate document requests would slow this down.

| Application Type | Income Proof Required? | Verification Process | Typical Approval Timeline |

|---|---|---|---|

| Standard credit card | Rarely upfront | Stated income + credit report analysis | Minutes to 24 hours |

| Credit card with manual review | Often yes | Documents requested; approval delayed | 3-7 business days |

| Credit limit increase | Sometimes yes | May request recent pay stub or tax return | Same-day to 48 hours |

| Mortgage or home equity | Yes, mandatory | Multiple documents required | 30-45 days |

| Auto loan | Yes, mandatory | Pay stub + recent tax return | 1-7 days |

How Credit Card Applications Are Evaluated for Gig Workers

Understanding how lenders evaluate your application helps you position your income for the best outcome.

The “Ability to Repay” Standard

When credit card companies review your application, they’re assessing one core question: Can this person make at least the minimum payment each month?

To answer this, they examine:

- Your stated monthly income. This is what you report on the application. There’s no magic formula, but it should reflect a realistic average of what you actually earn.

- Your credit history. Are you someone who pays bills on time? Do you have a track record of responsible credit use? A strong payment history tells lenders that you manage debt responsibly, even during months when income is lower.

- Your existing debt obligations. How much are you already paying out in monthly loan payments, credit card minimums, and housing costs? Lenders look at your debt-to-income ratio—the percentage of your monthly income consumed by these obligations. A ratio below 40% is typically healthier.

- Your account behavior with the issuer. After you’re approved, your actual spending and payment patterns matter enormously. A gig worker who consistently pays on time will build the credibility to request credit limit increases with relative ease.

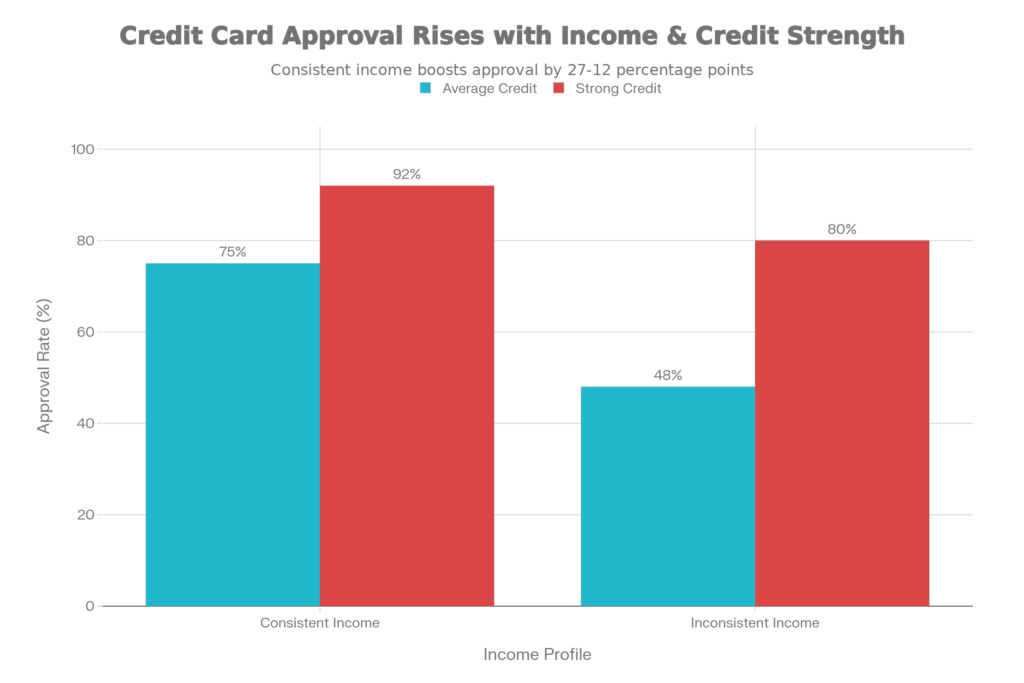

Why Income Consistency Matters (But Less Than You’d Think)

One of the most misunderstood points about gig worker credit applications is the role of income consistency. Yes, inconsistent income is noticed. But it’s not a dealbreaker—especially if other factors are strong.

