Introduction

First credit card options for new gig workers in the US can feel more complicated because income and documentation look different from traditional jobs. The challenge isn’t that gig workers can’t qualify for credit—it’s that lenders have to evaluate you differently, and many don’t have experience with your type of income.

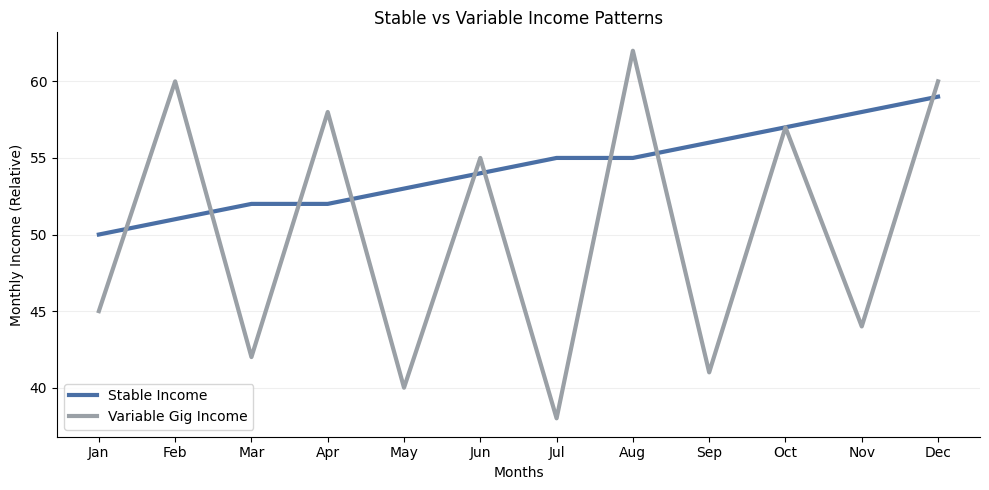

When you earn from apps and freelance platforms, your income looks different on paper. There’s no salary stub. Your monthly earnings fluctuate. You might make $2,500 in June and $1,800 in July. Traditional credit card algorithms were built for stable paychecks, so when a computer system sees variable income and no credit history, it often says “no” automatically. Choosing the right first credit card options for new gig workers early makes the credit‑building process smoother and avoids unnecessary rejections.

The good news: getting approved for a first credit card as a gig worker is absolutely possible. It just requires understanding how lenders evaluate your application, knowing which cards are designed for people like you, and choosing the right card for your situation. Your first card is a tool to start building credit—something that will matter for almost every major financial decision you’ll make in the years ahead.

On This Page

- Introduction

- Why New Gig Workers Struggle With Credit Card Approval

- What Card Issuers Look for in New Gig Workers

- First Credit Card Options for New Gig Workers Explained

- Credit Card Options Gig Workers Should Avoid

- How to Choose the Right First Card

- Credit Card Comparison for Gig Workers

- How Long It Takes to Build Credit as a Gig Worker

- Common Mistakes New Gig Workers Make

- Frequently Asked Questions

- Can gig workers get a credit card with no credit history?

- Are secured cards worth it?

- What income should I report on my application?

- How long should I wait before applying again after rejection?

- Should I apply for multiple cards in different categories to improve my odds?

- What if I’m denied? What’s my next move?

- Can I use my gig platform earnings records instead of bank statements?

- Is having no credit score better or worse than having bad credit?

- Conclusion

- Start with the Complete Credit Card Guide

- Disclaimer

Why New Gig Workers Struggle With Credit Card Approval

Credit card companies face a real challenge when evaluating gig workers. The approval process relies on data that doesn’t always exist for you.

Variable Income

Lenders want to see consistent income because it helps them predict whether you’ll be able to make monthly payments. When your earnings swing from $3,000 one month to $1,200 the next, the algorithm can’t calculate a reliable “average.” The computer might see the low months and reject you, assuming you can’t handle a payment obligation. Even if you know you’ll always earn enough, the system doesn’t.

Thin or Nonexistent Credit Files

Many new gig workers have never used credit before. If you’ve paid cash for everything and never had a credit card or loan, the credit bureaus have zero information about you. Credit card companies rely on this data to assess risk. With a blank file, they have nothing to reference—no payment history, no evidence of responsibility. If you are starting from scratch, understanding credit card options for people with low or no credit history can help you choose a safer first step.

