Introduction

How banks verify gig worker income for credit cards is a common question among freelancers, app-based workers, and independent contractors. The answer is more nuanced than a simple yes or no. Banks and credit card issuers approach gig worker income verification differently than they do with traditional employees. The process reflects both the realities of modern work and the financial industry’s evolving understanding of how people actually earn money today.

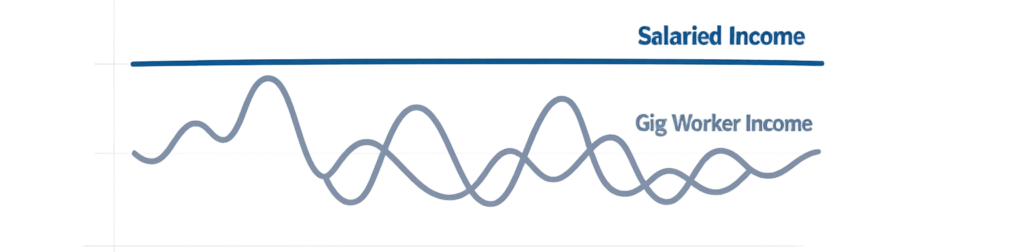

The core challenge is straightforward: unlike a salaried employee who receives a regular paycheck with a clear paper trail, gig workers experience income that fluctuates month to month. One month you might earn $3,000; the next, $1,200. This irregularity creates friction in a traditional lending system designed around predictable paychecks. Yet millions of gig workers get credit cards every year, which means banks have found ways to assess risk without requiring the neat salary slip documentation that salaried employees provide.

Understanding how this verification actually works matters for your financial life. It affects whether you’ll be approved for a card, what credit limit you might receive, and how to position yourself for the best possible outcome.

On This Page

- Introduction

- Do Banks Verify Gig Worker Income for Credit Cards?

- How Banks Verify Gig Worker Income for Credit Cards

- What Counts as Income for Gig Workers

- Gross Income vs. Usable Income for Gig Workers

- When Banks Actually Verify Gig Worker Income

- How Banks Verify Gig Worker Income If Asked

- How Inconsistent Gig Income Is Evaluated

- What Banks Do NOT Require from Gig Workers

- Common Income Verification Mistakes Gig Workers Make

- How Gig Workers Can Improve Approval Chances

- Frequently Asked Questions

- Conclusion

- Understand the Bigger Picture

- Disclaimer

Do Banks Verify Gig Worker Income for Credit Cards?

The short answer is: not always upfront, but they will if something looks suspicious.

Here’s what actually happens in most credit card applications. When you fill out an application, you’re asked to state your annual income. Most credit card issuers accept this figure at face value without immediately requesting documentation to verify it. This approach is called stated income—the lender takes what you tell them as true, at least initially.

This might seem surprising, but it reflects how credit card issuers operate differently from mortgage lenders or personal loan providers. Credit cards are unsecured debt, meaning the bank doesn’t have collateral to seize if you default. They manage risk through higher interest rates, credit limits, and strong credit history requirements. Your credit score becomes their primary verification tool—not your income documents.

Stated income means you declare your earnings on the application form, and the lender relies on that number to calculate your creditworthiness alongside your credit history, debt obligations, and credit score. The issuer trusts that you’re being reasonably honest because the consequences of lying are serious: if you default and it later emerges that you deliberately misrepresented your income, they can use that against you in collection efforts or legal proceedings. Understanding how banks verify gig worker income for credit cards helps applicants avoid overstating earnings and triggering unnecessary manual reviews.

Verified income refers to situations where the lender actually asks you to prove what you claim. They might request tax returns, bank statements, or earnings summaries from your gig platform. This typically happens with mortgages, personal loans, or when a credit card issuer becomes suspicious about your application. Many gig workers also wonder whether traditional pay stubs are required at all when applying for credit cards.

| Application Type | Documents Required | Approval Speed | Likelihood of Manual Review |

|---|---|---|---|

| Stated Income | Usually none upfront | Quick (often immediate) | Lower unless income seems extreme |

| Verified Income | Tax returns, pay stubs, bank statements, 1099 forms | Slower (several days) | High – intentional review part of process |

| Thin/New Credit File + Stated Income | May request limited documentation | Variable | Moderate to high |

| High Stated Income + Thin Credit | Documentation often requested | Slower | Very high |

The key distinction: banks do not routinely verify gig worker income when you first apply. They move quickly on most applications. Verification happens later—when you request a credit limit increase, if your spending patterns raise red flags, or if your stated income seems wildly inconsistent with your credit profile.

