Introduction

For many gig workers and freelancers, the “best credit cards for gig workers with variable income” are not about rewards or perks. They are about getting approved reliably, managing cash flow safely, and building a predictable credit history over time.

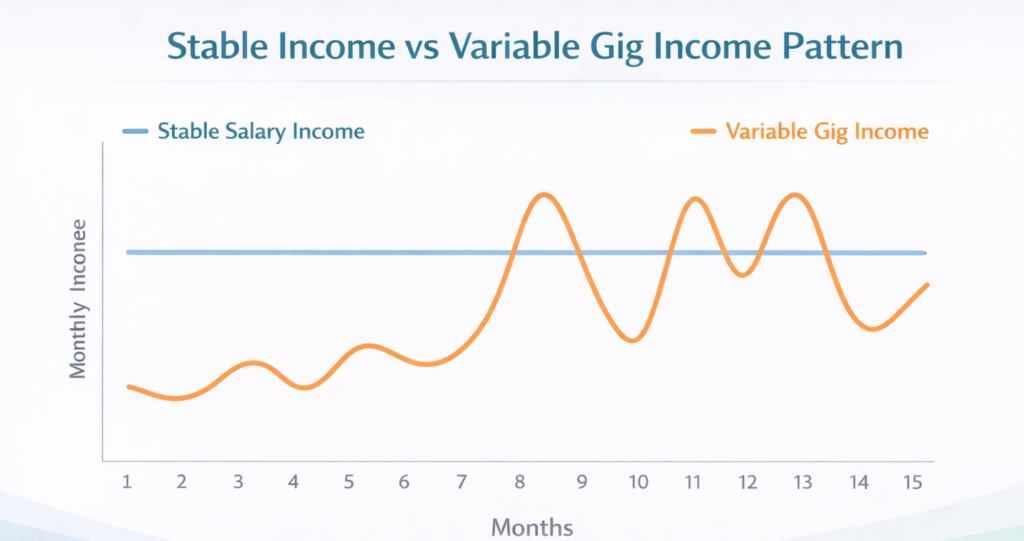

If you are used to paycheck work, credit card approval feels more straightforward: you list your salary, maybe your employer, and your income looks steady from month to month. With app-based gigs, multiple clients, and seasonal slowdowns, the same total yearly income can look very different to a lender because it arrives unevenly. That uneven pattern is what makes credit card approval with irregular income feel confusing.

In this context, “best” does not mean the flashiest or most generous card. It means card types that are more forgiving of fluctuating income, have lower barriers to entry, report to the major credit bureaus, and give you a clear path to better options as your profile improves. The goal is to match your current situation—not an ideal future version of your income—so you can grow your credit safely rather than stretching too far too early. That is why understanding the best credit cards for gig workers with variable income requires looking beyond rewards and focusing on approval flexibility and risk management.

On This Page

- Introduction

- Why income complicates approval

- How lenders see stable vs. variable income

- What makes a card good

- 7 card types that fit gig workers

- Secured vs unsecured for gig workers

- How banks evaluate gig worker income

- How to improve approval odds

- Common mistakes gig workers make

- Frequently asked questions

- Final recommendation

- Conclusion

- Disclaimer

Why income complicates approval

Lenders approve or deny credit cards based on how confident they are that you will pay on time, month after month. They look at your past behavior (credit history) and your current situation (income, existing debts, and other obligations) to estimate risk.

For someone with a stable paycheck, the numbers are easier to read: the lender sees the same or similar amount deposited on a regular schedule. With gig workers, the total yearly income might be similar or even higher, but the pattern is choppy—good months, slow months, and payouts from different platforms or clients. This inconsistency can make a lender more cautious, even when your overall earnings are solid. Lenders are also guided by ability-to-repay requirements for credit cards, which require them to consider whether an applicant has the financial capacity to make minimum payments.

Lenders care about both income consistency and total income. A high total income that swings wildly may look riskier than a lower, very predictable income. That is one reason variable income credit card approval can feel tougher than it “should,” based on your actual workload and effort.

How lenders see stable vs. variable income

Below is a simplified view of how key factors may look for a stable-income applicant versus a variable-income gig worker.

