Introduction

Applying for a credit card feels straightforward when you receive a regular paycheck. How banks verify self employed income for credit cards is often misunderstood by freelancers and independent workers. You look at your pay stub, note the annual salary, and move on. But for self-employed workers, freelancers, and gig economy participants, that simple question—”What is your annual income?”—becomes complicated quickly.

Self-employed income is fundamentally different from a salary. It fluctuates month to month. It comes from multiple sources. It requires understanding the difference between what you earn and what you actually keep after business expenses. And when you’re applying for credit, this unpredictability raises a natural question: How do banks verify self-employed income if there’s no paycheck to point to?

The answer is more nuanced than you might expect. Banks don’t verify every applicant’s income. They don’t require a stack of documents before approval. And they don’t treat self-employed income as automatically risky, despite its variability. Instead, they use a layered approach that combines your stated income, credit history, spending patterns, and debt obligations to make a decision.

Understanding how this process works gives you the knowledge to present your financial situation honestly and effectively—and to know what to expect when you hit “submit” on that application.

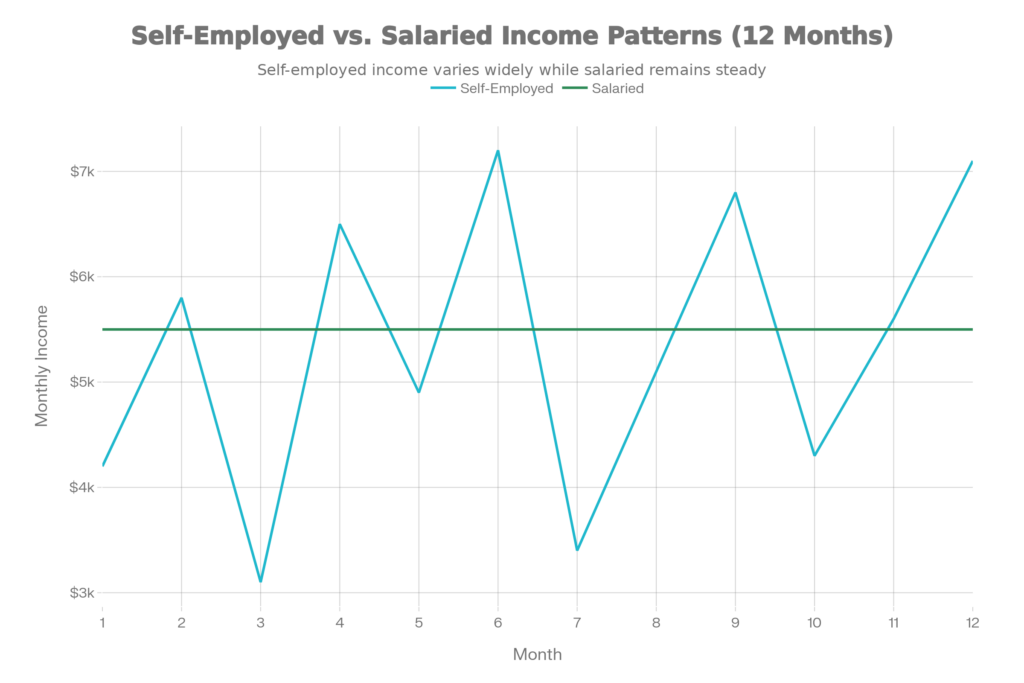

Self-employed income typically fluctuates month to month, while salaried income remains stable and predictable

On This Page

- Introduction

- Do Banks Verify Income for Credit Cards?

- Stated Income vs. Verified Income

- How Credit Card Income Verification Works

- What Counts as Income for Self-Employed Applicants

- Gross Income vs. Net Income: What Banks Care About

- When Banks Actually Verify Self-Employed Income

- How Banks Verify Self-Employed Income If Asked

- How Banks Verify Gig Worker Income for Credit Cards

- How Inconsistent Income Is Evaluated

- What Banks Do NOT Require

- Common Income Verification Mistakes Self-Employed People Make

- How Self-Employed Applicants Can Improve Approval Chances

- Frequently Asked Questions

- Conclusion

Do Banks Verify Income for Credit Cards?

Here’s the direct answer: Most of the time, no. Banks don’t verify your income during the initial approval process.