How Banks Verify Gig Worker Income for Credit Cards

To understand verification in practice, you need to understand how banks evaluate your ability to repay—and it’s broader than just looking at a single income number.

Ability to repay is a legal concept that credit card issuers must assess before approving you. They’re required to check whether you can actually afford to make monthly payments. This doesn’t mean you have to be rich; it means your income, debts, and obligations show a reasonable capacity to handle a credit card. Consumer credit rules require card issuers to assess an applicant’s ability to repay before approving a credit card.

Banks look at several factors simultaneously:

Your credit history and score is the strongest signal. If you’ve paid all your bills on time for years, even if you earn inconsistently, that history speaks louder than a single income number. A strong credit score demonstrates you prioritize payments even during lean months. In most cases, how banks verify gig worker income for credit cards depends more on credit history and existing debt than on traditional pay stubs.

Your existing debt load matters significantly. Banks calculate your debt-to-income ratio (DTI)—the percentage of your gross monthly income that goes toward debt payments. If your DTI is already 40% or higher, approval becomes harder, because you’re already committed to paying existing obligations. For instance, if you state $3,000 monthly income and already have $1,200 in monthly debt payments (from car loans, student loans, mortgage, other credit cards), your DTI is 40%. Adding a credit card payment to this becomes riskier.

Your bank account activity is another verification method that happens passively. Banks can see—if you grant permission during the application—whether income actually deposits into your account on a regular basis. Bank statement analysis looks at deposit patterns over months. If you said you earn $4,000 monthly but your bank statement shows $2,000 average deposits, that discrepancy flags a problem.

Your credit utilization on existing cards also matters. If you have a $5,000 credit card limit but only use $1,000, that signals responsible behavior. If you max out every card, issuers see risk, even if your income is high.

Your employment or business stability is evaluated based on what you’ve told them. Frequent job changes or constantly switching income sources raise concerns. Gig workers don’t face the same stigma they once did—banks now understand this is legitimate work—but newer workers with less than 6 months in a gig role might face scrutiny.

The big picture: banks assess your entire financial profile, not just income. This is why a gig worker with strong credit history, low existing debt, and consistent bank deposits often gets approved easily, even though their income fluctuates. Conversely, a salaried employee with a high salary but poor credit history, maxed-out credit cards, and a high DTI might be denied.

What Counts as Income for Gig Workers

Not all earnings are treated equally by banks, though in practice, credit card issuers are fairly flexible about income sources.

App-based gig income from platforms like rideshare, delivery, or task work absolutely counts. You report what the app shows you’ve earned. Banks accept this as legitimate income; the days of treating gig work as “not real work” are largely over.

Freelance and contract payments count as income. Whether you invoice clients directly or receive money from platforms like freelance marketplaces, these deposits into your bank account represent earned income that issuers will acknowledge.

Side income and multiple income sources can be added together. If you earn $2,000 monthly from delivery and $1,000 from freelancing, you can state $3,000 total monthly income. You don’t have to pick one source; the bank wants to know your total earning capacity.

Household income is trickier. If you live with a spouse or partner whose income regularly goes into a joint account you can access, or if someone regularly contributes to a shared account, you might be able to count a portion of that. However, you need to be clear about what you can actually access and be prepared to document it if asked. Banks want to see that the money actually flows to you or an account you control.

| Income Type | Stability Perception | Usability for Repayment |

|---|---|---|

| Primary gig work (6+ months history) | Moderate to good | High |

| Newly started gig work (<3 months) | Lower | Moderate |

| Multiple gig sources | Good if stable | High |

| Freelance with long-term clients | Good | High |

| Sporadic one-off freelance jobs | Lower | Moderate |

| Household income (shared, not primary) | Depends on documentation | Moderate |

| Seasonal work (gig-based) | Moderate if averaged annually | Moderate |

The principle is straightforward: if money regularly flows into your bank account, it counts. The more consistent and longer-established the pattern, the more weight it carries. A new gig job doesn’t disqualify you—but it might trigger a manual review to verify you’ve been at it long enough for the income to be real.

