Introduction

How credit score affects credit card approval for freelancers is one of the most common questions self‑employed professionals ask when applying for a new credit card in the United States. .For someone earning a steady W-2 paycheck, credit card approval is often straightforward. A bank checks your credit report, sees a decent score and regular income, and typically approves you within days. For freelancers and self-employed professionals, the process feels entirely different.

This disparity exists for a simple reason: banks see freelance income as inherently riskier than salaried employment. Your paycheck doesn’t arrive automatically on the 15th and last of every month. Some months you earn significantly more; others, your pipeline runs dry. That variability creates genuine uncertainty from a lender’s perspective. So when a freelancer applies for a credit card, lenders don’t just look at your credit score—they examine the entire financial picture to assess whether you can reliably make monthly payments.

Your credit score, though, remains the most important starting point. It’s often the first gate you must pass. This article explains exactly how credit scores factor into freelancer credit card approval, what scores you realistically need, and what you can do to improve your chances of getting approved.

On This Page

- Introduction

- How Credit Score Affects Credit Card Approval for Freelancers

- Credit Score Ranges and Risk Perception

- Minimum Credit Score Ranges Freelancers Typically Need

- Credit Score vs Credit History Length

- Payment History and Its Impact on Freelancer Approval

- Credit Utilization and Existing Debt

- Thin Credit Files and New Freelancers

- Score Alone vs Full Credit Profile Review

- Common Credit Score Myths Freelancers Believe

- Common Credit Score Mistakes Freelancers Make

- How Freelancers Can Improve Credit Score for Approval

- Does Credit Score Work Differently for Gig Workers?

- Frequently Asked Questions

- What credit score do freelancers realistically need to get approved for a mainstream credit card?

- Can a high income offset a low credit score?

- Can freelancers with thin credit files get approved?

- Does being self-employed automatically hurt my credit card approval chances?

- How fast can freelancers improve their credit scores?

- Conclusion

- Disclaimer

How Credit Score Affects Credit Card Approval for Freelancers

Your credit score is a three-digit number, typically ranging from 300 to 850, that summarizes your borrowing and repayment history. Lenders use it as a risk proxy. A higher score suggests you’ve reliably paid debts on time; a lower score suggests you’ve missed payments, carried high balances, or rarely borrowed money at all.

For freelancers, credit card issuers interpret your score the same way they do for anyone else: as evidence of your financial responsibility. The score itself doesn’t care whether you’re self-employed or salaried. Your employment status is not part of the score calculation. What matters is whether you’ve paid your bills on time, how much available credit you’re using, how long you’ve held credit accounts, and how many different types of credit you’ve managed.

That said, your credit score is only the first lens through which issuers evaluate you. Especially for freelancers, the bank will also want to verify that your stated income is real and stable. They may ask for tax returns, bank statements, or invoices to confirm you actually earn what you claim. A thin credit file—one with few accounts or limited history—can also trigger more scrutiny, because the bank has less data to predict your behavior.

The key distinction: your credit score is a historical grade based on past credit behavior. Your freelance income is a forward-looking question about whether you’ll be able to afford next month’s payment.