This comes as a surprise to many applicants. You’d think that before extending thousands of dollars in credit, lenders would demand proof of your income. But federal consumer credit laws require banks to assess your ability to repay—not to verify every number you provide.

When you apply for a credit card, the bank feeds your stated income into an internal risk model along with information from your credit reports. This process is similar to how freelancers apply for credit cards without income documents.

Income is a key variable in that equation, but it’s not the only one. Your credit score, payment history, existing debt levels, and the size of the credit line you’re requesting all matter. A lower credit score or unusually high debt-to-income ratio can trigger a manual review. A stated income that seems disproportionately high compared to your credit file might raise flags. But a straightforward application from someone with decent credit often sails through without anyone looking twice at the income figure.

For self-employed applicants, this is important: The bank isn’t comparing your stated income against your tax returns at approval time. They’re comparing it against behavioral patterns visible in your credit reports. If those patterns make sense—if you’re carrying debt loads consistent with that income level, if your existing credit limits align with it—you’ll likely get approved without additional verification.

Stated Income vs. Verified Income

The distinction between “stated income” and “verified income” is crucial.

Stated income is what you report on the application form. The bank takes it at face value initially. It’s the foundation of the approval decision, but it’s not independently confirmed before that decision is made. This is why the application asks you to certify that the information is true—because you’re making a statement under penalty of law, not because the bank will definitely check it.

Verified income comes into play later, usually only if something triggers suspicion. It means you’re being asked to produce documents—tax returns, bank statements, pay stubs, or business records—that prove your income is what you said it was.

| Factor | Stated Income | Verified Income |

|---|---|---|

| Documents required | None upfront | Requested if flagged |

| Approval speed | Fast | Slower |

| Common triggers | Normal applications | Manual review |

| Frequency | Most applications | Rare |

Stated income applications move quickly with minimal documentation, while verified income applications require thorough documentation and take longer to process

How Credit Card Income Verification Works

To understand income verification, you need to understand what banks are actually trying to assess: your ability to make the minimum required payment each month. This explains how banks verify self employed income by combining stated income with credit history, debt levels, and account behavior.

That’s not the same as having enough income to cover all your living expenses and debts. It’s a specific legal requirement under the Credit Card Accountability, Responsibility, and Disclosure Act (CARD Act). Before issuing a card or raising your credit limit, banks must have reasonable confidence that you can afford the minimum monthly payment on that specific card.

This is where income matters, but it’s also where it gets more flexible than people realize.

Banks use several methods to assess ability to repay: This approach is similar to how credit card companies evaluate freelancer income across different application profiles.

Credit scoring models. Your credit score already reflects your payment history over years. If you’ve consistently paid bills on time, the bank has evidence that you can manage debt. This is why credit history often matters more than income documentation in the initial decision.

Debt-to-income analysis. Banks calculate your monthly debt obligations (visible on your credit report) and compare them to your stated income. If you claim $4,000 monthly income but your credit cards and loans already show $3,500 in monthly payments, that $166 minimum payment on a new card looks risky. If you claim $6,000 monthly income with the same $3,500 in obligations, the picture changes entirely.

Income modeling. Some banks use algorithms that estimate your income based on patterns in your credit reports. If you have stable employment history visible in credit bureau records, or if your existing credit line history suggests a particular income range, the bank’s model might estimate your income even if you don’t report it. This is especially common when your stated income seems inconsistent with your credit file.

Spending analysis. After approval, banks can look at your actual spending on their card. If you claim $50,000 annual income but spend $10,000 monthly ($120,000 annually), that discrepancy will eventually trigger a review. This is rare, but it happens.

