Introduction

Many beginners hear terms like “secured card” and “unsecured card” and assume they’re just different labels for the same thing. Both are plastic (or metal) cards. Both swipe or tap in the same way. Both let you buy something now and pay later. So it is completely understandable to confuse them.

Under the surface, though, secured and unsecured credit cards work very differently. One asks you to put down money up front as a security deposit. The other does not. One is designed to give people with little or damaged credit a starting point. The other assumes you already have some track record with credit. Understanding that difference between secured and unsecured credit cards is crucial if you are a beginner. This guide explains the difference between secured and unsecured credit cards in simple terms so beginners can choose the right option without confusion.

Choosing the wrong type of card can slow down your progress. If you keep applying for unsecured cards and getting rejected, you waste time and create unnecessary “hard inquiries” on your credit reports. If you open a secured card with high fees and then close it too quickly, you might lose a useful tool for building a strong history. This guide walks through secured credit card vs unsecured credit card step by step so you can choose confidently and build credit in a steady, low‑stress way. If you’re new to credit, our credit card guides for beginners explain everything step by step.

On This Page

- Introduction

- What Is a Secured Credit Card?

- What Is an Unsecured Credit Card?

- Key Differences Between Secured and Unsecured Credit Cards

- Approval Requirements Compared

- Credit Limits, Fees, and Interest Rates

- Which Card Builds Credit Faster (And Why)

- Who Should Choose a Secured Credit Card

- Who Should Choose an Unsecured Credit Card

- Common Beginner Mistakes to Avoid

- Difference Between Secured and Unsecured Credit Cards: Final Verdict

- Frequently Asked Questions

- Conclusion

- Explore the Complete Credit Card Guide

- Disclaimer

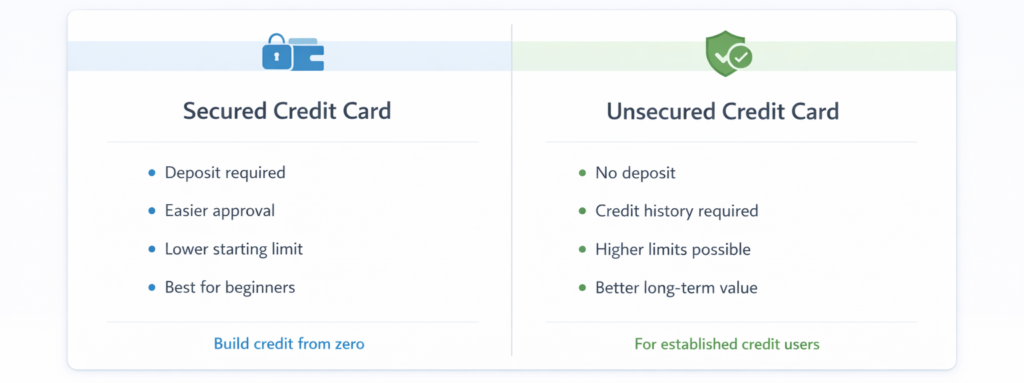

What Is a Secured Credit Card?

A secured credit card is a credit card that requires a refundable security deposit before you can use it. The deposit is usually paid by bank transfer or debit card when you open the account. The card issuer holds this money as collateral. If you do not pay your bill, the issuer can use the deposit to cover what you owe. A secured card requires a refundable deposit, which helps beginners understand what is a secured credit card and why approval is easier.

In most cases, your secured credit card deposit equals your credit limit. If you put down 300 dollars, your starting limit is usually about 300 dollars. Some issuers may give you a limit slightly higher than your deposit after you have shown good payment behavior for a while. But as a beginner, it is safest to assume: deposit in = starting limit out.

Typical minimum deposits often start around 200–300 dollars, and you may be allowed to deposit more if you can afford it. A higher deposit gives you a higher credit limit, which can make it easier to keep your “credit utilization” (the percentage of your limit you are using) comfortably low. For example, if your limit is 300 dollars and you carry a 150‑dollar balance, you are using 50% of your limit, which is quite high. If your limit is 1,000 dollars and you carry that same 150‑dollar balance, you are only using 15%.

Because the deposit reduces the risk for the lender, secured credit card approval odds are generally higher than with unsecured cards for people who have thin or damaged credit files. Issuers are often willing to approve:

- People with no credit history at all (true beginners)

- People with limited history (just a few accounts)

- People rebuilding after late payments, collections, or other issues

- Students, gig workers, or part‑time workers with modest incomes

This is why a secured credit card for beginners is often recommended when you are starting from zero. As long as you have some income and can afford the deposit and the ongoing payments, a secured card is usually easier to get than a traditional unsecured card.

