Best starter credit cards for first-time users are designed to help beginners enter the credit system safely and build a strong financial foundation. Your first card can help you rent an apartment, buy a car, or qualify for better loan rates later—or it can create stress and debt if used carelessly

Introduction

A starter credit card is a tool designed to help people who are new to credit learn how to borrow and repay in a controlled way. Many first-time users focus on rewards or flashy perks, but what matters most at the beginning is building a positive credit history and avoiding expensive mistakes.

Common beginner mistakes include using the card like “extra money,” carrying balances they cannot pay off, applying for multiple cards at once, and treating minimum payments as a target instead of a safety net. These habits can quickly lead to debt, fees, and damaged credit, which may take years to repair. Starter cards exist to make the learning curve gentler: they usually have lower credit limits, simpler features, and more flexible approval rules for people with little or no prior credit history.

For most people, the “best starter credit cards for first-time users” are not about one specific product, but about the right type of card that fits their situation—secured, student, or basic unsecured. This article walks through those types, how they work, and how to choose your first credit card for beginners in a calm, step-by-step way.

On This Page

- Introduction

- What Is a Starter Credit Card?

- Types of Starter Credit Cards

- Secured vs Unsecured Starter Cards

- Features to Look for in a Starter Card

- How to Choose Your First Credit Card

- How Starter Cards Help Build Credit

- Common Mistakes First-Time Users Make

- Who Should Consider a Secured Starter Card

- Who Can Qualify for an Unsecured Starter Card

- Final Recommendations

- Frequently Asked Questions

- Can Gig Workers and Freelancers Get Starter Credit Cards?

- Conclusion

- Disclaimer

What Is a Starter Credit Card?

A starter credit card is a basic credit card designed for people with limited or no credit history, such as students, young adults, or recent immigrants. The main goal is not luxury perks, but to help you enter the credit system and prove you can borrow and repay responsibly.

These cards are typically more forgiving than premium cards in terms of approval criteria. They usually come with lower credit limits and fewer features, which helps keep the risk smaller while you learn. Many starter cards are structured so that on-time payments are reported to the major credit bureaus, allowing you to build a record over time.

If you are looking for credit cards for no credit history, you are the target audience for starter cards. They may not feel exciting, but they are often the most realistic and safest first step. Understanding how best starter credit cards for first-time users are structured can make it easier to avoid early credit mistakes.

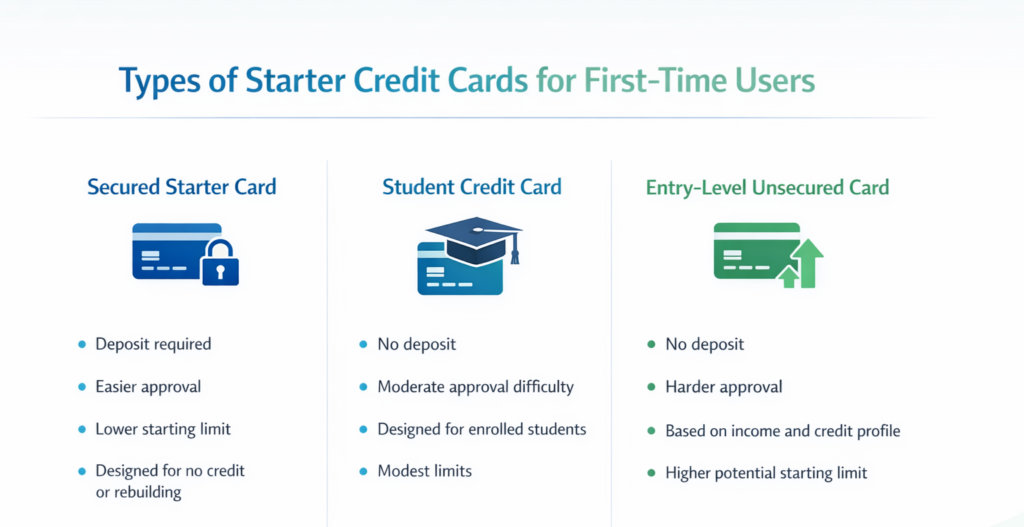

Types of Starter Credit Cards

There are three main categories of starter cards: secured cards, student cards, and entry-level unsecured cards.

Secured cards

A secured card requires you to put down a refundable cash deposit, which usually becomes your credit limit. For example, if you put down 300 dollars, your spending limit may be around 300 dollars. The deposit acts as collateral for the issuer, which makes it easier for beginners or people with damaged credit to be approved.