Here’s what matters:

- If you have a strong credit score (above 670), inconsistent income is less of a barrier. Your payment history demonstrates responsibility.

- If you have average or weak credit, consistent income becomes more important. Lenders need something to feel confident, and if your credit history is thin, steady earnings help.

- If your stated income is modest and realistic, it’s less likely to trigger scrutiny regardless of consistency.

Credit Card Approval Rates by Income Consistency and Credit Profile

This chart shows how approval rates shift based on these two factors. When you have both consistent income and strong credit, approval rates exceed 90%. But notice: even with inconsistent income, a strong credit score keeps approval rates at 80%. This is encouraging news for gig workers who may have irregular earnings but solid payment histories.

What Counts as Income for Gig Workers

Not all income is created equal in the eyes of credit card lenders. Here’s what qualifies and how to think about it.

Types of Income You Can Report

- Gig platform earnings. Income earned through ride‑share platforms, delivery apps, freelance marketplaces, and similar gig platforms

- Freelance and contract work. Writing, design, programming, consulting—any 1099 income

- Cash-based business income. Earned through your own business or side work (provided you deposit it in a bank account)

- Rental income. From a property you own

- Investment income. Dividends, interest, capital gains

- Unemployment benefits or disability payments. If you’re receiving these, they count

- Household income. If you’re 21 or older and can demonstrate reasonable access to a spouse’s or partner’s income, you can include it on your application

Gross vs. Net Income

Here’s a nuance that trips up many gig workers: should you report gross earnings or net earnings?

GGross income is what you earn before any deductions. If a gig platform pays you $4,000 in a month, that amount is considered gross income.

Net income is what you keep after expenses. That same $4,000, minus gas, vehicle maintenance, platform fees, and insurance, might be $2,800.

Most credit card applications don’t explicitly define which one they want, which creates ambiguity. Here’s the practical answer: state the income you believe you can reliably use to pay the credit card bill. For gig workers, this often means something between gross and fully-expensed net income—perhaps 70-80% of gross after accounting for major variable costs.

Being honest and internally consistent matters more than the exact number. If you’re audited or asked to verify income, you’ll need to be able to explain and support your figure.

| Income Reporting Method | Example Monthly Amount | How Lenders Perceive It | Best For |

|---|---|---|---|

| Gross earnings (before all deductions) | $4,000 | Optimistic; may trigger questions if you claim high expenses | New gig workers, strong credit |

| Gross minus major expenses (gas, fees) | $2,800 | More conservative and credible; realistic | Most gig workers |

| Net income (fully expensed) | $2,400 | Very conservative; safest but may lower credit limit | Lowest-income workers, weak credit |

| Household income (including spouse) | $5,500 | Credible if you have reasonable access | Married couples, one lower earner |