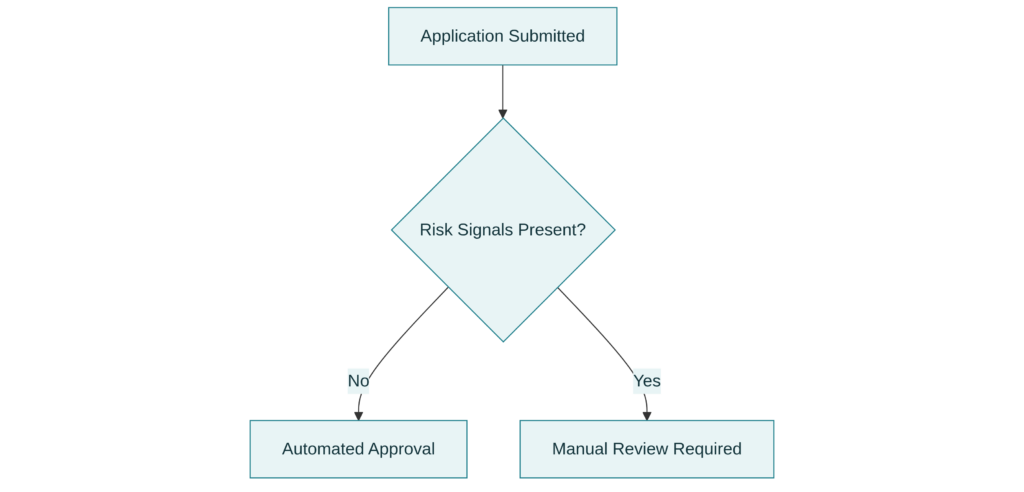

Most credit card applications are approved automatically, but suspicious patterns trigger manual review

What Counts as Income for Self-Employed Applicants

The first step in applying for a credit card is figuring out what number to report as your income.

For self-employed individuals, “income” is less straightforward than a salary. You might have:

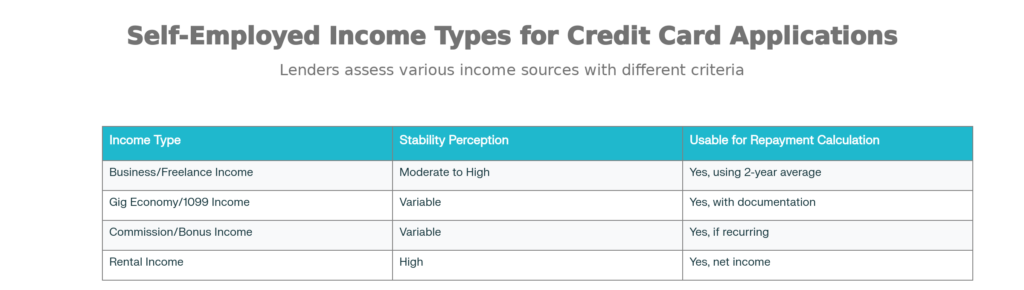

Business income. Revenue from consulting, freelancing, owning a service business, or professional practice. This is usually your primary income source. Banks generally want to see at least two years of business history. They’ll use your average net income (revenue minus legitimate business expenses) from your tax returns.

Freelance and contract income. Work performed for multiple clients where you’re issued 1099 forms (or no forms at all, in the case of cash-based or informal arrangements). Like business income, this is averaged over time. One high-income month doesn’t represent your true earning capacity.

Gig economy income. Income from platforms like rideshare services, delivery apps, or task-based work. This tends to be the most variable, but it still counts. Banks know gig income is inconsistent by nature. They’re interested in your average over several months.

Investment income. Dividends, interest, or capital gains. This counts, though it’s often stable and easy to document.

Rental income. Net income from rental properties (rent collected minus mortgage, maintenance, and other expenses). This is treated as legitimate income and is often more stable than business income.

Household or spousal income. If you’re married or live with a partner, you can potentially include their income if they have a reasonable expectation of access to it (such as it being in a joint account). Self‑employed applicants should follow general income reporting guidelines when estimating annual income for credit card applications.

Multiple income sources can strengthen a self-employed applicant’s credit card application if documented properly

What doesn’t count: Student loans, borrowed money, savings account withdrawals, or income you don’t actually have access to.

Gross Income vs. Net Income: What Banks Care About

Here’s a point that confuses many self-employed applicants: Should you report gross income or net income?

The answer depends on the application form, but it has less significance than you’d think.