Aside from the deposit, a secured card works like a normal card: you use it for purchases and then pay the bill from your bank account. If you manage it well over time, some issuers may allow you to move to an unsecured card and get your deposit back.

Student cards

Student starter credit cards are unsecured cards aimed at college students and others in school who are at least 18 and often have limited income and no credit history. They usually do not require a deposit, but you may need to show some income (such as part-time work) or other support.

These cards are designed to help students build credit as beginners while managing everyday expenses like books, food, and transportation. Limits tend to be modest, and features are often simpler than non-student cards.

Entry-level unsecured cards

Entry-level unsecured starter cards are regular credit cards with lower limits and more basic terms, available to people with thin or no credit files, or fair credit. Approval is usually stricter than for secured cards and may depend heavily on income, existing accounts, or factors such as being an authorized user on a family member’s card.

These can be an option if you already have some credit history (for example, from a loan or authorized user status) and want to avoid a deposit. However, they may carry higher interest rates or fees than cards aimed at more experienced borrowers.chase+1

Types of starter cards

| Type of Starter Card | Who It’s For | Deposit Required | Approval Difficulty |

|---|---|---|---|

| Secured card | No credit history, rebuilding credit, prior denials | Yes, refundable | Easier |

| Student card | College students with little or no credit history | No | Moderate |

| Entry-level unsecured card | New workers, thin credit files, fair credit profiles | No | Harder |

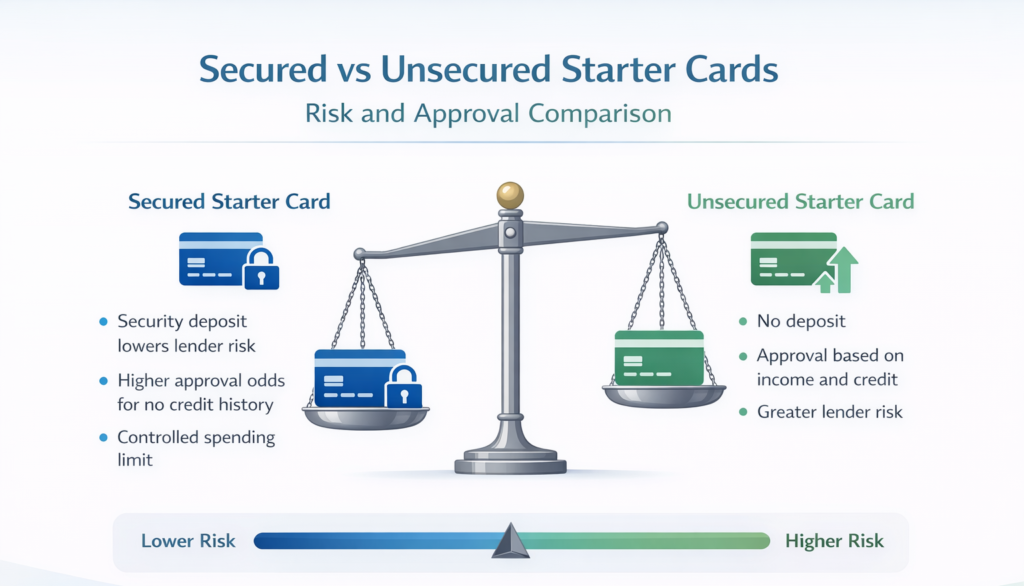

Secured vs Unsecured Starter Cards

At the core of “secured vs unsecured starter cards” is the question of who is taking more risk. With a secured card, you put down money upfront as a deposit, which lowers the lender’s risk and makes them more willing to approve you even if you have no credit history or past issues. With an unsecured card, there is no deposit; the issuer relies more on your income, existing credit record, and other factors. For a deeper explanation, read our guide on the difference between secured and unsecured credit cards.

Because of this, secured cards are often the first credit card for beginners with no credit, while unsecured starter cards may fit students with income or people who already have some positive history. Secured cards may have more fees or stricter terms, but they can be a reliable bridge toward better products. Unsecured starter cards may feel more “normal,” but approvals can be harder, and a weak application may lead to denials or low limits.

In practice, many beginners start with either a secured card or a student card and then move to unsecured cards as their profile improves. The best fit depends on whether you can afford a deposit, how strong your income is, and whether you have been denied for unsecured cards before.