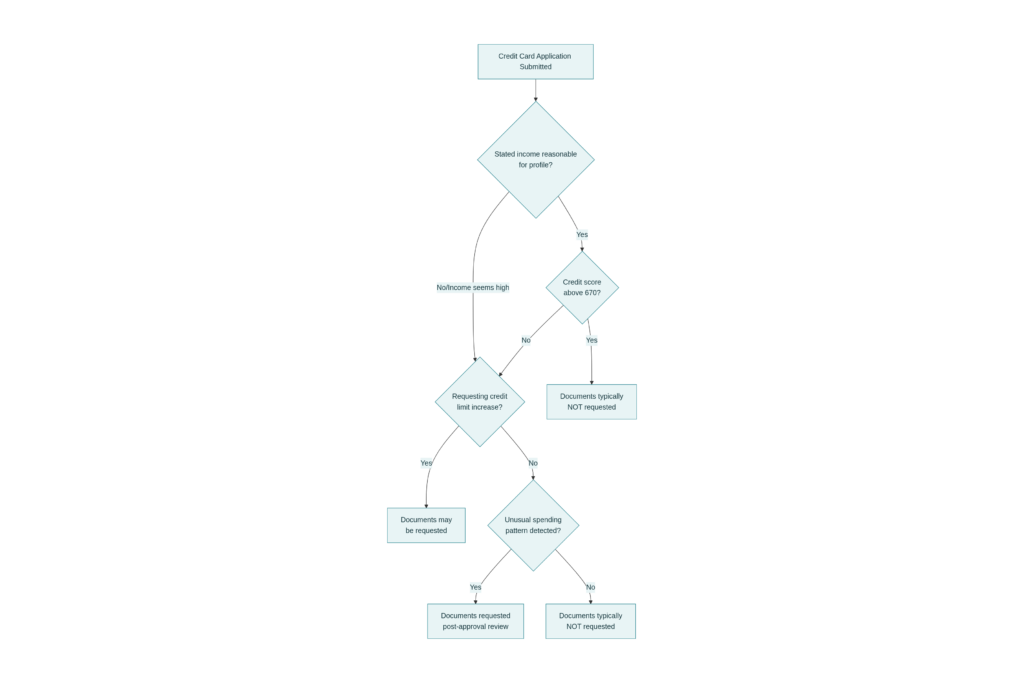

When Income Proof May Be Requested

Most gig workers won’t be asked for income documentation at the point of application. But it can happen. Knowing when and why helps you prepare.

Common Triggers for Documentation Requests

1. Manual Review

Automated approval systems flag certain applications for human review. Triggers include:

- Your stated income seems unusually high relative to your stated occupation or work history

- Your stated income seems inconsistently low (which raises questions about why you’re applying)

- A large gap between your stated income and what your credit report suggests you earn based on debt obligations

- Your credit history is limited or damaged, and the reviewer wants additional confidence

2. Credit Limit Increase Requests

When you apply to increase your credit limit after approval, issuers are more likely to ask for proof. You might be asked to submit:

- Recent pay stub (irrelevant for gig workers, but you can provide an earnings summary instead)

- Tax return from the past 2 years

- Bank statement showing recent deposits

- An earnings letter from a platform or client

3. Post-Approval “Financial Review”

Certain issuers, particularly premium card brands, conduct periodic reviews of account holders. If your account is flagged—perhaps due to unusual spending or a mismatch between your stated income and card usage—they may request documentation at that point.

4. Unusual Spending Patterns

If your credit report shows that you’ve suddenly run up balances across multiple cards or are spending far more than your stated income would reasonably support, the issuer may conduct a review to prevent fraud or over-extension.

When Income Documents Are Requested for Credit Card Applications

This flowchart shows the typical decision tree lenders follow when determining whether to request income documentation. For most gig workers with reasonable stated income and decent credit, documents are not requested at the point of application.

Types of Income Proof Gig Workers Can Use (If Asked)

If you’re asked to verify your income, you have options—and traditional pay stubs are not the only path.

Bank Statements

What to provide: 6 to 12 months of bank statements showing regular deposits from your gig work or business income.

Why it works: Statements provide a clear record of actual cash deposits. Lenders can see the frequency and amount of deposits, which directly demonstrates your ability to earn. This is often the easiest documentation for gig workers to provide.

Pro tip: Use a separate business bank account if possible. Lenders can clearly see income deposits without sifting through personal expenses.

Tax Returns and Transcripts

What to provide: Copies of your most recent 1 or 2 years of federal tax returns (Form 1040 with Schedule C for self-employed income).

Why it works: Tax returns are official documents that are filed with the IRS as part of annual tax filings. They carry significant credibility. If you’re claiming $30,000 in annual gig income, showing a Schedule C that confirms this amount is powerful proof.

Important: You don’t need extremely high income to show a tax return. Even modest earnings supported by a return are better than no documentation. If you earned less than $600 from a client and didn’t receive a 1099, you may not have a tax return to show—but you can explain this.

Income Summaries from Platforms

What to provide: Earnings reports or income summaries generated by the gig platforms, payment processors, or marketplaces you work with.

Why it works: These documents come from the source of your income and are difficult to fabricate. They show consistent earning patterns and are increasingly recognized by lenders.

Note: These are most reliable if they show multiple months or a year of earnings, not a single week.

Invoices and Contracts

What to provide: Copies of recent invoices you’ve issued and corresponding payment receipts showing those invoices were paid.

Why it works: Invoices demonstrate business legitimacy and client relationships. They’re especially valuable for freelancers in fields like consulting, design, or writing.