Manual Review Delays

When your application doesn’t fit the standard profile, it moves from automated approval to manual review. This means a human looks at your file, which takes longer. Some lenders don’t specialize in gig income, so even manual review can end in rejection. The delay alone frustrates many applicants who expect instant decisions. Gig workers who want to understand approval timelines in more detail can also explore how long credit card approval typically takes in the US.

Income Documentation Challenges

Traditional employees provide a recent pay stub. You can’t. Instead, you might have bank statements, 1099 tax forms, or platform earnings records. Not all lenders accept these documents, and those who do often need to verify them manually. This adds complexity to the approval process.

What Card Issuers Look for in New Gig Workers

Understand what lenders actually evaluate when they review your application. If you know what they want to see, you can present yourself in the strongest possible way.

| Approval Factor | What Lenders Look For | What Gig Workers Can Show Instead |

|---|---|---|

| Income verification | Recent pay stubs from stable employer | 3–6 months of bank statements showing deposits from gig platforms; 1099 tax forms; platform earnings records; tax returns showing Schedule C income |

| Bank account activity | Regular deposits from employer | Consistent deposits from multiple gig platforms; evidence of savings; active checking account with positive balance |

| Credit file | At least one credit account in good standing | Authorized user status on someone else’s card; utility payments; rent payments; other bill payments (through services that report to bureaus) |

| Debt-to-income ratio | Low monthly obligations relative to salary | Low existing debt; no other active credit cards; clean loan payment history |

| Employment history | Multiple years at current job | Evidence of gig work for 6+ months; multiple gig platforms used; positive platform ratings or reviews |

| Address stability | Same address for 2+ years | Any valid current address; rent or lease documents |

Key insight: Lenders want to know three things: Can you earn money consistently? Are you responsible with obligations? Have you successfully managed credit before? You can answer these questions even without a traditional job. Credit scores also play an important role in approval decisions, especially for applicants with limited credit history.

First Credit Card Options for New Gig Workers Explained

Your first card should accomplish two goals: get you approved, and help you build credit over time. Here are the realistic options.

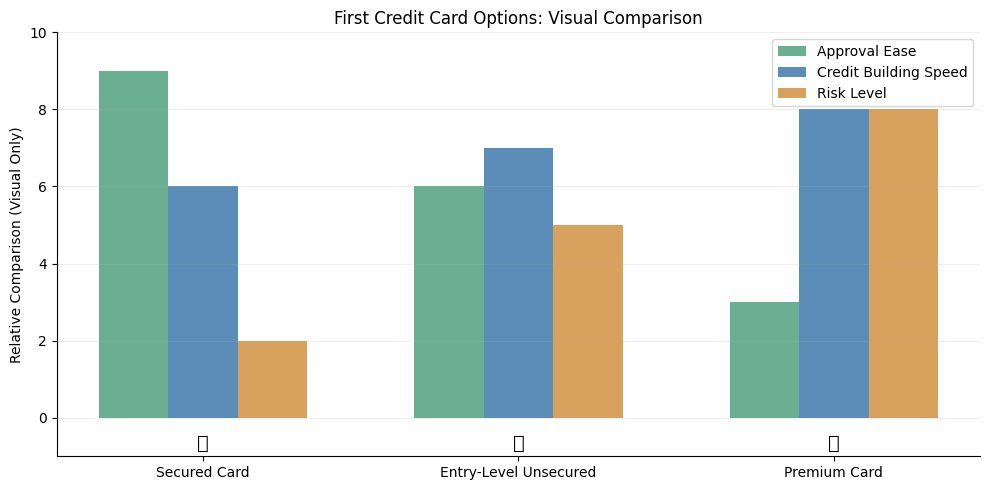

Secured Credit Cards

A secured card requires you to deposit cash upfront—typically $200 to $2,500. That deposit becomes your credit limit. If you put down $500, you get a $500 credit limit.

Why this works for gig workers: You don’t need a credit score to apply. Income requirements are minimal or nonexistent. Approval is nearly guaranteed. The card issuer takes almost no risk because they already have your money.

