A Comprehensive Guide for Freelancers, Gig Workers, and First-Time Credit Builders

Introduction

Can you get a credit card with low or no credit history is a common question among freelancers, gig workers, first-time credit users, and recent immigrants. The short answer is yes—but with important caveats that anyone without credit history needs to understand.

No credit history, sometimes called having a “thin file” or being “credit invisible,” is fundamentally different from having bad credit. This distinction matters because it changes your options, approval odds, and timeline to building credit. Many people new to credit feel trapped: How can you build credit without a credit card, but you can’t get a card without credit? It’s a valid frustration, but the solution is simpler than you might think.

Why do so many people find themselves in this situation? The reasons are varied. You might be a young adult making your first credit application. You could be a freelancer or gig worker with inconsistent income documentation. You may have recently moved to the U.S. and have no local credit history. Or you simply paid for everything in cash and never needed credit before. Whatever brought you here, know that lenders have created specific pathways for people in your exact position. Understanding those pathways is the first step to building the credit you need.

On This Page

- Introduction

- What Low or No Credit History Actually Means

- Can You Get a Credit Card with Low or No Credit History?

- Credit Card Options for Low or No Credit History

- Why Freelancers and Gig Workers Face Extra Challenges

- Credit Score vs. Credit History Length

- Timeline: What Changes at Each Milestone

- Common Reasons Applications Get Denied with No Credit History

- How to Build Credit from Scratch: Step-by-Step

- What to Expect: Realistic Timeline

- How Long It Takes to Qualify for Better Cards

- How to Handle Denial: Next Steps

- Common Myths About No Credit History

- Frequently Asked Questions

- Q: Can you actually get approved for a credit card with zero credit history?

- Q: How fast can you build credit from zero?

- Q: Are secured credit cards worth it?

- Q: Are secured credit cards worth it?

- Q: Does self-employment make it harder to get a credit card with no history?

- Q: If I have no credit score, can income alone help me get approved?

- Q: How many times should I apply for a credit card?

- Conclusion

- Disclaimer

What Low or No Credit History Actually Means

Before diving into solutions, it’s essential to clarify what lenders mean by these terms, because precision matters when discussing credit.

No credit history means you have never applied for credit, or if you have, the accounts never reported to the major credit bureaus. When lenders pull your credit report, they find nothing—no accounts, no payment history, no score. This is sometimes called being “credit invisible.” You don’t have a score of zero; you simply don’t have a credit score at all yet.

Low or thin credit history means you have some credit activity reported to bureaus, but not enough to generate a reliable credit score. For example, you might have one credit card you opened six months ago, but that’s insufficient for scoring. A thin file also describes someone who has limited credit diversity—maybe just one card, with no loans or other credit types. Even when someone has limited history, understanding the minimum credit score required for credit cards helps set realistic approval expectations.

The critical thing to understand is how scoring systems view these profiles. The major credit bureaus use models that require a minimum threshold of account history before generating a score. Most models require at least one account to have been open and reporting for approximately six months. Until that threshold is met, your credit file remains unscorable.

Lenders treat these profiles differently than bad credit. When someone has bad credit, lenders have concrete evidence—late payments, defaults, collections—that predict future risk. With no credit history, lenders simply lack information. They’re making a decision based on incomplete data, which makes them cautious and likely to impose restrictions: lower credit limits, higher interest rates, or outright denial. To better understand why lenders hesitate with first‑time applicants, it helps to know how credit scores are calculated and which factors influence approval decisions.

Can You Get a Credit Card with Low or No Credit History?

Yes, you can get a credit card with no credit history. This is perhaps the most important question to answer clearly, because many people assume they cannot.

Why approval is possible. First, understand that issuers recognize there’s a massive market of creditworthy people with no credit history. Recent immigrants, young professionals, freelancers—these are good customers waiting to be served. Second, modern lenders use alternative approval criteria beyond traditional credit scores. They look at income verification, bank account history, employment stability, and payment patterns on utilities or rent. Some use specialized underwriting models that analyze your cash flow, savings patterns, and transaction history rather than relying solely on a thin credit file.