Features to Look for in a Starter Card

When comparing the best starter credit cards for first-time users, focus less on flashy features and more on basic protections and costs. When comparing the best starter credit cards for first-time users, focus on simplicity, low fees, and credit-building potential rather than rewards.

Key features to look for:

- No or low annual fee

As a beginner, you generally want to keep your costs down. A no-fee or low-fee card makes it easier to keep the account open for years, which can help the length of your credit history. - Reports to all major credit bureaus

For a card to actually help you build credit as a beginner, the issuer must report your account and payment history to the major bureaus. If it does not, you are taking on risk without building the track record you need. - Reasonable interest rate for a starter card

Starter cards often have higher interest rates than top-tier cards, but try to avoid extremes. Even more important, plan to pay in full every month so interest never becomes a problem. - Clear, simple fee structure

Read the terms for late fees, foreign transaction fees, and any monthly or “maintenance” fees. Simple, transparent pricing is better for a first credit card for beginners. - Simple rewards (optional)

Some starter cards offer basic rewards, such as a flat cash-back rate on purchases. Rewards can be a nice bonus, but they should never drive your decision or tempt you to overspend.

If a card has complicated rules or many small fees, it may not be the best fit for someone just learning how to use credit.

How to Choose Your First Credit Card

Choosing how to start—secured vs student vs entry-level unsecured—comes down to a few key factors: income, approval odds, and your long-term plan.

Income considerations

Issuers are required to check that you can reasonably afford payments, so they look at your income and obligations. If your income is very limited or irregular, a secured card may be more realistic because the deposit lowers the lender’s risk. Students may be able to qualify for student cards using part-time income or certain other sources of support. Under federal consumer credit rules, issuers must consider your ability to repay before approving a credit card application.

Be honest when you estimate income and do not inflate the numbers. Doing so can violate the terms of your application and create problems later. Freelancers can also review our guide on secured credit cards for freelancers to understand deposit-based approval options.

Approval odds

If you apply for multiple cards in a short time and get denied, it can create unnecessary “hard inquiries” and frustration. To improve approval odds:

- Start with the most realistic type for your profile (secured or student if you have no history).

- Consider your recent history of denials; several recent denials suggest you should step back and choose a more accessible product.

- Keep other debts low to show room in your budget.

Long-term upgrade path

Starter cards are not meant to be your forever card, but they are also not just a temporary toy. Ideally, your first card should:

- Be affordable enough to keep open for many years.

- Offer a path to higher limits or better cards over time, especially if you pay on time and keep balances low.

- Fit the way you spend (for example, everyday purchases rather than rare, large expenses).

Think of your first card as a foundation tool: you want something stable, predictable, and easy to manage while you learn how to handle credit.

How to choose your first card

| Factor | Why It Matters | What Beginners Should Do |

|---|---|---|

| Income level | Affects approval and credit limit | Be honest; start with a card that matches your income reality |

| Credit history (or none) | Determines whether unsecured is realistic | If no history, favor secured or student cards |

| Ability to provide a deposit | Opens up secured card options | Use a secured card if you can afford a small refundable deposit |

| Willingness to keep card long term | Helps build length of credit history | Choose low-fee cards you can keep open for many years |

| Risk comfort | Lower limits can reduce damage from mistakes | If nervous, start with a low limit secured card |

| Upgrade goals | Future access to better cards and rates | Look for cards that can be upgraded or lead to better offers |