Gross Income vs. Usable Income for Gig Workers

This distinction might be the most misunderstood aspect of how gig worker income is evaluated for credit cards.

When you report income, you report gross income—the total before taxes and expenses. A gig worker earning $5,000 in gross income might only take home $3,500 after taxes, vehicle maintenance, phone bills, and app fees. But you still report the $5,000.

Banks understand this. They’re not naïve about gig work. They know you pay self-employment tax (around 15% for most gig workers), that you maintain vehicles or equipment, and that there are business expenses.

However, when they assess your ability to repay a credit card, they’re not doing complex tax math. They’re asking: “Can this person make the monthly payment?” They look at bank deposits to see what actually hits your account, regardless of whether it’s gross or net. If your bank statements show you’re typically depositing $2,500 monthly after all expenses, that’s the operative number for repayment capacity.

Usable income is what actually reaches your hands to spend on living expenses and debt payments. Here’s where the discrepancy matters. If you earn $5,000 gross but have $2,000 in monthly business expenses, taxes, and personal obligations, you’ve only got $3,000 truly available. That $3,000 needs to cover rent, food, insurance, loan payments, and your credit card payment. Your DTI calculation is based on this reality—lenders care about what you have left, not what you grossed.

This is why a credit card issuer might approve you for a higher limit based on your gross income, but then you get into trouble making payments because your actual monthly cash flow is tighter than the numbers suggested.

When Banks Actually Verify Gig Worker Income

Understanding the specific scenarios that trigger manual review and verification helps you prepare.

High stated income claims are a primary trigger. If you state annual income of $200,000 but your credit file is brand new, or if your spending history doesn’t match that income level, you’ll likely face a manual review. A lender wants to understand where such high earnings come from before extending significant credit.

Thin or new credit files combined with any income claim often result in verification requests. If you have no credit history, a few recent credit inquiries, or limited credit information, issuers want extra assurance. They might ask for documentation before approving you.

Credit limit increase requests almost always involve some verification, especially for gig workers. An issuer might initially approve you without documentation based on your credit score, but when you request a limit increase six months later, they’ll want current proof that your income is what you claimed.

Suspicious activity patterns trigger review. If you said your income is variable but claim $10,000 in income one month, nothing the next month, and then $500 the third month, that extreme volatility raises questions. Conversely, if you have perfectly flat deposits that don’t match a gig worker’s typical pattern, that can flag review too.

Multiple applications in a short period sends a risk signal. Applying for three credit cards in a month looks like you’re either desperate for credit or trying to maximize credit before something bad happens. Issuers see this as higher risk.

Inconsistencies between applications also matter. If you state $3,000 income on one card application and $6,000 on another submitted within weeks, that discrepancy will come out during verification and create problems.

New gig work status (less than 6 months) might trigger verification depending on the issuer. Some are flexible; others want to see you’ve sustained the income for a reasonable period.

How Banks Verify Gig Worker Income If Asked

When verification is required, here are the actual documents and methods used.

Bank statements are the most common request. A bank statement showing 6–12 months of deposits gives issuers a direct view of your cash flow. They look for patterns: regular deposits from your gig platform, consistency in amounts, and whether deposits align with your stated income. If you claim $3,000 monthly income but statements show $1,500 average deposits, that’s a problem.

Earnings summaries from gig platforms are valuable when you can access them. Many apps (rideshare, delivery, task work) let you generate earnings reports showing total earned, payments made, and payment dates. These reports directly verify the platform’s record of your income and carry weight because they’re from the source.

Tax filings matter most for self-employed gig workers. A recent tax return showing reported income gives official verification. However, keep in mind that many gig workers report income lower than what they actually earned due to claiming deductions. An issuer might see a tax return showing $30,000 reported income but your bank statements showing $45,000 in deposits—the deposits tell the fuller picture because they’re gross income before deductions.

1099 forms (if you receive them) document payments from clients or platforms. These prove income has been officially reported somewhere. However, not all gig workers receive 1099s—the IRS threshold is $20,000+ in annual transactions from a single source with 200+ transactions.