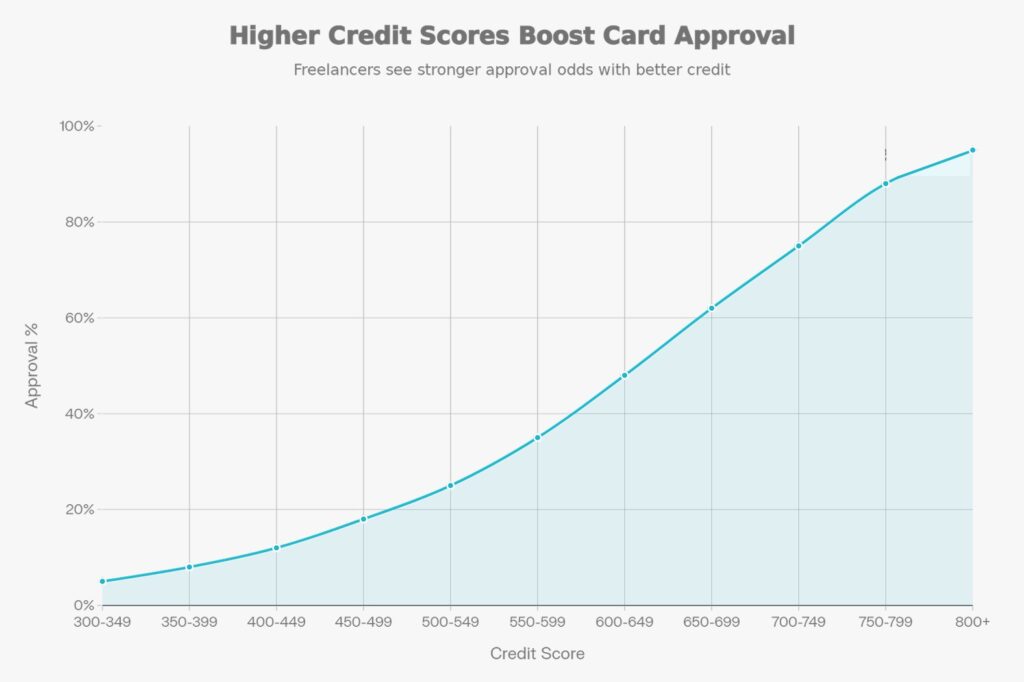

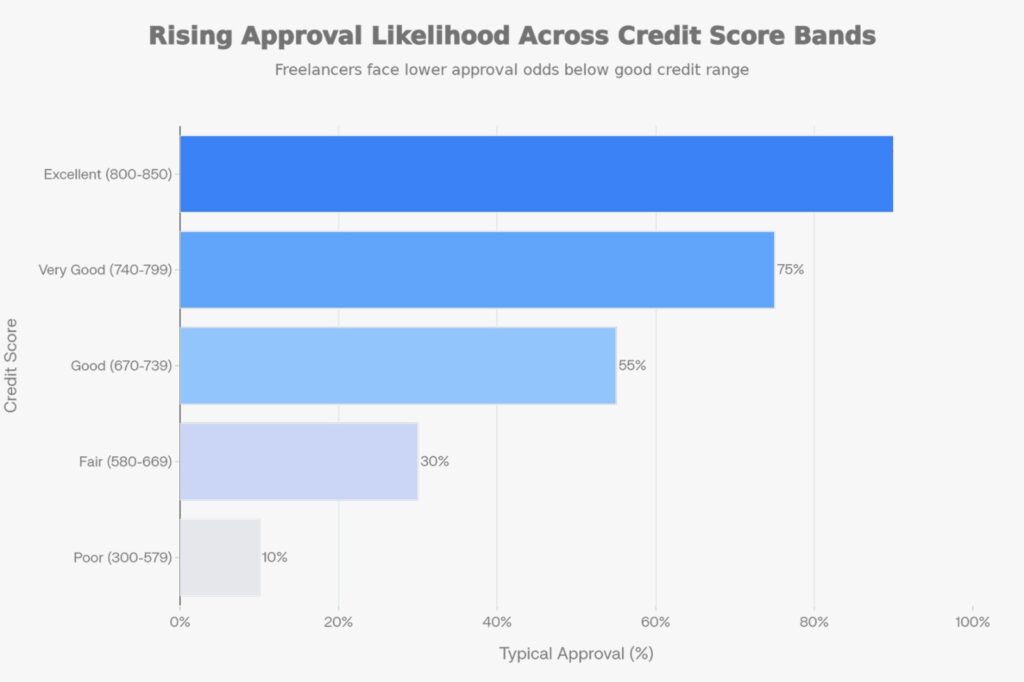

Credit Score Ranges and Risk Perception

The following table outlines how major credit bureaus categorize credit scores and what each range typically signals to credit card issuers:

| Credit Score Range | Category | Lender Risk Assessment | Typical Freelancer Approval Likelihood |

|---|---|---|---|

| 800–850 | Exceptional | Minimal risk; excellent borrower | Very high; likely best rates |

| 740–799 | Very Good | Low risk; reliable borrower | High; favorable terms likely |

| 670–739 | Good | Moderate risk; acceptable borrower | Moderate to high; standard terms |

| 580–669 | Fair | Higher risk; spotty history | Low to moderate; may require explanation |

| 300–579 | Poor | High risk; frequent defaults | Very low; secured card or co-applicant likely |

The average American FICO score hovers around 715, which falls into the “good” range. But for freelancers, even a good score alone may not be enough. Issuers often apply stricter income verification standards to self-employed applicants, so your score must be accompanied by clear proof of income stability. Understanding how credit score affects credit card approval for freelancers is critical because lenders rely on past credit behavior when freelance income is variable.