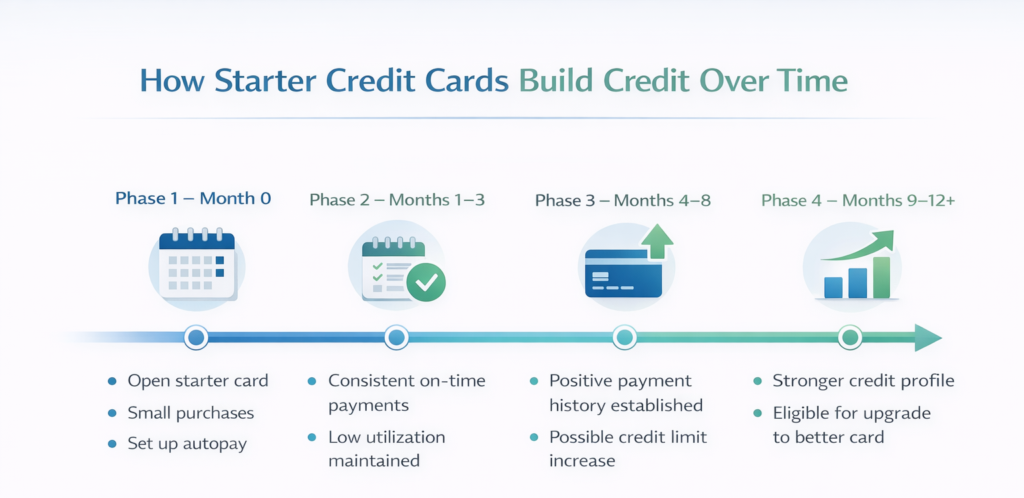

How Starter Cards Help Build Credit

Starter cards help build credit by reporting your behavior—good or bad—to the credit bureaus. Three main factors matter most for beginners: on-time payments, credit utilization, and length of history.

On-time payments

Payment history is usually the biggest part of most credit scoring models. Paying at least the minimum by the due date every month signals reliability, while late or missed payments can seriously hurt your score and stay on your record for years. As a beginner, making on-time payments should be your top priority, even if that means keeping your spending very low.

Credit utilization

Credit utilization means how much of your available limit you are using. For example, if your limit is 500 dollars and your balance is 250 dollars, your utilization on that card is 50 percent. High utilization suggests risk; lower utilization suggests you are using credit conservatively. A common beginner strategy is to keep balances well below the limit and, when possible, pay them down before the statement closes. To better understand how payment history and utilization affect your profile, review this official guide on how credit reports and scores work.

Length of history

The longer your accounts have been open and in good standing, the more data the scoring models have to work with. This is why experts often suggest keeping your first credit card open for many years, even if you later use other cards more. That long, positive track record can help stabilize your credit profile over time.

Together, these three elements allow a starter card to move you from “no history” to a solid beginning in 6 to 12 months, as long as you avoid major mistakes.

Common Mistakes First-Time Users Make

Many problems with starter cards come from a few predictable mistakes. Being aware of them can help you avoid them.

- Applying for too many cards at once

Each application can create an inquiry on your credit file. Multiple inquiries in a short time, especially with denials, can look risky and may reduce approval chances and scores temporarily. Multiple applications can lead to hard inquiries, which may temporarily impact your credit profile. Learn more about hard inquiries and credit checks here. - Maxing out small limits

Starter cards often have low limits, and it can be tempting to use all of it. High utilization can hurt your credit and makes it harder to pay the balance off quickly. - Treating the minimum payment as a goal

Paying only the minimum each month leaves most of the balance in place, which can lead to large interest charges and long payoff times. As a beginner, aim to pay your full balance monthly whenever possible. - Missing payments

A single late payment can trigger fees and damage your score. Setting up automatic payments for at least the minimum can be a simple protection. - Closing the first card too early

Many people close their first card when they “outgrow” it, not realizing that closing old accounts can shorten their average age of credit and slightly weaken their profile. Unless fees are high or the card is causing problems, keeping it open often helps.

Learning what not to do is a key part of using credit wisely.

Who Should Consider a Secured Starter Card

A secured starter card often makes sense when:

You are rebuilding after past mistakes

If you have prior late payments, collections, or other negative marks, secured cards are often specifically designed to help rebuild credit with responsible use.

You have no credit history at all

If you have never had a loan, card, or other account in your name, unsecured starter cards may be hard to get. A secured card allows you to show responsible use without the issuer taking as much risk.

You have been denied for unsecured cards

Several recent denials for student or entry-level unsecured cards can be a signal that you should step back and consider a secured option instead of continuing to apply.

Your income is low or irregular

Part-time work, gig income, or very modest earnings can make unsecured approvals harder. Putting down a small refundable deposit can improve your chances of approval with some issuers. If you earn through freelance or gig work and are unsure which type fits your situation, you can also explore our detailed guide on credit cards for gig workers and freelancers in the US to understand how income type affects approval.

In short, secured cards are often the best first credit card for beginners who need a more forgiving starting point and can afford to tie up a modest deposit for a period of time. If you earn through app-based or freelance work, our article on secured credit cards for gig workers explains how approval works with irregular income.

Who Can Qualify for an Unsecured Starter Card

Unsecured starter cards (including many student cards) can be a good fit when you already have some positive factors in your favor.