Profit and loss statements from your business (if you’re running a formal gig business) can demonstrate income and expenses, giving context for your net income available for repayment.

The pattern issuers look for: consistency and stability over time. They want to see that income deposits have been regular, that the amounts are sustainable, and that you’re earning what you claim. One big payment followed by nothing doesn’t count as reliable income. Steady $2,000 monthly deposits over a year proves more than sporadic $5,000 payments.

How Inconsistent Gig Income Is Evaluated

The fear many gig workers have is that irregular income automatically disqualifies them. It doesn’t. Here’s how issuers actually think about volatility.

First, they average income over time. If you earned $2,000 in January, $3,500 in February, $1,800 in March, and $2,700 in April, they’d calculate your average as about $2,500 monthly. That average becomes your stated income figure, not the highest or lowest month. This approach acknowledges that gig work has natural fluctuations while still measuring sustainable earning power. Inconsistent gig earnings can influence approval decisions differently depending on credit history and overall financial stability.

Second, they assess whether high-volatility income combines with a strong credit profile. A gig worker with inconsistent income but excellent payment history, low debt, and a credit score above 750 gets approved easily. The credit history proves you manage irregular income successfully. Conversely, a gig worker with volatile income, a recent late payment, and already-high debt faces rejection or higher scrutiny.

The logic is sound: if you’ve successfully managed irregular income for years, you’ve demonstrated the discipline to handle credit. A lender trusts that pattern.

Third, they consider whether you’ve worked in gig economy for sufficient time. Someone one month into a gig job faces more scrutiny than someone with two years of gig work. It takes time to prove you can sustain irregular income.

Some credit card issuers now specifically market to gig workers and have adjusted their underwriting models to handle volatility better. They’re more likely to approve irregular income if everything else looks solid. Traditional banks sometimes remain skeptical of self-employed and gig income, even when the income is real and consistent.

What Banks Do NOT Require from Gig Workers

Understanding these boundaries helps clarify how different gig work is treated.

Employer verification is not required. Unlike traditional employment where issuers might call your company’s HR department, gig workers don’t have employers to verify with. Banks understand this. They don’t expect or ask for employer verification because you don’t have one. The gig platform is your employer, and your bank statements prove you’re getting paid by them.

A fixed monthly paycheck is not required. This should be obvious, but many gig workers worry they’ll be penalized for not having a regular paycheck. You won’t. Banks have moved beyond the assumption that all income must be identical every month. They understand that consultants, freelancers, contractors, and gig workers have variable income, and they have processes for this.

Perfectly stable income is not required. Month-to-month variation is expected for gig workers. A 20% fluctuation in monthly income doesn’t disqualify you. What matters is that you’re earning something consistently enough that it’s predictable and sustainable.

Minimum tenure in a gig job is typically not a hard rule, though it is a consideration. Some issuers have internal policies that prefer 6+ months in a job before approving credit. However, many will approve newer gig workers if credit history is strong. There’s no universal minimum; it varies by issuer and situation.

Traditional employment history is not required. You don’t need to have ever worked a W-2 job or salaried position. Pure gig workers with no traditional employment history get credit cards regularly. What matters is your credit score and earning pattern, not what kind of work you do.

These non-requirements exist because the financial industry has caught up to the reality that work has changed. Gig economy participation in the US has grown substantially in recent years. Banks had to adapt or lose significant customer segments.

Common Income Verification Mistakes Gig Workers Make

Being aware of what doesn’t work helps you avoid creating problems.

Overstating income significantly is the most dangerous mistake. Claiming $10,000 when you earn $4,000 is fraud. If you’re approved based on that claim and then you default, the lender can use the deliberate misrepresentation against you. Even if you never default, if an issuer runs a financial review (which some card companies do periodically), discovering massive discrepancies can result in account closure, credit limit reduction, or your having to pay off your balance immediately.

Using your best month instead of average creates an inflated income figure that doesn’t reflect reality. If you made $6,000 in your best month but average $3,500, claiming $6,000 is misleading. Use averages.

Applying for multiple credit cards in a short period makes issuers cautious. Each application generates a hard inquiry on your credit report, which temporarily lowers your score. Multiple inquiries within weeks signal desperation for credit, which raises risk signals. Space applications out by at least a few months.