Minimum Credit Score Ranges Freelancers Typically Need

The short answer: it depends on the issuer and the card. But there are reasonable benchmarks. This section further clarifies how credit score affects credit card approval for freelancers, especially when income is variable and documentation is limited.

For entry-level or mainstream credit cards, most issuers want to see a credit score of at least 650 to 700. Some banks may approve applicants with scores in the 620–650 range, but those approvals typically come with higher interest rates, lower credit limits, or both. Below 620, approval becomes significantly less likely without either a secured card (where you deposit collateral) or a co-applicant.

For premium or rewards cards, issuers generally expect scores above 740, often in the 750+ range, because these cards offer better benefits and the issuer wants to minimize risk.

Why might freelancers need slightly higher scores than salaried employees at the same income level? Because lenders view self-employment as an inherent risk factor. A score that would comfortably approve a salaried employee might put a freelancer in the borderline category, requiring more documentation or resulting in a decline if other factors don’t align.

This doesn’t mean freelancers with scores below 700 can’t get approved. Thousands do every day. But you’ll likely face one of three scenarios: approval with higher interest rates, approval with a lower credit limit, or a requirement to provide additional income documentation. The clearer your income picture, the better your chances even with a below-700 score. For a deeper breakdown of the minimum credit profile freelancers need to qualify for credit cards, including score ranges and history requirements, see this detailed guide.

Credit Score vs Credit History Length

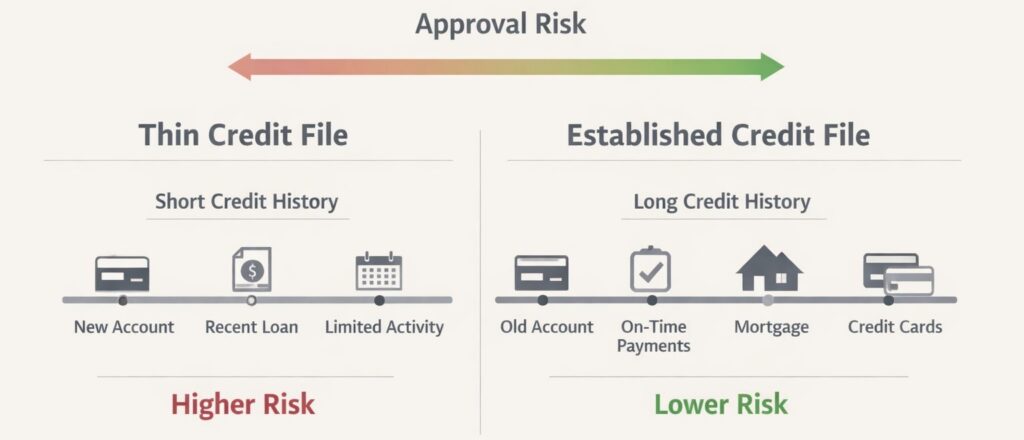

One challenge unique to many freelancers is what’s known as a “thin credit file.” If you only recently went independent and don’t have a long history of managing credit, your credit report might contain few accounts—perhaps just a credit card and a car loan. Credit bureaus like to see more accounts to create a reliable score. Reports with fewer than five accounts are often classified as thin.

A thin file creates a problem: even if you have a decent score, there’s not enough data for the algorithm to confidently predict your future behavior. You may have a 680 score, but with only two accounts in your history, a lender has limited confidence in what that score represents. They’ll ask more questions, request more documentation, and may deny you to avoid the uncertainty.

For newer freelancers building credit history, this is a real bottleneck. The solution isn’t quick, but it’s straightforward: accumulate more credit accounts over time and keep all payments on time. This might mean starting with a secured credit card (where you put down a cash deposit as collateral), using it responsibly for a year, then graduating to an unsecured card. It’s not glamorous, but it works.

| Credit History Scenario | Time in Business | Account Diversity | Typical Approval Challenge |

|---|---|---|---|

| New freelancer, thin file | < 1 year | 1–2 accounts (credit card only) | May be denied; secured card advised |

| Thin file, some history | 1–3 years | 2–3 accounts (card, loan) | May be approved; higher rates likely |

| Established freelancer | 3+ years | 4+ accounts (cards, loan, installment) | Standard approval process likely |

| Long history, diverse accounts | 5+ years | 5+ accounts + mortgage/auto | Best approval odds; competitive rates |

The longer you successfully manage credit as a freelancer, the less weight any single missed payment or high balance will carry. A thin file magnifies the damage of a late payment; an established credit history dampens it.