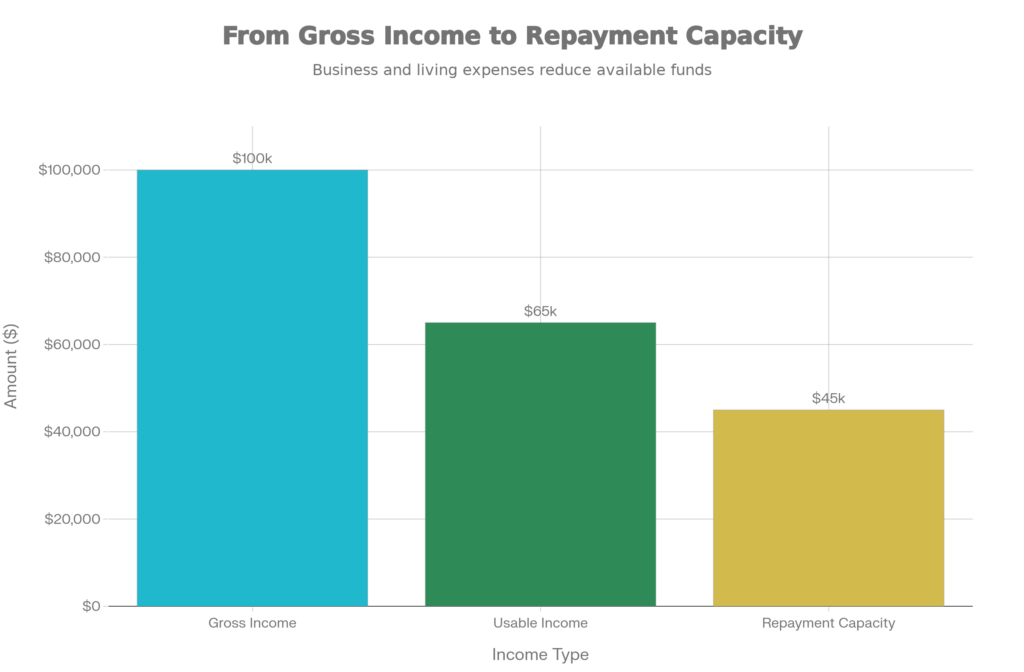

Gross income is your total revenue before any expenses or taxes. For a freelancer who billed $80,000 last year, gross income is $80,000—even if after paying software tools, insurance, workspace rent, and taxes, you took home $45,000.

Net income is what’s left after expenses: $45,000 in the above example.

Most credit card applications ask for “annual income” without specifying which type. When in doubt, credit card companies default to expecting gross annual income from self-employed applicants, averaging it over the past two years using your tax return figures.

But here’s what matters more: Banks want to know your repayment capacity, not the mathematical niceties of your tax filings.

If you report $80,000 gross income but your bank statements show you’re spending $50,000 monthly on the business and living expenses combined, that’s a red flag. The bank wants to see available cash—not accounting figures.

This is why bank statement analysis has become more common in lending. A bank can look at your actual deposits and see real cash flowing into your account. They can estimate your true available income by looking at months of transaction history. If you claim $6,000 average monthly income, they can verify whether deposits actually average around that figure.

Banks focus on repayment capacity—what’s left after expenses—rather than just gross income figures

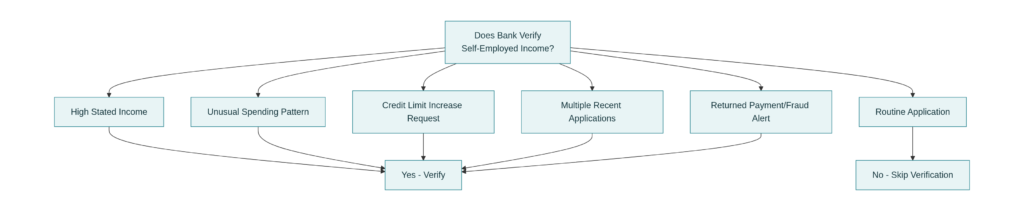

When Banks Actually Verify Self-Employed Income

The critical question for self-employed applicants: When will the bank actually ask to see proof?

The answer is: rarely during initial approval, but it can happen afterward.

Verification typically occurs in these scenarios:

High stated income. If you claim an unusually high income relative to your credit history, someone will want proof. A 25-year-old with three credit cards claiming $200,000 annual income will likely face a financial review.

Rapid income changes. If you apply for two cards within a month and claim $50,000 income on the first and $150,000 on the second, that inconsistency triggers scrutiny.

Credit limit increase requests. When you ask to raise your credit limit, the bank may ask for updated income documentation, especially if the requested limit would exceed what your stated income typically supports.

Unusual spending behavior. If you quietly spend $15,000 a month on a card when your stated income was $3,000 monthly, algorithms flag this for review. This is particularly common with high-end cards that attract more scrutiny.