From your day‑to‑day point of view, a secured card works just like any other credit card. You use it for purchases, you get a monthly statement, and you must make at least the minimum payment by the due date. The deposit does not act as a pre‑paid balance; you still owe the bill every month.

What Is an Unsecured Credit Card?

An unsecured credit card is the “regular” kind of credit card most people think of. It does not require any deposit or other collateral. The issuer gives you a line of credit based on your application, income, and credit history, and you promise to pay back what you borrow. Before applying, beginners should clearly understand what is an unsecured credit card and how approval depends on credit history.

Instead of looking for a secured credit card deposit, the issuer looks at:

- Your credit reports and credit scores

- Your income and employment or self‑employment situation

- Your existing debts, such as student loans, auto loans, or other cards

- How reliably you have paid other accounts in the past

Because there is no deposit protecting the lender, unsecured credit card approval is more selective. Many of the best unsecured cards—especially those with rewards or low promotional interest rates—expect you to have at least some established, positive credit history.

This is exactly where beginners run into problems. You might:

- Have never had a credit card or loan before

- Be working part‑time, freelancing, or gig driving with inconsistent income

- Be a student with limited work history

- Have recent late payments or other negative marks

From the lender’s perspective, this makes you a higher risk. As a result, beginners often get rejected for unsecured credit cards, or are only offered cards with lower limits and higher interest rates and fees. That is why understanding unsecured credit card requirements is so important before you start applying.

Key Differences Between Secured and Unsecured Credit Cards

At a glance, the difference between secured and unsecured credit cards comes down to collateral (deposit) and who they are designed for. But there are several other practical differences that matter for beginners.

Here is a simple side‑by‑side view:

Secured vs Unsecured Credit Card – Key Features

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Deposit required | Yes, refundable security deposit | No deposit required |

| Typical minimum deposit | Around 200–300 dollars | Not applicable |

| How limit is set | Usually equals deposit (may grow over time) | Based on credit history, income, and overall profile |

| Who it’s designed for | No/low credit, rebuilding credit | People with established credit history |

| Approval difficulty | Generally easier for thin or poor credit | Harder with no history; easier with good history |

| Typical fees | May be higher; sometimes more fees | Varies; more low‑fee options available |

| Typical APR | Often higher than similar unsecured cards | Varies; many cards still high, but best offers can be lower |

| Ability to build credit | Yes, if issuer reports to major credit bureaus | Yes, if issuer reports to major credit bureaus |

| Path to upgrade | May “graduate” to unsecured after good behavior | Already unsecured; you may qualify for better cards over time |

Both types can help with credit building if managed responsibly. The main difference is that secured cards are easier to get when you are new to credit, while unsecured cards are usually cheaper to hold over the long run once your credit is stronger.

Approval Requirements Compared

Income

For both secured and unsecured cards, issuers want to see that you have enough income to pay your bills. With a secured card, the deposit reduces risk, so issuers may be more open to lower or less predictable income sources, such as part‑time work or gig income. For unsecured cards, income requirements can be stricter because there is no deposit backing the account.

In simple terms:

- Secured card: Income needs to be sufficient to afford the deposit and minimum payments, but standards may be more flexible.

- Unsecured card: Income often needs to be higher and more stable for approval, especially for cards with better rates or rewards.

Credit History

Secured cards are built for people with little or no history, or for those trying to repair past mistakes. Many secured cards specifically advertise that they accept people with “limited” or “less‑than‑perfect” credit.

Unsecured cards, by contrast, are usually based heavily on your existing credit track record: have you made payments on time, kept balances low, and avoided serious delinquencies? The better your history, the higher your odds of approval and the better the terms you receive.

Risk Perception by Lenders

From a lender’s point of view:

- Secured credit card: Lower risk because the deposit can be used to cover losses if you stop paying. This is why secured credit card approval odds are often higher for beginners.

- Unsecured credit card: Higher risk because there is no collateral. The lender relies solely on your promise to pay, backed by your past behavior and current finances.

This is the heart of secured credit card vs unsecured credit card approval differences. If your profile looks risky—no history, irregular income, or prior credit issues—a secured card is usually the more realistic and less stressful starting point.