Payment History and Its Impact on Freelancer Approval

Of all the factors that make up your credit score, payment history is the heavyweight champion. It accounts for 35 percent of your FICO score—more than any other factor.

This is both good news and bad news for freelancers. Good news: if you have a spotless payment history, that’s a powerful signal to lenders that you’re reliable even if your income fluctuates. Bad news: a single late payment creates immediate damage, and the damage is often worse for freelancers than for salaried employees.

Here’s why: if you have a thin credit file (common among newer freelancers) and you make one 30-day late payment, that late payment represents a larger proportion of your total credit history. The algorithm has fewer positive data points to offset it. For someone with a decade-long credit history and dozens of on-time payments, a single 30-day late payment barely registers. For someone with three years of history and six accounts, that same late payment is a much bigger deal.

Late payments don’t hit your credit report until you’re at least 30 days past due. However, you’ll typically be charged a late fee as soon as you’re one day late. The key threshold is day 30. Before that, you might be able to call your card issuer, explain the situation (especially important if it’s your first miss), and sometimes get the fee waived. After day 30, you’re in the credit report system.

Once a late payment is reported, it stays on your credit report for seven years, though its impact diminishes over time. A late payment from six months ago hurts much less than a late payment from last month. But it still appears. In addition to credit history, lenders often request documentation to understand how banks verify self‑employed income before approving a credit card.

For freelancers with variable income, the most common scenario triggering late payments is a slow month followed by the rationalization that you’ll catch up next month. That’s exactly when you shouldn’t fall behind, because lenders view even one late payment as a crack in the foundation of your creditworthiness.

| Payment Behavior | Impact on Freelancer Approval | Risk to Credit Score | Recovery Timeline |

|---|---|---|---|

| All on-time payments (24+ months) | Strong approval signal; competitive rates | Builds score; improves approval odds | N/A (positive factor) |

| 1–2 late payments (30–60 days, 2–3 years ago) | Manageable; approval likely but rates higher | Minor damage; diminishes over time | 2–3 years visibility decline |

| Recent late payment (< 6 months) | Significant barrier; may be denied or require explanation | Severe damage; major score reduction | 6–12 months minimum |

| Multiple late payments (within 12 months) | Likely decline unless strong income proof | Severe damage; thin file hit hardest | 12–24 months typical recovery |

| Current delinquency (30+ days overdue) | Approval unlikely; secured card necessary | Catastrophic impact | 7-year reporting period |