What NOT to Use

- Screenshots from apps. Easily doctored; lenders rarely accept them.

- Estimates or projections. “I expect to earn $50,000 this year” isn’t documentation.

- Verbal confirmations. Get everything in writing.

- Unverified statements from friends or family members. Only official documents count.

How Income Inconsistency Affects Credit Card Approval

Income volatility doesn’t disqualify you from credit card approval. But it does influence the process.

What Happens When Income Is Irregular

1. Approval May Take Longer

If your stated income triggers questions—or if your credit profile is average—your application may be routed to manual review instead of automated approval. This extends the timeline from minutes to several business days.

2. Your Initial Credit Limit May Be Lower

If approved, you might receive a lower credit limit than you’d get with consistent income. A salaried worker earning $50,000 might get a $10,000 limit; a gig worker with the same stated $50,000 income might get $5,000. This is a conservative approach, but limits can be increased over time with responsible use.

3. Additional Verification Steps May Be Required

You might be asked to verify employment (which is tricky for gig workers), provide documentation of income, or submit to a co-signer or guarantor arrangement.

4. Your Credit Score Becomes Extremely Important

This cannot be overstated: if your income is inconsistent, your credit score becomes your strongest asset. A 750+ score tells lenders, “I have a track record of managing credit well.” A 600 score combined with inconsistent income is a weaker position.

If you want a deeper explanation, this guide on how inconsistent gig earnings affect credit card approval explains the process in more detail.

How to Improve Approval Chances With Irregular Income

- Build your credit history. Before applying for premium cards, establish a track record with secured cards, retail cards, or credit-builder loans.

- Reduce your existing debt. A lower debt-to-income ratio makes you a less risky applicant.

- Use a stable secondary income source if available. If you have any W-2 income (even part-time), include it. It demonstrates income diversity.

- Apply with a co-signer. If you’re early in a gig career or have weak credit, a co-signer with stable income significantly improves approval odds.

- Consider cards designed for self-employed or gig workers. Some cards have underwriting criteria better suited to non-traditional income.

How Gig Workers Should Estimate Income on Applications

Accuracy and honesty are essential. Here’s how to think through the number you report.

Calculate an Honest Average

Don’t use your best month. Don’t use your slowest month. Use a realistic average across the past 12 months.

Example:

Over the past 12 months, you earned:

- $1,800 (Jan), $1,600 (Feb), $2,200 (Mar), $2,800 (Apr), $3,400 (May), $4,100 (Jun), $4,500 (Jul), $4,200 (Aug), $3,100 (Sep), $2,400 (Oct), $1,900 (Nov), $2,200 (Dec)

Total: $34,200 ÷ 12 months = $2,850 monthly average

This is what you should report, not the $4,500 you earned in July.

Account for Significant, Predictable Expenses

If you’re deciding between gross and semi-net income, consider major costs that affect your ability to pay a credit card bill:

- Gas or vehicle costs (for delivery/rideshare)

- Platform fees (typically 15-30% for many platforms)

- Equipment or supplies essential to the work

- Vehicle insurance required for commercial use

A reasonable approach: deduct 20-30% from gross income for these items, then report that figure. This is more defensible than either pure gross income or a heavily expensed net figure.

Handle Seasonal Income Honestly

If your income is highly seasonal (e.g., holiday delivery drivers earn much more in November-December), you have two legitimate approaches:

- Use a true 12-month average. This is the most honest and defensible.

- Explain seasonality on the application. Some applications have space for notes. A brief note—”Income is seasonal; $2,850 monthly average based on 12-month history”—helps.

Include All Legitimate Income Sources

If you have multiple income streams, add them:

- Gig platform earnings + freelance clients + part-time W-2 job = total income to report

- Your income from your spouse (if you’re including household income) = add to your own

Never Overstate

Deliberately inflating income on a credit application is fraud. Consequences include:

- Account closure after approval

- Legal action by the issuer

- Potential criminal charges

- Forfeiture of any rewards you earned

The risk far outweighs any short-term benefit of a slightly higher credit limit. Also, issuers conduct periodic reviews. If you claim $60,000 in annual income but your bank statements show $30,000, that discrepancy will eventually be noticed.