Credit Limits, Fees, and Interest Rates

Typical Credit Limits

Secured credit limits usually start low, often equal to your deposit amount—commonly in the 200 to 500‑dollar range for beginners. You can sometimes raise your limit by adding to your deposit or by showing a pattern of reliable payments.

Unsecured card limits vary widely. If you are just starting out, you might be approved for a relatively low limit. With stronger credit and higher income, limits can be much higher, and they may increase over time based on your payment history and how you use the card.

Annual Fees and Other Charges

Secured cards sometimes come with higher or more frequent fees: annual fees, monthly maintenance fees, activation fees, or even setup charges in some cases. Not all secured cards are expensive, but the lower your credit standing, the more likely you are to see extra fees.

Unsecured cards range from no‑annual‑fee options to premium cards with higher annual fees in exchange for richer rewards or perks. For beginners with modest credit, there are usually at least some low‑fee or no‑fee unsecured options, but they may still come with higher interest rates.

Interest Rates (APR)

Both secured and unsecured cards can have high interest rates, and many are above 20% annual percentage rate (APR) in today’s market. However, secured cards often sit at the higher end of the range, especially for people with poor or very limited credit. Unsecured cards for people with good credit may offer lower ongoing APRs or even short‑term introductory 0% APR offers on purchases or balance transfers.

Here is a high‑level cost overview:

Cost Comparison Overview

| Cost Element | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Security deposit | Yes, usually 200–500 dollars or more; refunded if account closes in good standing | None |

| Typical starting limit | Roughly equal to deposit; may increase with good behavior | Based on credit and income; can be higher, with potential increases |

| Annual fee | Sometimes higher, especially for weaker credit profiles | Wide range: no‑fee to premium fees |

| Other fees | Possible setup, maintenance, or additional fees | Varies; may include late, balance transfer, and cash advance fees |

| Typical APR pattern | Often high; can be higher than similar unsecured cards | Also often high; best offers can be lower or include promos |

Remember, if you pay your statement balance in full and on time each month, you can generally avoid paying interest on purchases, regardless of whether your card is secured or unsecured. The key is disciplined use.

Which Card Builds Credit Faster (And Why)

Both secured and unsecured credit cards can help build credit if the issuer reports your account to the major credit bureaus and you use the card responsibly. From a credit‑building perspective, what matters most is not the label on the card, but your behavior.

Key factors include:

- On‑time payments: Paying at least the minimum by the due date every single month.

- Credit utilization: Keeping the balance low relative to your limit—ideally using only a small portion of your available credit.

- Account age: Keeping accounts open and in good standing over time.