Credit Utilization and Existing Debt

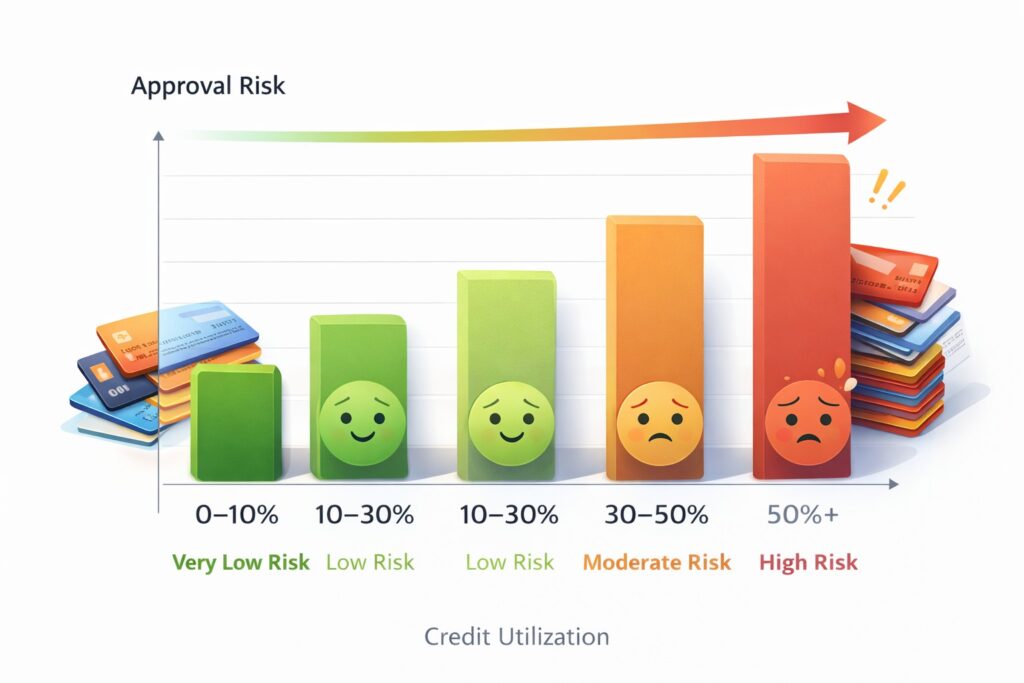

Credit utilization ratio is the second-largest factor in your credit score, accounting for roughly 30 percent. It’s calculated simply: divide your total credit card balances by your total available credit limits. If you have a credit limit of $10,000 and carry a $3,000 balance, your utilization is 30 percent.

For freelancers applying for a new credit card, your current utilization ratio matters significantly. Here’s why: lenders use utilization as a proxy for financial stress. A low ratio (below 30 percent) suggests you’re managing credit responsibly—you have available room if you need it, but you’re not dependent on it. A high ratio (above 50 percent) suggests you’re either over-leveraged or living paycheck to paycheck, both red flags for a lender.

The relationship between utilization and approval gets more complex when your income is variable. A lender sees that you’re carrying a high balance during a slow month and may worry that you lack cash reserves. If your next month is strong but you don’t immediately pay down that balance, the lender’s concern grows. A freelancer with 70 percent utilization and variable income looks riskier than a salaried employee with the same utilization, because the freelancer’s steady income assumption doesn’t apply.

To improve your approval odds, aim to bring your overall utilization below 30 percent before you apply for a new card. This is especially important if you have a borderline credit score (650–700). A few months of lower balances can make the difference between approval and denial.

| Credit Utilization Ratio | Lender’s Risk Perception | Effect on Approval Likelihood | Recommendation for Freelancers |

|---|---|---|---|

| 0–10% | Excellent; underutilized credit | Best approval odds | Ideal; demonstrates discipline |

| 10–30% | Good; healthy balance | Strong approval odds | Target this range before applying |

| 30–50% | Fair; acceptable but noted | Moderate approval odds | May require income explanation |

| 50–70% | Concerning; potential stress | Approval uncertain; higher rates | Pay down before applying |

| 70%+ | High risk; overleverage | Likely denial or secured card | Immediate action needed |

A practical note: if you’re planning to apply for a new card, spend two to three months reducing your balances on existing cards to below 30 percent utilization. The improvement to your approval odds is worth the effort, and you’ll also improve your credit score during that time.

Thin Credit Files and New Freelancers

Starting freelance work often means starting with a limited credit file. You’ve had a job for ten years, built good credit, then left to start a business. Did that help your credit file? Not directly. Your employment status doesn’t appear on your credit report. But going independent often coincides with not taking on new credit, which means your credit file doesn’t grow with new accounts.

A thin credit file isn’t a barrier to approval, but it is a complication. Lenders have less historical data to assess your reliability. A single negative mark (like a late payment) looms larger. A short history of all on-time payments is promising but not conclusive—maybe you’ve just been lucky or responsible for a brief window, not long enough for the bank to be sure.

For freelancers with thin files, realistic expectations matter. You might not qualify for premium credit cards with excellent rewards and high limits. You might get approved at lower credit limits initially. That’s normal. The path forward is straightforward: get approved for a basic card, use it responsibly for a year or two, and build your file. Once you have four to five active accounts and a few years of clean payment history, you’ll qualify for better offers.

If you’re completely new to credit as a freelancer—no credit history at all—a secured credit card is the standard entry point. You deposit $500–$2,500 with the issuer, and that becomes your credit limit. You use it like a normal card, and as long as you pay on time, after 12–18 months, many issuers will convert it to an unsecured card and refund your deposit. This is not a permanent solution; it’s a bridge to building a real credit file.

Score Alone vs Full Credit Profile Review

Here’s a critical distinction that many freelancers miss: credit card issuers don’t make approval decisions based on your score alone.