Frequently Asked Questions

Do gig workers need pay stubs for credit cards?

No. Most credit card issuers rely on stated income without requiring immediate proof. Unlike mortgages or auto loans, credit cards are approved based on your credit report and your stated income. Documentation may be requested during a manual review or for credit limit increases, but it’s not required upfront.

Can gig workers apply without any income proof?

Yes. Many gig workers are approved for credit cards without ever submitting documentation. Credit card companies use automated systems that evaluate your stated income, credit score, debt history, and credit report behavior. As long as your application doesn’t trigger red flags, you won’t be asked for proof.

What income do credit card issuers look at for gig workers?

Lenders evaluate any income you receive regularly and expect to continue receiving. This includes gig platform earnings, freelance income, rental income, investment income, disability benefits, unemployment benefits, or household income (if you’re 21+ and have reasonable access to a spouse’s or partner’s income). The key is that it must be ongoing, not a one-time payment.

Does inconsistent income reduce approval chances?

Inconsistent income makes approval harder, but it’s not a dealbreaker. If your credit score is strong (700+), inconsistent income is less of a barrier. If your credit score is lower (600-700), lenders may require additional verification or offer a lower credit limit. Building a strong credit history is essential for gig workers because it compensates for income unpredictability.

What if I have no income history yet?

If you’re brand new to gig work, credit card approval is harder but not impossible. Strategies include: building credit with a secured card first, becoming an authorized user on a family member’s account, using alternative lenders that accept gig workers, or applying with a co-signer. Many platforms now help new gig workers establish credit through responsible use.

Can I include my spouse’s income?

Yes, if you’re 21 or older and can demonstrate reasonable access to that income. This might mean a joint bank account, the ability to pay bills from your spouse’s earnings, or a joint tax return. You can’t include a roommate’s or friend’s income unless you’re married or in a legally recognized partnership.

What happens if I’m asked to verify my income?

Provide the strongest documentation you have: 6-12 months of bank statements, recent tax returns, platform earnings summaries, or invoices. Bank statements are often easiest and most credible for gig workers. Be prepared to explain how you calculated your stated income.

How often do credit card companies verify income after approval?

Infrequently, but it happens. Manual “financial reviews” are triggered by unusual account activity, requests for large credit limit increases, or suspected fraud. As long as you use your card responsibly and don’t show dramatic spending misalignment with your income, you’re unlikely to face a review.

Can I report net or gross income?

Most applications don’t specify. Report the income you realistically have available after major expenses needed to earn that income. Being honest is more important than the exact figure. If asked to verify, you’ll need to support the number you reported.

What’s a reasonable debt-to-income ratio for gig workers?

Below 40% is generally healthy (your monthly debt payments divided by gross monthly income). For gig workers with variable income, keeping this ratio below 35% is even better, as it provides a buffer during slower months.

Conclusion

Here’s what you need to remember: gig workers do not need pay stubs for credit cards. Most credit card issuers approve applications based on stated income without requiring upfront verification. Your credit score, credit history, and the reasonableness of your stated income matter far more than proof of traditional employment.

When income documentation is requested—whether during initial application, manual review, or a credit limit increase request—gig workers have viable alternatives to pay stubs: bank statements, tax returns, platform earnings summaries, and invoices.

The key to successful credit card approval as a gig worker is threefold:

- Be honest about your income. Calculate a realistic 12-month average and report that.

- Build your credit score. Since income consistency is harder to demonstrate, a strong payment history becomes your greatest asset.

- Understand the evaluation process. Lenders aren’t judging you based on employment type; they’re assessing your ability to repay. Show responsibility through on-time payments, low debt levels, and reasonable income statements.

Income volatility is a reality of gig work, and credit card companies understand this. Your path to approval doesn’t depend on fitting into a traditional employment box—it depends on demonstrating financial responsibility and manageable debt relative to your earnings.

Disclaimer: This article is for educational purposes only and should not be construed as financial, legal, or tax advice. Credit card eligibility varies by issuer and individual circumstances. Consult with a financial advisor or the specific credit card issuer for guidance tailored to your situation.