How key factors differ by income type

| Factor | Stable Income Applicant | Variable Income Applicant |

|---|---|---|

| Pay pattern | Same amount, same day each pay period | Amount changes month to month; timing can shift |

| Proof of income | Single pay stub series or simple documentation | Multiple deposits from platforms or clients, harder to summarize |

| Income volatility | Low; easy to predict future | Medium to high; lender may assume more uncertainty |

| Documentation clarity | Straightforward, one main employer | Mix of app payouts, transfers, sometimes cash deposits |

| Perceived repayment risk | Lower, if other factors are average | Higher, unless strong history or savings offsets the variability |

| Underwriting comfort | Higher, rules are clearer | Lower, more judgment and manual review may be needed |

What makes a card good

When you compare credit cards for gig workers, it helps to stop thinking about specific brands and instead focus on the underlying features that matter with fluctuating income. When evaluating the best credit cards for gig workers with variable income, the goal is to find card types that remain manageable even during slower earning periods.

Here are key traits that tend to make a card more suitable for someone with variable income:

- Flexible approval criteria

Cards aimed at beginners, credit builders, or people with limited credit history often place more weight on responsible use than on a single high income number. This can help with variable income credit card approval. - Lower minimum income expectations

While exact thresholds are rarely published, entry-level and secured products usually accept modest income levels, which is helpful when you are early in your gig career or building up your client base. - Reports to major credit bureaus

For credit-builder or secured credit cards for gig workers, this is critical. Reporting means your on-time payments can gradually improve your profile, opening the door to better options later. - Reasonable fees and clear terms

Complex fee structures or very high ongoing costs are risky if your income dips. Simpler, more transparent fees make it easier to plan. - Upgrade path

Some card types are designed to be stepping stones: use them responsibly for a period, and you may become eligible for higher limits or more flexible unsecured products without reapplying from scratch.

When you read about the best credit cards for freelancers and gig workers, look through the marketing and ask: “Does this card type give me some flexibility if I have a slow month?” and “Will using this card help my future approval chances?”

7 card types that fit gig workers

Below are the best credit cards for gig workers with variable income when viewed through the lens of approval flexibility, income stability, and long-term credit building. Instead of chasing specific brands, think in terms of seven broad card categories that can work well for self-employed and app-based workers with irregular income. For a broader overview of credit card options and how banks view different income types, check our guide on credit cards for gig workers and freelancers in the US.

1. Secured credit cards

Who they fit

- Gig workers with little or no credit history

- Anyone who has had past credit issues and needs a fresh start

- Self-employed people who can set aside a refundable deposit without harming day-to-day cash flow

Why they work for variable income

Secured cards are among the most accessible credit cards for gig workers because approval is partly backed by your cash deposit. The card issuer takes less risk, which can make them more open to applicants with thin files, past mistakes, or uneven income patterns. The credit limit often matches your deposit, so you have a built-in spending boundary.

Risks to consider

- You need to lock up cash for the deposit, which can be uncomfortable if your income is unpredictable.

- If you run the balance too close to the limit, your utilization ratio can spike and hurt your credit profile.

- Some secured cards carry higher fees, so it is important to read the terms carefully.

2. Student credit cards (for eligible gig-working students)

Who they fit

- College or training program students who also earn gig income

- Young adults with limited credit history but some ongoing income from app-based or part-time work

Why they work for variable income

Student cards often anticipate limited earnings and short work histories. As long as you can reasonably show enough income to support payments, the approval criteria can be more forgiving than many mainstream cards. For students doing delivery, rideshare, tutoring, or online gigs, this can be a gentle first step into credit.

Risks to consider

- Low limits can feel restrictive, which might tempt you to carry balances near the maximum.

- Mismanaging a student card—late payments or high utilization—can slow down your progress at a very early stage.

If a secured option interests you, our detailed guide on secured credit cards for gig workers breaks down how deposits and approval work with variable income.

3. Entry-level unsecured cards

Who they fit

- Gig workers with at least some established credit history (for example, a loan or older card)

- Freelancers whose income fluctuates but who can document a reasonable yearly total

Why they work for variable income

Entry-level unsecured cards do not require a deposit, yet they are still designed for people who are building or rebuilding credit. If you meet basic self-employed credit card requirements—verifiable income, manageable existing debts, and no recent severe delinquencies—these cards can offer a modest limit with room to grow.

Risks to consider

- Approval can still be denied if your documented income appears too unstable or your other debts are high.

- Some entry-level cards carry higher interest rates; carrying a balance on them can get expensive quickly if cash flow tightens.

4. Low-limit starter cards

Who they fit

- New gig workers who prefer a very small limit to “test-drive” credit

- People who are worried about overspending and want a built-in cap

Why they work for variable income

A low-limit starter card can be easier to approve because the lender’s risk is naturally limited by the small credit line. This appeals to applicants whose income is hard to predict month to month. You can use the card for a few recurring expenses, pay it off each month, and slowly demonstrate that you can handle credit even when your income has ups and downs.