Your score is a checkpoint. It tells the issuer whether you’re worth reviewing further. But the actual approval decision involves a full review of your application: your stated income, your existing debts, your payment history pattern, your credit file diversity, and sometimes your bank account balance or savings.

For mainstream applications and cards, this full review happens automatically, and the score is weighted heavily. A 750 score with a clean payment history almost always gets approved. A 620 score with a history of missed payments usually gets declined.

But there are gray zones. What if you have a 680 score (borderline good), a spotless 24-month payment history, but you’re claiming $35,000 annual freelance income and the bank suspects you haven’t documented that adequately? The issuer might run a more detailed review. They might ask for tax returns or bank statements. They might decline you not because of your score, but because they can’t confidently verify your income.

Conversely, what if you have a 710 score, but your credit file shows you missed a payment two months ago while your bank statements show erratic deposits and high turnover? The issuer might decline you despite your score being above the typical threshold, because the full profile suggests financial instability. Lenders may also evaluate whether your earnings come from client‑based income or short‑term contract work, as different income patterns affect perceived stability.

The score is the filter; the profile is the decision.

| Scenario | Credit Score | Full Profile Signal | Likely Outcome |

|---|---|---|---|

| High score + clean history + verified income | 750+ | All positive; stable freelancer | Approval; best rates |

| Good score + thin file + unverified income | 700 | Uncertainty; needs documentation | Conditional approval or delay |

| Fair score + clean recent history + strong income proof | 650 | Mixed; recent positive behavior | Approval likely; standard rates |

| Fair score + recent late payment + income unverified | 680 | Red flags; recent concern + uncertainty | Likely decline or secured card |

| Low score + excellent recent history + strong income | 620 | Very mixed; hard to interpret | Decline likely; secured card advised |

Common Credit Score Myths Freelancers Believe

Myth 1: “If I make more money, my credit score will improve.”

This is false. Your income doesn’t appear on your credit report, so it can’t factor into your score calculation. A freelancer earning $100,000 annually can have an excellent, good, or poor credit score. A freelancer earning $30,000 can have the same range. What affects your score is how you manage credit, not how much money you make. That said, higher income gives you more capacity to pay bills on time, which indirectly helps your score.

Myth 2: “One really good month of income will help me get approved.”

Wrong. Credit card issuers want to see sustained income, typically averaged over the past two years. One good month proves nothing. Lenders assume freelancers have variable income (which is true), so they average it out or ask for tax returns showing consistent year-to-year earnings. One month of $15,000 revenue after months of $4,000 doesn’t change the lender’s assessment.

Myth 3: “If I have a high credit score, income doesn’t matter.”

Partially false. A high credit score improves your approval odds significantly, but it doesn’t eliminate the income requirement. Lenders still want to verify that you can reasonably afford the card’s credit limit and make regular payments. A freelancer with a 780 score and unverifiable income might be declined. A salaried employee with the same score and unverifiable income would also be declined. The difference is that for salaried employees, income verification is simpler (just a pay stub). For freelancers, it’s more involved.

Myth 4: “My freelance income is proof of creditworthiness.”

No. Your income is proof that you have money; it’s not proof that you’ll use it to pay your debts. Credit scores and credit history are proof of creditworthiness. You can have a strong income but a poor credit score if you’ve missed payments, carried high balances, or defaulted in the past. Conversely, you can have a modest income and an excellent credit score if you’ve consistently paid your obligations on time.

Common Credit Score Mistakes Freelancers Make

Mistake 1: Missing a payment because cash flow is tight.

This is the biggest trap. You have a slow month, your invoices haven’t been paid yet, and your credit card payment is due. You skip it, planning to catch up next month. What happens: after 30 days, the late payment hits your credit report. Your score drops—often by 50–100 points if you have a thin file. The issuer may call. Your new credit card applications will likely be declined for the next six months.

The better approach: if a payment is coming due and cash is tight, call the issuer. Explain that you’re self-employed, you have slower months, and you need a temporary payment plan. Many will work with you. This isn’t reported to credit bureaus. It keeps your credit intact and shows the issuer you’re proactive, which matters if you want to build a long-term relationship.

Mistake 2: Carrying high balances on multiple cards.