Multiple applications in short timeframe. Applying for five credit cards in two weeks raises fraud detection flags. Banks share information, and a flurry of applications signals either fraudulent activity or someone dangerously overextending themselves.

Account behavior issues. Returned payments, missed payments, or patterns suggesting financial distress trigger automatic reviews.

Periodic income verification requests. Some card issuers periodically ask existing cardholders to confirm or update their income. These are often low-pressure requests that you can ignore without penalty, though responding can help you qualify for credit line increases.

Banks typically verify income only when specific red flags appear, not during routine applications

How Banks Verify Self-Employed Income If Asked

If your account enters a manual review or if the bank proactively asks for income verification, here’s what they typically request:

Recent tax returns. Usually the past two years. For self-employed individuals, banks look at Schedule C (Profit or Loss from Business) or the business section of your return, where your net profit or loss is reported. They’re not forensic auditors; they’re looking for a reasonable number that matches what you claimed. Be honest: if you claimed $60,000 annual income but your tax returns show $35,000 average net profit, there will be consequences.

Bank statements. Three to six months of statements from business and personal accounts. The bank is verifying that the income you claimed actually flows into your accounts. They’re looking for deposit patterns and consistency.

Profit and loss statements. Year-to-date or annual P&L statements from your business accounting system. This is particularly useful if your most recent tax returns are older and don’t reflect current business performance.

Business account information. The name and account type of your primary business account, to cross-reference deposits.

Invoice records or contracts. Evidence of ongoing client relationships, retainer agreements, or project contracts showing future income stability.

Schedule C excerpt. You can provide just the relevant portion of your tax return rather than your entire filing.

For card issuers, the pattern matters more than exact figures. They want to see that income deposits happen consistently, that the amounts roughly align with what you claimed, and that the income appears sustainable.

One important caveat: Some people fear sharing tax returns with lenders because they’ve minimized their income through aggressive deductions to lower tax bills. This creates a real problem. If you claimed $60,000 income on your card application but your tax return shows $35,000, that’s fraud—or at minimum, it looks like fraud. The bank can and will close your accounts over this.

How Banks Verify Gig Worker Income for Credit Cards

Banks verify gig worker income differently because gig-based earnings often fluctuate from month to month. Unlike salaried applicants with predictable paychecks, gig workers often have irregular payment schedules and varying amounts of income depending on workload and demand.

When reviewing an application, lenders typically look for consistency over time—steady deposits, repeat clients, or a clear upward or stable trend in monthly income. Documentation plays a larger role since most gig workers don’t receive formal pay stubs; instead, banks may request bank statements, tax returns, or digital payment summaries to confirm the source and reliability of earnings, which is a key part of gig worker income verification for credit cards. This helps lenders gauge whether the applicant can manage regular credit payments despite irregular cash flow.

A strong credit score still carries significant weight in the decision, as it reflects the applicant’s past record of managing debt responsibly, complementing the income verification process and providing a fuller picture of overall creditworthiness.