Mixing personal and business finances makes it harder to document income. If your gig earnings, personal savings, and everything else flows into one account with frequent transfers and commingling, bank statements become hard to interpret. Cleaner accounts with clearly identifiable income deposits are easier to verify.

Not accounting for tax liability. Some gig workers think about their gross income and fail to mentally account for the fact that they’ll owe self-employment tax. When they get a credit card and start spending based on gross income, they find themselves short when tax season arrives.

Providing outdated documentation. If asked for verification, submitting tax returns from three years ago or bank statements from six months ago when you’re applying now weakens your case. Current documentation matters.

Inconsistent information across applications. If you apply for two cards and state different income amounts, that inconsistency will surface during underwriting and create problems.

| Mistake | Impact | Better Approach |

|---|---|---|

| Overstating income (40%+ above actual) | Risk of fraud charge, account closure if discovered | Report honest average income |

| Using best month instead of average | Approval for higher limit you can’t afford; payment problems | Calculate 6–12 month average |

| Multiple applications in weeks | Lower credit score, manual reviews, possible denials | Space applications 3+ months apart |

| Undocumented cash income | Can’t be verified or counted; may trigger review | Deposit cash to bank account for verification |

| Vague income descriptions | Hard to verify; may trigger review | Specify “app-based rideshare income” not just “gig work” |

| Old documentation (2+ years) | Issuers want current picture | Provide current bank statements and recent tax returns |

How Gig Workers Can Improve Approval Chances

Beyond just honesty, strategic positioning helps.

Estimate income responsibly. Calculate your average monthly income over the past 6–12 months. If you’ve earned between $2,000 and $4,000 per month, with an average of $3,000, state $3,000. You can note that income varies, but averaging is fair. Most issuers allow you to explain variable income on the application.

Manage your debt-to-income ratio. Before applying, look at your monthly debt obligations. Add up car payments, student loan payments, mortgage or rent (some issuers count this), and minimum credit card payments. Divide by your average monthly income. If your DTI is above 40%, focus on paying down debt before applying. Even a $200 monthly debt reduction changes the equation materially.

Build and maintain strong credit history. This is the single most important factor. If you have a credit score above 700, consistent on-time payments, and low credit card utilization, you’ll be approved for most cards regardless of gig income unpredictability. Pay all bills on time, keep credit card balances below 30% of limits, and avoid hard inquiries unless necessary.

Use a primary bank account for income deposits. Don’t scatter gig income across five different accounts. Use one or two primary accounts so your deposit history is clear and concentrated. This makes bank statement verification straightforward.

Maintain consistent banking relationships. Issuers like to see that you’ve had the same bank account for at least 6–12 months with regular income deposits. Frequent account switching creates the appearance of instability.

Prepare documentation in advance. Before you apply, gather your last 6 months of bank statements, recent tax returns, and any earnings summaries from gig platforms. If you need to provide them, you’re ready immediately rather than scrambling to compile things later.

Apply with your primary bank first. Banks are more likely to approve existing customers than strangers. If you have a checking account at a bank, apply for their credit card first. The existing relationship increases approval odds.

Start with a credit card appropriate for your profile. Don’t apply for premium travel cards or high-end cash-back cards if you’re brand new to credit or have a thin file. Apply for cards designed for fair or good credit, get approved, use it responsibly, and upgrade later. This builds a track record.

Frequently Asked Questions

How do banks verify gig worker income for credit cards?

Most of the time, they don’t—not initially. They rely on your stated income, credit score, and credit history. Verification happens later if something looks suspicious, if you request a credit limit increase, or if automated systems flag your application for manual review. When verification is required, they’ll ask for bank statements (usually 6–12 months), tax returns, or earnings summaries from your gig platform.

Do gig workers need pay stubs?

No. Pay stubs are for employees. Gig workers typically don’t receive them. Instead, issuers accept alternative documentation: bank statements showing regular deposits from your gig work, earnings reports from the app or platform, tax returns, or 1099 forms if you receive them. The underlying principle is proof that money regularly reaches your account.

Can banks check my bank accounts?