If you’re using your personal credit cards to manage business cash flow—common among freelancers—high balances build up fast. You load business expenses on your card, planning to reimburse yourself from the next invoices. But invoices run late. Now you’re carrying 60 percent utilization across three cards. Your score drops. You apply for a new card and get denied because lenders see you as overleveraged. A year later, when you finally pay down those balances, you realize you could have been approved if you’d managed utilization better.

The better approach: separate personal and business finances as much as possible. If you need cards for business expenses, get a dedicated business card. If you’re using personal cards, pay them down to below 30 percent utilization each month, even if you have to dip into business savings to do it. The credit score benefit is worth the cash flow timing shuffle.

Mistake 3: Applying for multiple cards in quick succession.

Each credit application triggers a hard inquiry on your credit report. One inquiry is normal. Two inquiries in three months signals to lenders that you’re aggressively seeking credit—a potential red flag. Multiple inquiries can drop your score by 5–10 points per inquiry, and lenders may interpret the pattern as financial desperation.

Better approach: space your applications. If you don’t get approved for one card, wait three to six months, improve your credit profile (pay down balances, build more history), and try again. If you’re planning to apply for multiple cards (say, for different business and personal purposes), do it within a short window (same week), so the inquiries bunch together rather than appearing scattered over months.

Mistake 4: Not checking your credit report for errors.

Credit bureaus make mistakes. Closed accounts might still show as open. A paid-off loan might still show as active. A late payment from someone else with a similar name might end up on your report. If you don’t check, you don’t know.

Better approach: pull your credit report annually (you’re entitled to one free report per year from each bureau). Look for errors. If you find one, dispute it with the bureau. Corrected errors can improve your score by dozens of points, which might be the difference between approval and denial.

| Mistake | Credit Score Impact | Effect on Approval | Prevention Strategy |

|---|---|---|---|

| Missed payment (30+ days late) | 50–100 point drop | Likely decline for 6–12 months | Call issuer; negotiate plan |

| High utilization (50%+) across cards | 20–50 point drop | Lower approval odds; higher rates | Pay balances monthly; below 30% target |

| Multiple applications (3+ in 3 months) | 5–10 points per inquiry | Signals financial stress; decline risk | Space applications 3–6 months apart |

| Credit report errors (uncorrected) | Variable; often 10–50 points | May cause unfair decline | Check annually; dispute errors |

| Maxing out individual cards | 30–60 point drop | Major risk signal even if total utilization okay | Monitor per-card limits; rotate usage |

How Freelancers Can Improve Credit Score for Approval

If your credit score is lower than you’d like, here’s the realistic path to improvement.

Start with payment consistency. Pay every bill on time, every month, without exception. This is more important than anything else. Even a modest score of 650 with 24 months of on-time payments will usually get approved for a mainstream card. A 720 score with recent late payments might be declined.

Pay down high balances. Focus on getting your overall utilization below 30 percent. If you have a credit card with a $3,000 balance and $5,000 limit, you’re at 60 percent. Paying it down to $1,500 (30 percent) improves your score and your approval odds.

Don’t close old accounts. If you have a credit card you’re not using, leave it open. Account age helps your score. The average age of your accounts factors in. Closing your oldest card actually hurts your score. The exception: if the card charges an annual fee you don’t want to pay, closing it is reasonable, but know the short-term score hit will come.

Build account diversity. Lenders like to see a mix of credit types: credit cards (revolving credit) and loans (installment credit). If you only have credit cards, consider a small personal loan or a store card. Just be strategic—don’t take on unnecessary debt to build diversity. One extra account is enough.

Timing matters. If you’re planning to apply for a new card, spend two to three months improving your profile before you apply. Pay down balances. Make all payments on time. Let new positive payment history accumulate. Then apply. This dramatically improves your approval odds.

Monitor your reports. Pull your free credit report from each bureau annually. Dispute any errors. Check that old negative items are aging off (accounts with late payments should drop off after seven years).

The timeline for meaningful improvement depends on your starting point. If your only issue is a 30-day late payment from two years ago, and everything else is clean, you may get approved now. If you have recent late payments and high utilization, realistic improvement takes six to twelve months of clean behavior. If you have multiple recent delinquencies, you’re looking at 18–24 months before mainstream approval is realistic.

Does Credit Score Work Differently for Gig Workers?