How it helps you: After 6–12 months of responsible use—making on-time payments and keeping your balance low—you can ask the issuer to convert the card to a regular unsecured card. Your deposit gets returned, and you’ve built a documented payment history.

Realistic fees: Expect a $25–$95 annual fee on most secured cards. Monthly interest rates (APR) are typically 18–25%, which is higher than regular cards, but this doesn’t matter if you pay your balance in full each month.

Best for: Gig workers with zero credit history or those who have been denied for unsecured cards.

Entry-Level Unsecured Cards

Some card issuers specifically design products for people building credit. These don’t require a deposit, but they do have higher interest rates and lower credit limits than premium cards.

Income requirements: Usually between $15,000–$25,000 annually (some cards ask for no proof at all, just your stated income).

Approval odds: Better if you can show 6 months of gig income through bank statements. Lenders care less about job stability and more about recent income evidence

Credit limits: Usually $300–$1,000 for first-time applicants.

Best for: Gig workers with 6+ months of documented income and no credit history, or those with a thin credit file (1–2 previous accounts).

Cards That Accept Gig Income

A small number of card issuers have built systems specifically to evaluate self-employed and gig workers. They use alternative income verification—bank statements, platform records, and tax returns instead of W-2s.

What’s different: These issuers understand that your income looks different and don’t penalize you for it. Their systems are designed to evaluate platform-based income.

Income documentation: You’ll typically need 3–6 months of bank statements showing gig deposits, or your most recent tax return (Form 1040 with Schedule C).

Best for: Gig workers with 12+ months of gig work history and moderate income consistency.

If you can’t qualify for your own card, ask a family member or trusted friend with good credit to add you as an authorized user on their existing card. Their positive payment history gets reported on your credit report.

Why this matters: You build credit without approval risk. After 6 months as an authorized user on a well-managed account, your credit file becomes thicker and stronger, making you a more attractive applicant for your own card.

What to expect: No impact on your credit score immediately, but within 6 months, your file should improve enough to qualify for a beginner’s card.

Important: Make sure the primary cardholder pays on time and keeps balances low. If they miss payments or max out the card, it hurts your credit too.

Best for: New gig workers waiting to build an initial credit foundation, or those recently denied for a card.

Credit Card Options Gig Workers Should Avoid

Not all cards are good starting points. Some will waste your money, and others might actually hurt your credit journey.

Cards that promise travel rewards, cash back, or luxury benefits require a credit score of 750+. If you’re building credit from zero, you won’t qualify. Applying anyway just generates a hard inquiry that temporarily lowers your score.

Cards with Excessive Fees

Some cards charge $200+ annual fees for beginners. With a secured card requiring a deposit, you’d be paying a deposit plus a high fee for the privilege. The math doesn’t work. Stick with cards that charge under $50 annually or have no annual fee.

High-Risk “Guaranteed Approval” Cards

Cards advertised as “no credit check” or “guaranteed approval” are usually predatory. They come with extreme fees, deceptive terms, or interest rates above 35%. Building credit isn’t worth these terms.

Multiple Cards at Once

New gig workers often want to apply for several cards simultaneously to improve their odds. This backfires. Each application generates a hard inquiry, which temporarily damages your credit. Multiple inquiries in a short time signal to lenders that you’re desperate for credit, making rejection more likely.

Cards Requiring Income Above Your Reach

If a card requires $50,000+ annual income and you earn $18,000, don’t apply. The issuer will deny you, and you’ll get a rejected application on your record. Each rejection makes the next application harder.

How to Choose the Right First Card

Given the options, how do you pick the right first card for your situation?

Step 1: Assess Your Current Credit Position

Start by knowing where you stand. Check if you have a credit score at all. If you’ve never used credit, you probably don’t—and that’s fine. Go to your credit bureau’s website and request a free credit report. Look for errors and get a baseline understanding of your file.

Step 2: Verify Your Income Documentation

Before applying, gather what you’ll need to prove income: 3–6 months of bank statements (highlight gig deposits); your most recent tax return if filed (Form 1040 with Schedule C); copies of 1099s from gig platforms (if you received them); and paystubs or earnings records from apps you use.

Having these ready speeds up the approval process and prevents delays from missing documents.