You may qualify for an unsecured starter card if:

- You are a student with some income

Many student-focused cards are built for college students with little or no credit, as long as they can show some income and meet age and enrollment requirements. - You have part-time or full-time work

Regular paychecks, even at modest levels, help issuers see that you can handle monthly payments. Stronger income can support higher starting limits and better terms. - You are an authorized user on someone else’s card

If a family member added you as an authorized user and maintained a positive payment history, that record may appear on your file and make unsecured approvals easier. - You already have some credit history

For example, if you have paid a small loan on time or have kept another account in good standing, you may be able to start directly with an unsecured starter card.

Unsecured starter cards can feel more flexible and require no deposit, but they do expect more from your application. If you are not sure, it can be helpful to start with the more certain option (often secured or student) rather than collecting denials.

Final Recommendations

When evaluating the best starter credit cards for first-time users, the right choice depends more on your financial situation than on flashy features.

Broadly:

- If you have no credit history and limited income, a secured card is often the most realistic and controlled starting point.

- If you are a student with at least some income, a student starter credit card can be a good way to build credit while managing everyday expenses.

- If you already have some positive history or stronger income, an entry-level unsecured card may be available without a deposit.

Across all types, the most important factor is how you use the card. Paying on time, keeping balances low relative to your limit, and avoiding unnecessary applications will do more for your long-term financial health than any single feature or reward program. Discipline matters more than card type.

Frequently Asked Questions

What is the best starter credit card for first-time users?

The best starter credit card for first-time users is usually the one that matches your situation while keeping costs and risk low. If you have no credit and limited income, a secured card is often the best fit. Students with income may prefer a student card, while those with some history can consider an entry-level unsecured card.

Focus on low fees, reporting to all major credit bureaus, and a simple structure you understand. Avoid chasing rewards if they tempt you to overspend. In most cases, the best starter credit cards for first-time users are the ones that prioritize low risk, simple terms, and consistent credit reporting.

Can I get a credit card with no credit history?

Yes. Many lenders offer credit cards for no credit history, including secured cards and student cards designed for beginners. These products are built to help you start a file and build a record through responsible use.

You may need to provide a deposit (for secured cards) or show proof of income or enrollment (for student cards). Over time, regular on-time payments can help you qualify for other types of cards.

Are secured starter cards safe?

Secured cards are generally safe as long as you understand how the deposit works. The deposit is typically held as collateral and may equal your credit limit; it is not used to pay your monthly bills unless you default. If you manage the account well and later close it or upgrade, you can usually get your deposit back.

To protect yourself, read the terms for how and when deposits are returned, and choose deposits only at levels you can afford to set aside for a period of time.

How long should I keep my first credit card?

In many cases, you should plan to keep your first card open for many years, even if you later get better cards. Keeping a long-term account in good standing can help the length of your credit history, which is one factor in many scoring models.

You might close it if it becomes too expensive (for example, high fees that no longer make sense) or if it no longer fits your needs. But in general, keeping your oldest account open, paid on time, and lightly used can be helpful.

Can Gig Workers and Freelancers Get Starter Credit Cards?

If you earn 1099 income, work on gig platforms, or freelance with variable income, starter credit cards can still be an option. However, approval may depend more heavily on income stability and documentation.

For gig workers with irregular income, secured starter cards often provide a more realistic starting point because the deposit reduces lender risk. Freelancers with part-time or project-based income may qualify for student or entry-level unsecured cards if they can demonstrate consistent deposits or tax filings.

If you want a deeper breakdown of how credit card approval works specifically for gig workers and freelancers, read our complete guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Conclusion

Your first credit card is more than just a piece of plastic—it is a training tool and a foundation for your financial life. Used wisely, a starter card helps you build a record that makes future steps, like renting, buying a car, or getting other loans, smoother and cheaper.

The safest path is usually to start simple: choose a card type that realistically fits your income and history, keep your spending modest, pay on time every month, and avoid chasing rewards or prestige. Over time, good habits will matter far more than which specific starter product you chose. Start small, stay disciplined, and let your credit grow gradually alongside your experience. For more beginner-friendly credit education guides, explore our full resource center.

Disclaimer

This article is for educational purposes only and is not financial, legal, or tax advice. Credit card terms, eligibility criteria, and offers vary by issuer and individual profile, and they change over time. Always review the latest terms and conditions directly from a card issuer and consider seeking personalized advice from a qualified professional if you have questions about your specific situation.