Risks to consider

- If your limit is very low, one or two purchases can push your utilization ratio high, which may be viewed as riskier.

- It can be tempting to apply for multiple low-limit cards at once, which can lead to too many hard inquiries.

5. Credit-builder cards

Who they fit

- Gig workers who have struggled with past debt or collections

- Freelancers returning to credit after a period of being “credit invisible”

Why they work for variable income

Credit-builder cards focus less on rewards and more on consistent reporting to credit bureaus and clear rules for use. Many of these products are explicitly designed to give people with uneven finances a structured way to show regular, on-time payments. For gig workers, this can be a realistic bridge between no or damaged credit and more mainstream options.

Risks to consider

- Some credit-builder cards require fees that might not make sense if you already qualify for simpler starter cards.

- Progress can feel slow; these products are a long game, not a quick fix.

6. Cards with prequalification tools

Who they fit

- Anyone who wants to test the waters without multiple hard inquiries

- Gig workers comparing several options but unsure which will accept their income profile

Why they work for variable income

Prequalification lets you see your odds of approval using a soft inquiry that does not impact your credit score. This is especially valuable for credit card approval with irregular income because you can avoid wasting hard inquiries on cards that are unlikely to accept your situation. You can compare different card types and target the ones where you have a stronger chance.

Risks to consider

- Prequalification is not a guarantee; final approval can still change after a full review.

- It is easy to get carried away and apply for several cards after seeing prequalification, which can still result in multiple hard inquiries.

7. Cards designed for fair credit profiles

Who they fit

- Gig workers with some established history but not yet in “good” or “excellent” territory

- People who have a mix of on-time payments and a few older issues

Why they work for variable income

Cards marketed toward fair or average credit often sit between strict credit-builder products and more selective mainstream cards. They may accept applicants whose files show responsible use overall, even if income is not perfectly smooth. For freelancers and independent contractors, this can be a natural next step once your early starter or secured card history looks solid.

Risks to consider

- Terms can vary widely; some fair-credit cards are competitive, others are not.

- Limits might start low and only increase slowly, requiring patience and consistent use.

Card type overview for gig workers

| Card Type | Deposit Required | Approval Difficulty* | Best For |

|---|---|---|---|

| Secured Credit Cards | Yes | Easier | New or rebuilding gig workers who can set aside a refundable deposit |

| Student Cards | No | Easier–Moderate | Students with side gigs and limited history |

| Entry-Level Unsecured Cards | No | Moderate | Gig workers with some established credit and verifiable income |

| Low-Limit Starter Cards | No | Easier–Moderate | New users who want strong boundaries and small limits |

| Credit-Builder Cards | Sometimes | Easier–Moderate | Rebuilding credit or starting from “credit invisible” |

| Cards with Prequalification Tools | No | Varies | Anyone testing odds before a full application |

| Cards for Fair Credit Profiles | No | Moderate | Gig workers ready to move beyond basic starter or secured cards |

*“Approval Difficulty” is a general tendency, not a guarantee; each lender sets its own standards.

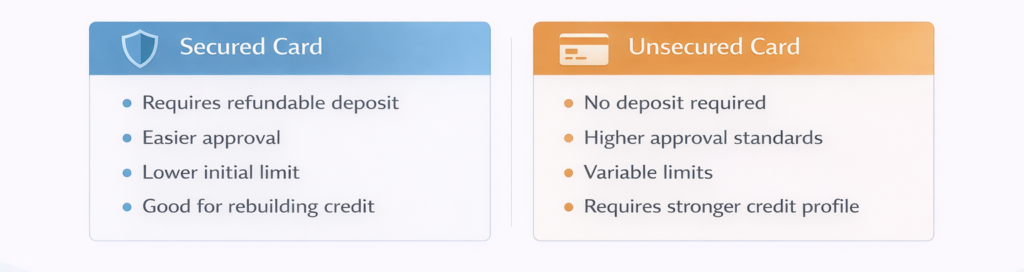

Secured vs unsecured for gig workers

Choosing between secured and unsecured cards is one of the most important decisions for gig workers with variable income. For many applicants, the best credit cards for gig workers with variable income often come down to choosing wisely between secured and unsecured structures.

Risk and safety trade-offs

With a secured card, the deposit reduces the lender’s risk, which can improve your chances if your income is uneven, your history is thin, or you have past issues. In return, you tie up your own cash, which becomes a form of self-insurance. If things go badly and you default, the issuer can use that deposit to cover part of the loss.