Step 3: Consider Your Approval Odds

If you have no credit history and zero access to someone who can add you as an authorized user, start with a secured card. Your approval odds are nearly 100%.

If you have 6+ months of documented gig income and no credit history, try an entry-level unsecured card first. If rejected, a secured card is your backup.

If you have some credit history (even if thin) and moderate gig income, entry-level unsecured cards are realistic.

If you’ve been denied once, wait at least 30 days before applying again. Each rejection stays on your credit report for 12 months, but its impact fades.

Step 4: Check Your Approval Odds Without Risk

Many card issuers offer a “pre-qualification” or “pre-approval” tool on their websites. You enter basic information, and the system tells you whether you’re likely to be approved. This is a soft inquiry and doesn’t affect your credit score. Use this before submitting a full application. For a clear understanding of how credit cards work and how consumer credit is regulated, gig workers can also review basic credit education provided by consumer protection authorities.

Step 5: Choose Based on Your Goals

- Fastest approval: Secured card

- Best credit-building terms: Entry-level unsecured card with low fees

- Lowest deposit requirement: Secured card with flexible deposit amounts ($49–$200 options)

- Potential rewards: Entry-level unsecured cards that offer 1% cash back

Credit Card Comparison for Gig Workers

| Card Type | Approval Odds | Security Deposit | Annual Fee | APR | Best Use |

|---|---|---|---|---|---|

| Secured Card | ~95% | $200–$2,500 | $25–$95 | 18–24% | No credit history, guaranteed approval needed |

| Entry-Level Unsecured | ~70% | None | $0–$50 | 20–27% | 6+ months gig income, building credit |

| Gig-Worker Specialized | ~65–80% | None | $0–$95 | 18–26% | 12+ months gig work, platform income verified |

| Authorized User | ~100% | None | Varies | Varies | Access someone with established credit |

How Long It Takes to Build Credit as a Gig Worker

Building credit doesn’t happen overnight, but it’s faster than many people think. Understanding how credit scores are built over time can help gig workers set realistic expectations during the early months.

| Timeline | Credit Progress | What Happens |

|---|---|---|

| Months 1–3 | No score yet | Your account is open and reporting to bureaus, but no FICO score exists. You’re in the quiet period. |

| Month 6 | First score generated | You usually get your first credit score between 500–700. On-time payments result in higher scores |

| Months 6–12 | Score improves 20–50 points | Each on-time payment strengthens your file. Keeping utilization below 30% helps. You’re now creditworthy for many purposes |

| Months 12–24 | Score improves another 50–100+ points | Your account age increases, building length of credit history (15% of your score). You can apply for a second card. |

| Year 2+ | Good credit possible | With consistent on-time payments and multiple accounts, scores above 700 are realistic. You qualify for better rates on everything. |

Variables that speed things up:

- Adding utility or rent payments to your credit report (via services that report to bureaus)

- Becoming an authorized user on a well-managed account

- Multiple cards with on-time payments

- Low credit utilization (under 10% is ideal)

Variables that slow things down:

- Any missed payments (even one day late)

- High utilization (using 50%+ of your limit)

- Too many credit applications in a short time

- Not using your card at all (bureaus need to see activity)

Common Mistakes New Gig Workers Make

Even when you understand the process, it’s easy to stumble.

Applying for Multiple Cards Immediately

Each application creates a hard inquiry, which temporarily lowers your score by 5–10 points. Three applications in one month can lower your score by 15–30 points. Lenders see multiple inquiries as desperation, which increases rejection odds. Instead, apply for one card, wait 6 months, then add another.

Overstating Your Income

It’s tempting to round up your earnings or claim income you don’t consistently receive. Don’t. Lenders verify this information, especially for gig workers. Providing false income is application fraud and can result in legal consequences. Stick to honest numbers you can document.

Choosing the Wrong Card Type

Applying for premium cards when you have no credit wastes time and generates rejections. You can’t build credit with cards designed for people already holding credit. Start with cards explicitly designed for beginners.

Ignoring Your Credit Report

Errors on your credit report are surprisingly common. A mistaken late payment or someone else’s account listed under your name can tank your approval odds. Request your free annual credit report and review it before applying. If you find errors, dispute them.