Credit scores work the same way for gig workers as they do for freelancers and salaried applicants, because the score itself is based on credit behavior rather than employment type. Payment history, credit utilization, account age, and recent credit activity are calculated using the same scoring models regardless of how income is earned. However, lenders often interpret risk differently when reviewing gig worker applications. Because gig income can fluctuate more sharply from month to month, issuers may rely more heavily on credit score signals to assess consistency and reliability.

Strong on-time payment history and low credit card balances can help offset concerns about variable income. Gig workers with thin credit files or recent late payments may face additional scrutiny, even if their income is sufficient. In practice, this means maintaining a solid credit score becomes especially important. when applying for credit cards with non‑traditional income, especially for those exploring credit cards for gig workers, as it helps reassure lenders that the applicant can manage credit obligations despite uneven cash flow.

Frequently Asked Questions

What credit score do freelancers realistically need to get approved for a mainstream credit card?

Understanding how credit score affects credit card approval for freelancers helps set realistic expectations before applying for any new credit card. Most mainstream card issuers want to see a score of at least 650–700. Some approve scores as low as 620. Above 740, approval is very likely unless other factors (unverified income, very high debt) complicate things. The average U.S. credit score is 715, so aim for that or higher if possible.

Can a high income offset a low credit score?

Partially. High income improves your debt-to-income ratio, which lenders do consider. But it doesn’t fix a low score. Income isn’t part of the score calculation, so a score of 600 won’t become 650 just because you earn $100,000 annually. High income can help you get approved despite a lower score, but approval is harder than if your score were higher.

Can freelancers with thin credit files get approved?

Yes, but with caveats. If your thin file also contains clean payment history, approval is reasonable for mainstream cards. If your thin file contains any late payments or high utilization, approval becomes harder. A secured credit card is a realistic option if you’re declined, and after 12–18 months of responsible use, you can graduate to unsecured cards.

Does being self-employed automatically hurt my credit card approval chances?

No. Your employment status doesn’t affect your credit score or appear on your credit report. However, lenders may view self-employed applicants with more caution because income is typically less stable than salaried employment. This means you may need to provide more documentation (tax returns, invoices, bank statements) to verify income stability. Your score and payment history matter more than your employment status.

How fast can freelancers improve their credit scores?

Score changes depend on your starting point and what changes. If your only issue is high utilization, paying it down can improve your score in one to two billing cycles. If you have a recent late payment, you’ll see gradual improvement over months, with the most improvement coming after six months and one year pass. For significant rebuilding (multiple late payments, charge-offs), realistic improvement takes 12–24 months of consistent positive behavior.

Conclusion

Your credit score is the primary signal you send to credit card issuers. It says, “Here’s how I’ve behaved with credit in the past.” For freelancers, that signal is critical because your income itself is less stable than a salaried employee’s. Banks use your score as a proxy for financial reliability when your income is variable.

Realistically, a credit score above 680 makes mainstream credit card approval likely. A score below 620 makes it unlikely without a secured card or co-applicant. But your score isn’t the whole story. Issuers also verify your income, review your overall debt, assess your payment history pattern, and evaluate your credit file depth. A thin file, recent late payments, or high utilization can push approval into the “maybe” category even with a decent score. For freelancers, understanding how credit score affects credit card approval is essential because income alone rarely determines approval outcomes.

The good news: unlike salaried employees whose income is largely fixed, you have direct control over your credit behavior. Paying bills on time is always in your power. Managing your credit card balances is always in your power. Checking for errors on your credit report is always in your power. These actions don’t require higher income or a perfect business. They require discipline and consistency.

Set realistic expectations. If your credit score is currently below 650, don’t expect approval for premium cards. Aim for mainstream cards or a secured card first. Build positive payment history over 12–18 months. Then upgrade. If your score is 700+, you have a reasonable shot at mainstream approval, especially if you can verify income with tax returns or bank statements.

Credit scores are not a judgment on your worth as a person or entrepreneur. They’re a data-driven assessment of credit risk based on your past behavior. The positive take-away: your future behavior can always improve your score and your approval odds. At UncoverCards, we publish clear, research‑driven guides to help freelancers understand credit cards, approval criteria, and long‑term credit building strategies.

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, or credit advice. Credit card approval criteria vary by issuer, applicant profile, and market conditions. This information is based on general credit industry practices as of 2026 and should not be relied upon as specific guidance for your situation. Readers should review the specific terms, conditions, and eligibility requirements of any credit card issuer before applying. For personalized advice, consult with a financial advisor or credit counselor.