With an unsecured card, you do not need a deposit, which preserves cash for living expenses or business needs. However, the lender takes on more risk, so approval standards are often higher. For gig workers, this means better terms may be available, but only once your credit profile and documentation support it.

Cash flow considerations

If your emergency savings are thin, committing several hundred dollars to a secured deposit might feel risky. On the other hand, starting with an unsecured card and then facing high interest on carried balances during a slow period can also be risky. The right choice depends on:

- How much cash you can afford to set aside without jeopardizing rent, bills, or taxes

- How confident you are in maintaining at least the minimum payment during slow months

- Whether you already have a small emergency fund that can cover both card payments and essential expenses

In many cases, a secured card used very lightly—small recurring charges, paid in full each month—can be safer than a higher-limit unsecured card that tempts you to overspend when income is strong.

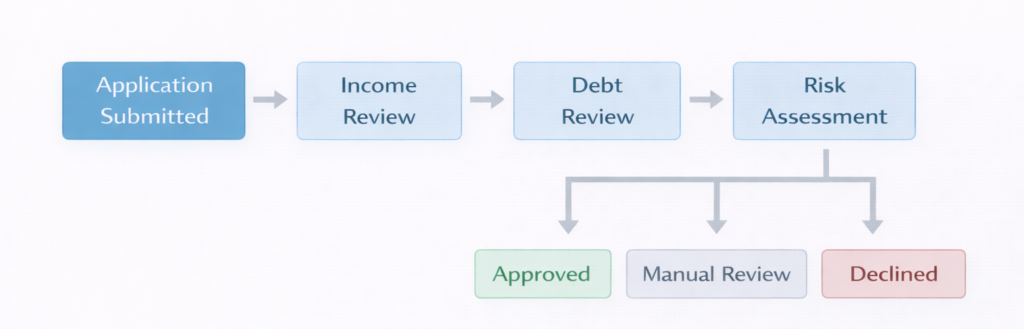

How banks evaluate gig worker income

Understanding how banks verify gig income can remove much of the mystery from the process. While each issuer has its own approach, most follow a few common steps when reviewing self-employed credit card requirements. For deeper insight into how issuers assess non‑W2 income, see our guide on credit card approval for 1099 income, which explains how lenders interpret irregular earnings.

Income averaging

Because gig income bounces up and down, lenders often look at an average over a period rather than a single high or low month. They may consider:

- Your stated annual income on the application

- Patterns visible in bank account deposits over several months

- Prior-year totals reflected in tax documents, if provided

From there, they form a picture of what a “typical” month might look like for you, rather than basing the decision on your busiest or slowest season.

Bank statements vs. tax returns

For many self-employed applicants, lenders rely heavily on bank statements to see actual money coming in and going out. Some may also review summaries from your most recent tax filing or documents that show your total 1099 earnings. The goal is not to audit your finances, but to confirm that your stated income is reasonable and consistent with what flows through your accounts.

If your reports show an upward trend over time and relatively stable monthly averages, that can support your case for variable income credit card approval.

Debt-to-income impact

In addition to income, banks look at your existing obligations—loans, other credit cards, and sometimes housing costs—to estimate how much of your monthly income already goes toward debt payments. This is often described as a debt-to-income ratio.

For gig workers, a high ratio can be especially concerning to lenders because it leaves less room for income dips. Keeping other debts modest and avoiding maxed-out credit lines helps show that you have capacity to take on a new card responsibly.

How to improve approval odds

You cannot control every part of a lender’s decision, but you can improve your position before you apply. These steps are especially useful for credit cards for gig workers and others with fluctuating earnings. Gig workers should review their free annual credit reports before applying to ensure there are no errors affecting approval.

1. Estimate income carefully

- Use realistic numbers, ideally based on your last 6–12 months of work, not your single best month.

- If your income has recently increased in a stable way (for example, you added a steady client), you can reasonably project that forward, but avoid optimistic guesses.

- Never overstate income; misrepresentation can hurt you if the bank requests documentation.

2. Manage your utilization

Utilization is the share of your available credit that you are using. Even if you pay in full, carrying very high balances relative to your limits can make you look financially stretched. For gig workers:

- Consider paying down balances before the statement closing date so reported balances stay modest.

- If you have multiple cards, spread purchases to avoid one card consistently appearing near its limit.

3. Time your application

Applying during or right after a strong earnings period can help, especially if your bank statements show steady or rising deposits. At the same time:

- Try to avoid applying immediately after taking on new debt, such as a large personal loan.

- Make sure you are not behind on existing obligations; recent late payments are strong negative signals.