Not Reading the Fine Print

Secured cards vary wildly in terms. Some allow you to convert to unsecured after 7 months; others require 18 months. Some have no annual fee; others charge $95. Some cap your deposits at $500; others allow $5,000+. Read the full terms before applying.

Maxing Out Your Card

Your credit utilization ratio (how much of your limit you’re using) is 30% of your credit score. If you have a $500 limit and carry a $400 balance, you’re using 80%—which hurts your score. Keep it below 30%. Even better, keep it in single digits (under 5%).

Missing a Payment

One missed payment stays on your credit report for 7 years. If you have a new credit card, missing even one payment significantly damages your building credit. Set up automatic payments if you’re worried about forgetting.

Frequently Asked Questions

Can gig workers get a credit card with no credit history?

Yes. Secured cards don’t require credit history—just a cash deposit. Entry-level unsecured cards also approve people with no history if they have documented income. Being added as an authorized user is another zero-history option. General guidance on credit cards and first‑time applicants is also available through official public information resources.

Are secured cards worth it?

Absolutely, but only if the issuer reports to credit bureaus (which nearly all do). The card builds your credit history quickly, and after 6–12 months, you can graduate to an unsecured card and get your deposit back. The annual fee is the only real cost, usually $25–$95.

What income should I report on my application?

Report your actual average monthly or annual income. You can calculate this from bank statements or tax returns. If your income fluctuates, use an average from the past 6–12 months. Be honest—lenders verify this, especially for gig workers

How long should I wait before applying again after rejection?

Wait at least 30 days, ideally 60–90 days. This gives time for the rejection to age on your report and for you to improve your application (build income history, lower utilization on other cards, etc.). Applying immediately after rejection rarely helps.

Should I apply for multiple cards in different categories to improve my odds?

No. Multiple hard inquiries hurt your score and signal desperation to lenders. Instead, focus on one card that fits your profile. Wait 6 months after approval before applying for a second card.

What if I’m denied? What’s my next move?

Request the denial reason from the card issuer (they’re required to provide this). Common reasons: low income, no credit history, or high debt-to-income ratio. Address the specific issue (e.g., get a secured card if it’s “no credit history,” wait 6 months if it’s “too recent income”). Then reapply.

Can I use my gig platform earnings records instead of bank statements?

Some issuers accept platform earnings records, but bank statements are stronger because they prove money actually reached your account. Provide both if possible.

Is having no credit score better or worse than having bad credit?

Better. Lenders would rather take a chance on someone with no history (you could be responsible) than someone with a proven track record of missed payments. Starting from zero puts you ahead of rebuilding from damage.

Conclusion

Getting your first credit card as a gig worker is possible and absolutely worthwhile. The key is understanding that you’ll be evaluated differently than someone with a W-2 job, and that’s not a barrier—it’s just a different process. Understanding first credit card options for new gig workers helps you start building credit without rushing into the wrong product.

Start with the right card type for your situation. If you have no credit history, a secured card is your fastest path. If you have 6+ months of documented income, entry-level unsecured cards are within reach. Either way, you’re building the foundation for better financial opportunities.

Your first card is not about rewards or fancy features. It’s about proof. Over the next 12–24 months, every on-time payment proves to lenders that you’re responsible. That proof opens doors: better credit card terms, lower interest rates on future loans, approval for car financing, and even advantages on rental applications.

Consistency beats speed. The gig workers who build strong credit fastest are those who use their first card responsibly for months and years—not those who apply for multiple cards immediately or max out their limits. Keep your balance low, pay on time every time, and you’ll be amazed at how quickly your credit story improves. These first credit card options for new gig workers are designed to help you build credit slowly and safely without unnecessary rejections. For more beginner‑friendly guides on credit cards and approval strategies, explore our complete credit education resources.

Start with the Complete Credit Card Guide

If you’re new to credit cards as a gig worker or freelancer and want a full breakdown of how approval works, income is evaluated, and what improves your chances, read our complete guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This article is educational and informational only. It does not constitute financial advice, legal advice, or a recommendation to apply for any specific credit card. Credit card approval criteria vary by issuer and individual profile. Terms, fees, and rates change frequently. Before applying for any credit card, review the issuer’s full terms and conditions, and consult a financial advisor if needed.