Only if you give permission. When you apply for a credit card, you authorize the issuer to pull your credit report. Checking bank account balances typically requires explicit consent, often through a separate authorization. Some issuers have started requesting this as part of their evaluation, but it’s not universal. If asked, you can decline, though it might result in a manual review or denial.

What if my income can’t be verified?

The outcome depends on your credit profile and the specific issuer. If your credit score is excellent and you have strong payment history, many issuers will approve you based on credit factors alone, even without income verification. If your credit is average or below, inability to verify income often results in denial or a request for more documentation. You might be offered a lower credit limit as a compromise. Alternatively, you could apply for a secured credit card, which requires a cash deposit and has less stringent income requirements.

Can I include household income?

Sometimes, yes. If you have a spouse or partner whose income you genuinely have access to and use to support household expenses, you can sometimes include a portion of it. However, you need to be prepared to document it—likely with their tax returns and bank statements showing deposits. Be conservative: if you claim household income and can’t substantiate that you actually have access to it, you’re creating a verification problem. Most issuers are stricter about household income than your own income, so unless it’s significant and well-documented, stick to your own income.

How long does verification take?

Stated income applications without verification can be approved within minutes or hours. If manual review and income verification are required, expect several days to a week, sometimes longer. Documentation delays your application timeline.

What if I was recently laid off from my job and just started gig work?

This is a common scenario. Your first gig months might trigger more scrutiny because you’re new to gig work. However, if you had stable employment before and your credit score is good, many issuers will approve you based on prior income history while acknowledging your income transition. After a few months of gig work, reapply for better terms, and the newer income stream will be established.

Does being a new gig worker automatically disqualify me?

No, but it’s a risk factor, especially if combined with other concerns (limited credit history, high DTI, thin credit file). New gig workers with strong credit history and low existing debt still get approved regularly. New gig workers with poor credit or high existing debt face steeper obstacles.

Can I mention irregular income as a reason for lower approval?

Yes, and many gig workers do. On applications, you often have a field to explain circumstances. Being upfront about seasonal fluctuations or noting that you’re new to gig work can actually help because it shows transparency. However, if you’re going to mention irregularity, your credit profile and documented income pattern need to demonstrate you manage it successfully.

Conclusion

How banks verify gig worker income for credit cards is ultimately less dramatic than many gig workers fear. The system has evolved to recognize that irregular income doesn’t equal unreliable income, and that a gig worker with strong credit history and disciplined financial management can be approved just as readily as a salaried employee.

The core mechanism is pragmatic: issuers care about ability to repay, demonstrated through credit history and current financial obligations, more than they care about employment classification. They’ve learned that a gig worker earning $3,000 monthly consistently over two years, with a 750 credit score and $200 in existing debt, represents less risk than a salaried employee earning $5,000 monthly with a 650 credit score and $3,000 in existing debt.

Most applications aren’t verified upfront. Banks use stated income for speed. When verification happens, it’s because something prompted manual review—high income claims, thin credit files, suspicious patterns, or limit increase requests. The documents they request are straightforward: bank statements showing your deposits, tax returns, or earnings reports from your gig platform. These directly demonstrate that you earn what you claim.

The biggest verification risks come from overstating income, making inconsistent claims across applications, or applying when you don’t have a clear income pattern. Gig workers who are honest about their average income, maintain strong credit history, manage their existing debt, and apply strategically get approved without complications.

Your path to credit card approval as a gig worker isn’t fundamentally different from any other applicant’s. Your credit behavior matters more than your employment type. Build strong credit, manage debt, and apply strategically—the rest follows. Knowing how banks verify gig worker income for credit cards allows gig workers to apply confidently, report income honestly, and improve approval chances without unnecessary stress.

Understand the Bigger Picture

While income verification is a key part of approval, it’s only one piece of the process. To see how credit cards work overall for gig workers and freelancers in the US, explore our complete guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This article is for educational purposes only and should not be considered financial, legal, or tax advice. Credit card application policies, approval processes, and income verification requirements vary by issuer and change over time. Income thresholds, credit score requirements, and documentation needs differ between banks. Individual circumstances affect approval decisions in ways that generalized guidance cannot predict. Consult with your bank directly about their specific requirements, and consider speaking with a financial advisor about your personal situation before applying for credit.