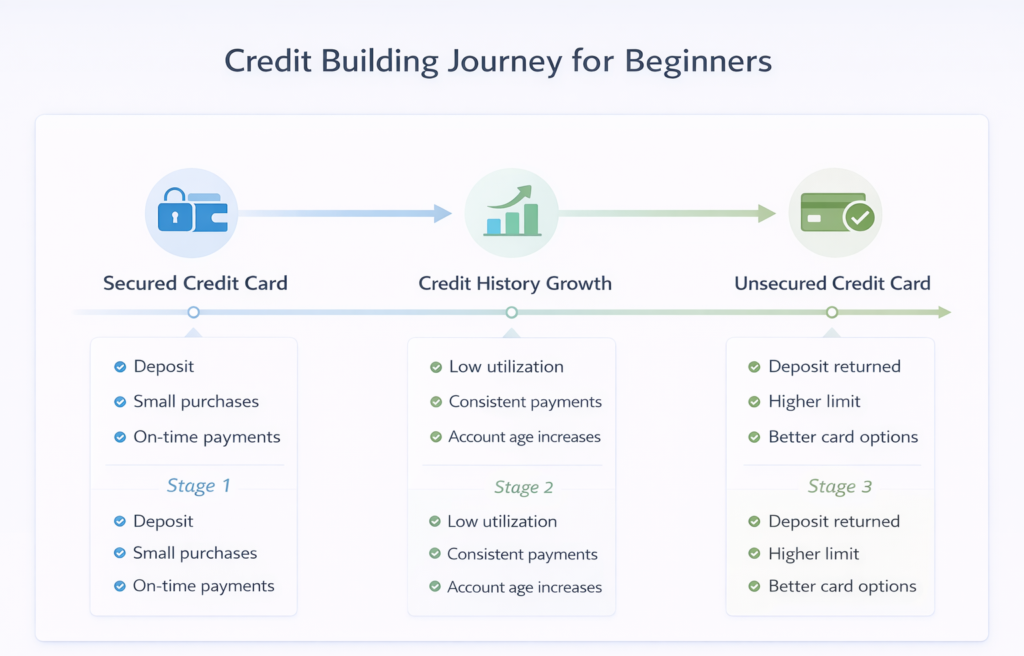

Where a secured card can have an advantage is simply that it is easier for a beginner to obtain early on. Instead of applying for multiple unsecured cards and getting denied, you can secure approval once and start your credit building with secured cards right away. Long‑term progress depends on payment behavior and understanding how credit cards build credit, not just the card type. That means positive payment history starts appearing more quickly on your credit reports.

That said, if you already qualify for a reasonably priced unsecured card with a decent limit and low fees, it can build credit just as well. The card type does not change how your history is recorded; the bureaus generally do not care whether your card is secured or unsecured, only whether you pay on time and manage it well.

Many issuers allow a “graduation” path: after around 6 to 18 months of on‑time payments and responsible use, they may review your account, return your deposit, and convert you to an unsecured card. This makes the secured card a kind of temporary training tool that leads to a standard unsecured card over time.

Who Should Choose a Secured Credit Card

A secured card is often the right first step if:

- You have no credit history at all. Maybe you have never had a loan, never co‑signed for anyone, and never had a credit card. In that case, a secured credit card for beginners can serve as your very first entry in your credit file.

- You have been rejected for unsecured cards. If you have already tried for an unsecured card and received denials, switching to a secured option can stop the cycle of rejections and give you a realistic path forward.

- You are rebuilding after problems. Past late payments, charge‑offs, or other negative events can make unsecured credit card approval hard. A secured card gives you a structured way to demonstrate that things have changed.

- Your income is irregular. If your work is seasonal, freelance, or gig‑based, lenders may be more comfortable starting you on a secured product, because the deposit reduces their risk during months when your income may drop. Secured cards are often a safer option for people with irregular income, including those exploring credit cards for gig workers and freelancers.

The key is to choose a secured card with reasonable fees and clear terms, use it lightly, pay it in full and on time, and treat it as a short‑to‑medium‑term tool. Over time, you can move up to a regular unsecured card and get your deposit back.

Who Should Choose an Unsecured Credit Card

An unsecured card may be the better starting point if:

- You already have some positive credit history. Maybe you have a student loan in good standing or have been an authorized user on a family member’s card with a positive record. In that case, you might already meet unsecured credit card requirements for an entry‑level product. If you already have some history, reviewing first credit card options for beginners can help you choose wisely.

- You have stable, documented income. A full‑time job or a consistent, well‑documented self‑employment income can make it easier to qualify. If your income looks reliable and your other debts are manageable, lenders may feel comfortable approving you without a deposit.

- You prefer lower ongoing costs and more flexibility. Over the long run, unsecured cards often offer better combinations of fees, rates, and benefits, especially once your credit improves. If you can qualify now, you avoid tying up cash in a deposit and may find more no‑annual‑fee options.

- You want to avoid locking up savings. If you do not have spare cash for a deposit—or would rather keep that money in an emergency fund—going straight to an unsecured card can make sense, provided your approval odds are solid.

In short, if you can comfortably qualify for an unsecured card with reasonable terms, it is often simpler to start there. But if you are on the edge, a secured card may still be the faster route to better offers later because it gets your positive history started sooner.

Common Beginner Mistakes to Avoid

1. Applying for the Wrong Type of Card

A very common mistake is applying for multiple high‑end unsecured cards as a beginner, getting denied repeatedly, and only then considering a secured card. Each application can create a hard inquiry on your reports, and too many inquiries in a short period can make you look riskier.

As a beginner, it is important to honestly assess where you stand and choose either a secured or basic unsecured card that matches your profile.

2. Ignoring Fees and Terms

Some secured cards charge several different fees, and some unsecured cards for lower credit tiers also carry high costs. Beginners sometimes focus only on “Will I get approved?” and ignore the rest. Always read the fee schedule and understand:

- Annual fee (if any)

- Any monthly or maintenance fees

- Penalty fees for late payments

- APR for purchases and other transactions

A slightly higher deposit on a low‑fee secured card may be smarter than a no‑deposit unsecured card with heavy ongoing costs.

3. High Utilization

Using a large portion of your credit limit harms your credit score over time, even if you pay on time. With a small secured card limit, it is easy to accidentally use 50–80% of your limit with just a few purchases.