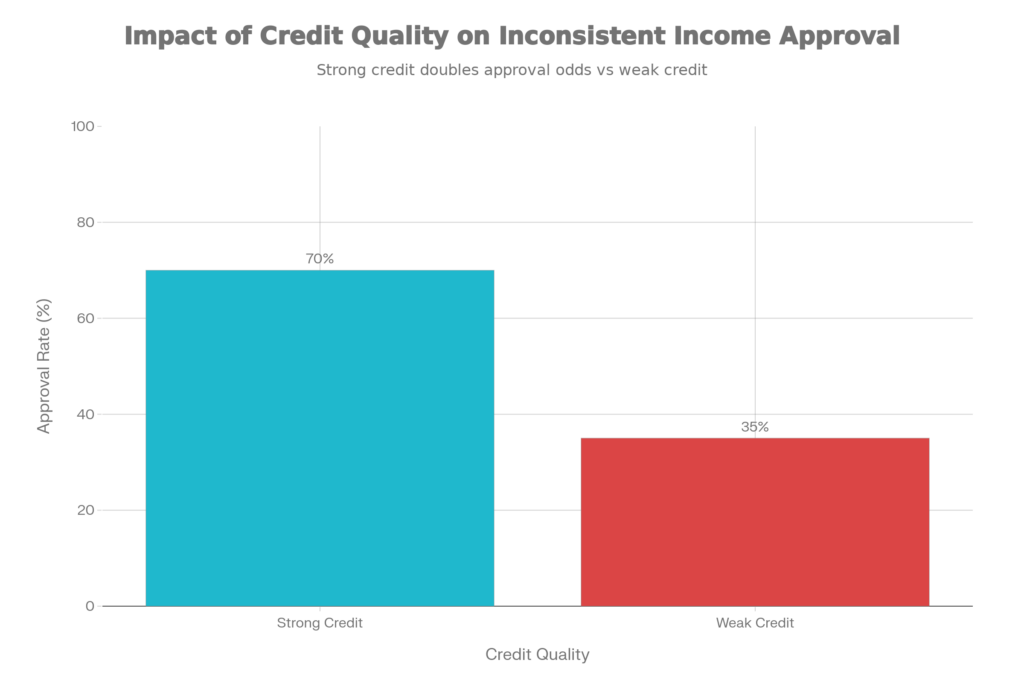

How Inconsistent Income Is Evaluated

Self-employed income being variable is normal. Banks know this. It doesn’t automatically disqualify you.

What matters is how banks interpret that variability in context.

With strong credit history. If you have five years of on-time payments, low credit utilization, and a solid credit score, the bank is confident in your ability to manage debt despite income volatility. You’ve proven it through behavior. A dip in income one month is less concerning because your track record suggests you’ll recover.

Strong credit history significantly improves approval odds even with inconsistent self-employed income

With weak credit history. If you have recent late payments, high credit utilization, or a low credit score, variable income becomes a bigger concern. The bank has less evidence that you’ll manage a new credit obligation responsibly. A spotty track record combined with inconsistent income looks riskier.

This is also why income averages matter. Banks don’t look at your best month or worst month; they want your realistic expected monthly income. If you made $8,000 one month, $3,000 the next, and $5,500 the third, your average is roughly $5,500—and that’s the number the bank uses for ability-to-repay calculations. It’s a more honest picture than claiming your best-case scenario.

What Banks Do NOT Require

Clearing up the myths is important here. Here’s what banks typically do not do when evaluating self-employed applicants:

They don’t call your clients. Banks don’t verify that you actually have the projects or clients you’ve listed. They don’t phone businesses to confirm you work there.

They don’t require a fixed monthly paycheck. You don’t need a W-2 or consistent monthly deposits to get approved. Many self-employed applicants get approved on stated income alone, with no documentation requested upfront.

They don’t demand perfect income stability. A credit card issuer won’t reject you simply because your income fluctuates. Gig workers, seasonally employed people, and commission-based workers get credit cards regularly.

They don’t require a specific minimum income for basic cards. While some premium cards have minimum income thresholds (sometimes $50,000 or more), basic credit cards have no published minimum. Your approval depends on ability to cover the minimum payment, not on hitting a specific income target.

They don’t conduct forensic tax audits. They’re not looking for hidden income or complex deductions. They want a reasonable income number that explains your credit behavior.

Common Income Verification Mistakes Self-Employed People Make

Understanding what not to do is as important as understanding the process:

Overstating income significantly. Claiming $100,000 when you make $60,000 might get you a higher credit limit temporarily, but if you’re ever reviewed, the discrepancy with your tax returns will be obvious. The bank will lower your limits or close your accounts. In extreme cases, intentional fraud can lead to criminal charges.

Using your best month as representative. If you had one exceptional month earning $15,000 but typically make $5,000 monthly, don’t claim the $15,000 as your annual income. Banks understand that exceptional months exist. They want your realistic average.

Mixing personal and business finances. When personal and business money flows through the same account, it becomes hard to prove actual business income. Banks can’t easily verify your true self-employment earnings. Maintain separate accounts whenever possible.

Applying too early in your business. If you’ve been self-employed for three months, you don’t have sufficient history to support a credible income claim. Most banks prefer at least a year or two of business history, ideally with tax returns showing you’ve sustained the income.

Not having documentation ready. Don’t guess or eyeball your numbers. Have your tax returns, profit and loss statements, and recent bank statements accessible before you apply. This makes the process faster if verification is requested.