4. Limit hard inquiries

Each full application usually involves a hard inquiry, which can temporarily lower your score. Applying for many cards in a short period makes you look riskier. To avoid this:

- Use prequalification tools when available to gauge your chances without multiple hard pulls.

- Focus on one or two card types that realistically fit your current profile instead of applying broadly.

Common mistakes gig workers make

Even careful applicants can make missteps that reduce their odds of approval or lead to problems after getting a card.

Frequent pitfalls

- Overstating income

It may be tempting to round up or assume best-case earnings, but if documentation is requested and does not match, it can damage your credibility. - Applying too aggressively

Submitting applications to several issuers in a short time can create a cluster of hard inquiries, which may concern lenders. - Ignoring existing debt and obligations

Focusing only on whether you can get approved, rather than whether you can comfortably manage payments during slow months, can set you up for stress.

Better approaches in practice

Thinking ahead about these mistakes can help you build a healthier long-term relationship with credit.

Common mistakes and better strategies

| Mistake | Why It Hurts | Better Strategy |

|---|---|---|

| Overstating income | Documentation may not match; lender may view you as higher risk | Use a 6–12 month average and be honest about fluctuations |

| Applying too aggressively | Multiple hard inquiries signal desperation or rising risk | Use prequalification when possible and target 1–2 realistic options |

| Ignoring existing debt | High overall obligations reduce capacity for new credit | Pay down balances and stabilize other debts before adding a new card |

| Relying on credit for slow months | Leads to growing balances and interest charges | Build a basic cash emergency fund to cover shortfalls |

| Maxing out starter limits | High utilization looks risky even if you pay in full | Keep recurring charges modest and pay early when possible |

Frequently asked questions

Can gig workers qualify for credit cards?

Yes. Many gig workers and independent contractors qualify for credit cards each year. Lenders are less concerned with your specific job title and more concerned with whether your income is sufficient and reasonably stable, your debts are manageable, and your past behavior suggests you will repay on time.

Does variable income automatically cause rejection?

No. Variable income does not guarantee rejection, but it can make approval more challenging if lenders cannot see a clear pattern or if your overall financial picture is tight. Strong factors—such as a consistent history of on-time payments, moderate existing debt, and a growing income trend—can offset some of the concern about fluctuations.

Are secured cards better for irregular income?

Secured cards are not automatically better, but they are often more achievable for gig workers at early stages. If you can afford the deposit and use the card lightly and responsibly, a secured card can offer a controlled way to build or rebuild credit. If your credit profile is already solid and your income, while variable, is well-documented, an unsecured starter card might be equally or more appropriate.

How much income do gig workers need?

There is no universal minimum number that guarantees approval. Each lender sets its own internal guidelines, and they rarely publish exact income thresholds. Instead, they look at income in context: your total debts, your housing costs, your history, and the size of the credit line you are requesting. Practically, higher and more consistent income improves your odds, but careful management of existing obligations matters just as much.

Final recommendation

If you are searching for the best credit cards for gig workers with variable income, start by honestly assessing where you are today:

- Do you have any open credit accounts with a clean recent history?

- How volatile is your income from month to month?

- Could you comfortably set aside a deposit without straining essential expenses?

If your credit history is thin or damaged and your income still swings widely, a secured card, credit-builder product, or low-limit starter card is often the safest entry point. These options tend to offer more flexible approval for self-employed applicants, while giving you a clear framework to show reliable payment behavior.

If you already have some positive history and your irregular income is trending upward and well-documented, an entry-level unsecured card, a student card (if you are in school), or a card designed for fair credit may be an appropriate next step. Regardless of type, long-term success comes less from choosing the “perfect” card and more from simple habits: charging only what you can repay, keeping utilization modest, paying on time every month, and applying only when your overall finances are ready for more responsibility. For broader official consumer guidance on credit cards, applicants can review educational material provided by federal regulators.

Conclusion

Credit approval is fundamentally about risk, not about whether you receive a W-2 or multiple 1099s. Variable income can work in your favor if you show lenders a pattern of responsible use, realistic borrowing, and steady progress over time.

For most gig workers, the path forward is to start simple, with card types that match your current situation, then let your history and income trends do the work of unlocking better options. With patience and planning, your irregular income does not have to block you from building a strong, flexible credit profile. For more beginner‑friendly credit education guides, explore our full resource library.

Disclaimer

This article is for general educational purposes only and does not constitute financial, legal, or tax advice. Individual approval decisions depend on each issuer’s policies and your personal financial profile, which can change over time. Always review the terms and conditions of any credit product carefully before applying or using it.