As a beginner, it helps to:

- Keep regular spending on the card modest

- Make one or more payments during the month, not just at the end

- Aim to have only a small balance showing on your statement

4. Closing Your First Card Too Early

Many beginners close their first secured card as soon as they get an unsecured card, especially once they get their deposit back. While it is okay to close cards, doing so quickly can shorten your average account age and remove a useful positive line from your history.

If the annual fee is low and the terms are reasonable, it can be beneficial to keep your first card open for a while—even after you get approved for a new unsecured card—so your credit file has more depth and history.

Difference Between Secured and Unsecured Credit Cards: Final Verdict

For true beginners, the secured credit card vs unsecured credit card decision usually comes down to one honest question: Could you realistically be approved for a decent unsecured card today at a reasonable cost?

- If the answer is no—because you have no credit, a limited file, past mistakes, or unstable income—a secured card is generally the better starting point. It is more forgiving, and it allows you to begin credit building with secured cards right away, instead of collecting a string of denials.

- If the answer is yes—you have some established, positive history and stable income—an unsecured card with low or no annual fee is likely the more efficient choice. You avoid tying up a deposit and may enjoy lower costs and more features over time.

In terms of pure credit building speed, there is usually no built‑in advantage to unsecured over secured or vice versa. What matters is that you get something you can qualify for, use it responsibly, and let time do its work. The right choice is the one that matches your current situation and sets you up for consistent, on‑time payments and low utilization.

Frequently Asked Questions

Can secured cards become unsecured?

Yes. Many issuers offer a “graduation” process. After a period of responsible use—often around 6 to 18 months—an issuer may review your account. If you have paid on time and kept balances under control, the issuer may convert your secured card to an unsecured card and refund your deposit. Some issuers may automatically review, while others may require you to request an upgrade.

Do secured cards build real credit?

Yes, as long as the issuer reports your account activity to the major credit bureaus. In that case, a secured card appears on your reports just like an unsecured card. On‑time payments, low utilization, and a longer account age will all help your credit profile over time. Before applying, check that the card you are considering does in fact report to the bureaus.

Which option is better when comparing the difference between secured and unsecured credit cards for first‑time users?

If you are a first‑time user with no or very little credit history, a secured card is often better simply because approval is more likely. It gives you a controlled environment to learn how credit works. If you already have some positive history and steady income, a simple unsecured card with low fees might be equally good or better. The “better” card is the one that you can handle responsibly and that fits your current profile.

Is a deposit a fee?

No. A secured credit card deposit is not a fee; it is collateral. As long as you keep your account in good standing and eventually close it or graduate to unsecured, your deposit should be returned to you. Fees, on the other hand, are charges you pay and do not get back (like annual or late fees). The deposit protects the lender, and the fees pay for the cost of offering and servicing the card.

Understanding the difference becomes easier once you know how credit cards work at a basic level.

Conclusion

Credit cards are tools, not shortcuts. A secured card does not magically fix your credit, and an unsecured card is not a sign that you can safely spend whatever you like. Both are simply lines of credit that can either help you or hurt you depending on how you use them. Understanding the difference between secured and unsecured credit cards helps beginners avoid rejections and build credit faster.

Understanding the difference between secured and unsecured credit cards—especially how approval works, how deposits and limits are set, and how fees and interest compare—puts you in control of your path. If you choose a card that matches your situation and you use it with patience and discipline, you can build a positive history that opens doors over time.

For most beginners, that means starting small, paying on time every month, keeping your balance low, and letting time do its work. Whether you begin with a secured card or qualify for an unsecured card right away, your long‑term success comes from consistent, responsible habits, not from the card type alone.

This article is for general educational purposes only and is not financial, legal, or tax advice. Credit card terms, approval criteria, fees, interest rates, and benefits vary by issuer, product, and individual user profile. Before applying for any credit product, review the specific terms and conditions carefully and consider seeking advice from a qualified professional who understands your personal situation.

Explore the Complete Credit Card Guide

Understanding the difference between secured and unsecured cards is just one step. To see how these options fit into the full approval process for gig workers and freelancers in the US, read our complete guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This article is for general educational purposes only and is not financial, legal, or tax advice. Credit card terms, approval criteria, fees, interest rates, and benefits vary by issuer, product, and individual user profile. Before applying for any credit product, review the specific terms and conditions carefully and consider seeking advice from a qualified professional who understands your personal situation.