How Self-Employed Applicants Can Improve Approval Chances

Several concrete steps improve your odds of approval and smooth approval process:

Calculate your income responsibly. Use your average net income over the past two years from your tax returns. Don’t round up significantly or use best-case projections. For newer businesses without two years of history, estimate conservatively based on actual performance to date.

Manage your debt-to-income ratio. Calculate your total monthly debt payments (loans, credit cards, rent or mortgage) and divide by your estimated monthly income. Keep this ratio below 35% if possible, though credit card issuers aren’t held to a specific DTI threshold like mortgage lenders are. A lower DTI always improves approval odds.

Build credit history. If you’re new to self-employment or have limited credit history, start with a secured card or become an authorized user on someone else’s account. Establish a track record of on-time payments. Credit score improvements happen quickly once you demonstrate reliability.

Keep organized records. Maintain clear business accounting, separate business and personal accounts, and save all relevant documents. If you’re ever asked for verification, organized records make the process fast and painless. Disorganized finances raise red flags.

Be consistent on applications. If you apply for multiple cards over time, use roughly the same income figure unless your actual earnings changed substantially. Major unexplained income swings between applications trigger reviews.

Apply for appropriate credit limits. Don’t request a $10,000 limit if your income only justifies a $2,500 limit. Start with a realistic limit that matches your income and debt situation. You can always request increases later as your income grows and your credit improves.

Consider your timing. Apply when your business is on solid footing, preferably after at least one or two years of stable performance. If you just started your business, waiting a year or two improves approval odds significantly.

Frequently Asked Questions

How do banks verify self-employed income for credit cards?

Most banks don’t verify initially. They assess your ability to repay using stated income, credit history, and debt-to-income ratio. If something seems off—unusually high income, rapid spending spikes, inconsistent applications—they may request tax returns, bank statements, and business records.

Do banks check tax returns for credit card applications?

Not for initial approval. But if your account enters manual review—often triggered by unusual spending behavior, high stated income relative to credit history, or credit limit increase requests—banks can request tax returns to verify your income matches what you claimed.

Can I get approved without income proof?

Yes. Most applicants are approved without providing any documentation. The bank uses your stated income and credit report to make the decision. Documentation only comes into play if verification is triggered.

What if my income is inconsistent?

Inconsistent self-employed income is expected and normal. Banks understand this. They’ll evaluate you on your average income over time, combined with your credit history. Strong credit history makes inconsistent income less of a problem.

Can I include household income?

Yes, if you’re over 21 and it’s income to which you have reasonable expectation of access. This typically means a spouse’s income in a joint account. You can’t just claim someone else’s income without access to it.

What happens if my stated income doesn’t match my tax return?

If there’s a significant discrepancy and the bank discovers it (usually during a financial review), they can lower your credit limits or close your accounts. Intentionally lying about income is fraud and can result in criminal charges, though this is rare in practice.

How long does verification take?

If no verification is needed, approval happens in minutes to days. If verification is requested, the process can take one to three weeks, depending on how quickly you submit documents and how backed up the review department is.

Should I report gross or net income?

Most credit card applications asking for “annual income” from self-employed people expect gross revenue from your business, averaged over two years using tax return figures. If the application asks for something more specific (“net income,” “disposable income”), follow those instructions.

Conclusion

The process of getting approved for a credit card as a self-employed individual is less mysterious than it seems. Banks aren’t trying to catch you in a lie or trap you with undisclosed requirements. They’re trying to assess, with reasonable confidence, whether you can make the minimum monthly payment on a credit card.

For most applicants with decent credit history, that assessment happens automatically, using your stated income without any verification. Your credit report already tells the bank whether you’ve managed debt responsibly. If those two factors—your stated income and your credit history—align reasonably well, you get approved. Knowing how banks verify self employed income allows self‑employed applicants to report income honestly and avoid issues during manual reviews.

The key is honesty. Report your income realistically based on what you actually earn and what your tax returns show. If income verification ever comes up, honest numbers will pass. Inflated numbers create problems you don’t want to face.

Your employment status—whether you’re salaried, self-employed, or a gig worker—matters less than you’d think. What matters is your ability to manage credit responsibly, which your credit history demonstrates far better than employment type ever could.

Disclaimer:

This content is for educational purposes only and does not constitute financial, legal, or tax advice. Credit card policies vary by issuer and individual circumstances.