Why lenders still limit risk. Even with these alternatives, issuers are cautious. They don’t know your payment habits. You have no track record. So while they may approve you, they typically impose restrictions: smaller credit limits (often $300–$1,000 to start), higher annual percentage rates (APRs often above 20%), and in some cases, annual fees. These aren’t penalties—they’re the issuer’s way of managing risk on an unknown borrower.

Why your card options are restricted initially. You won’t have access to premium cards with annual fees, high rewards rates, or travel benefits. Those cards require established credit to qualify. Your options will be limited to entry-level products specifically designed for first-time users. But here’s the opportunity: if you use that card responsibly, you’ll start building credit that opens doors to better options within six to twelve months.

Credit Card Options for Low or No Credit History

Three main pathways exist for people with limited or no credit history. Each has distinct advantages and drawbacks.

Secured Credit Cards

A secured credit card requires you to place a cash deposit with the issuer. That deposit becomes your collateral and typically determines your credit limit. For example, if you deposit $500, you’ll receive a $500 credit limit. This isn’t borrowed money—it’s your own funds held in reserve.

Why they’re the easiest to get approved for: Banks face minimal risk because they hold your cash. Approval odds are very high, even with zero credit history. Many issuers advertise approval for applicants with no credit file at all.

The cost: You’re tying up your own money. If you deposit $500, you can’t access that $500 elsewhere. Most secured cards also charge annual fees ($25–$75 typically). Interest rates are often higher than unsecured cards (frequently above 20% APR). You receive minimal rewards, if any.

The benefit: After 6–12 months of perfect payment history, many issuers automatically convert your secured card to an unsecured card, returning your deposit. From there, you can access better cards with lower rates and actual rewards. This makes secured cards an excellent stepping stone—not a long-term solution, but a proven bridge to better credit.

Entry-Level Unsecured Cards

Some issuers, particularly fintech companies and certain banks, offer unsecured cards to people with no credit history. These cards don’t require a deposit. Instead, approval is based on income verification, employment history, and alternative data.

Approval requirements: You typically need demonstrated income (often $30,000+ annually) and a stable residency history. Some cards target specific groups, like students or recent graduates. Others use banking history—if you’ve maintained a checking account in good standing, that demonstrates financial responsibility.

Advantages: No deposit required, no money tied up. Some offer modest rewards (1% cashback on all purchases). No annual fees on many options. You’re building genuine credit without paying unnecessary costs.

Drawbacks: Higher APRs (typically 20%+) and lower initial credit limits ($300–$1,000). These cards are harder to qualify for than secured cards—approval isn’t guaranteed, even with decent income. You’ll need to show more documentation.

Store and Retail Cards

Department store, gas station, and online retailer cards are often the easiest cards to get approved for when you have no credit history. These cards can only be used at the issuing retailer or affiliated stores, but approval standards are significantly more lenient.

Why they’re easier: Retailers issue their own credit cards through their payment processing partners. They use their own underwriting criteria, which often emphasize your shopping history with them rather than your credit score. A customer with a good history of in-store purchases may get approved for a card despite having no credit history.

Best for credit building: If you already shop at a particular retailer, applying for their card can be your fastest approval. You can use it responsibly for 3–6 months, then apply for a broader card with better terms. The key is using it only for small purchases you can pay off in full each month—this demonstrates responsibility without carrying a balance.

Limitations: Single-use cards won’t help your credit grow as much as general-purpose cards because they report less varied spending activity. Approval for a retail card also doesn’t automatically translate to approval for a traditional bank card.

Getting a credit card with low or no credit history requires choosing the right starter option and applying at the right time.

Comparison: Card Types by Approval Difficulty and Requirements

| Card Type | Approval Difficulty | Deposit Required? | Typical Starting Credit Limit | Annual Fee Range | Best For |

|---|---|---|---|---|---|

| Secured card | Easiest | Yes ($200–$5,000) | $300–$5,000 | $25–$75 | First-time builders, zero credit |

| Entry-level unsecured | Moderate | No | $300–$1,500 | $0–$50 | Those with income documentation, students |

| Store/retail card | Easier | No | $300–$2,000 | Often $0 | Existing retailers, immediate approval |

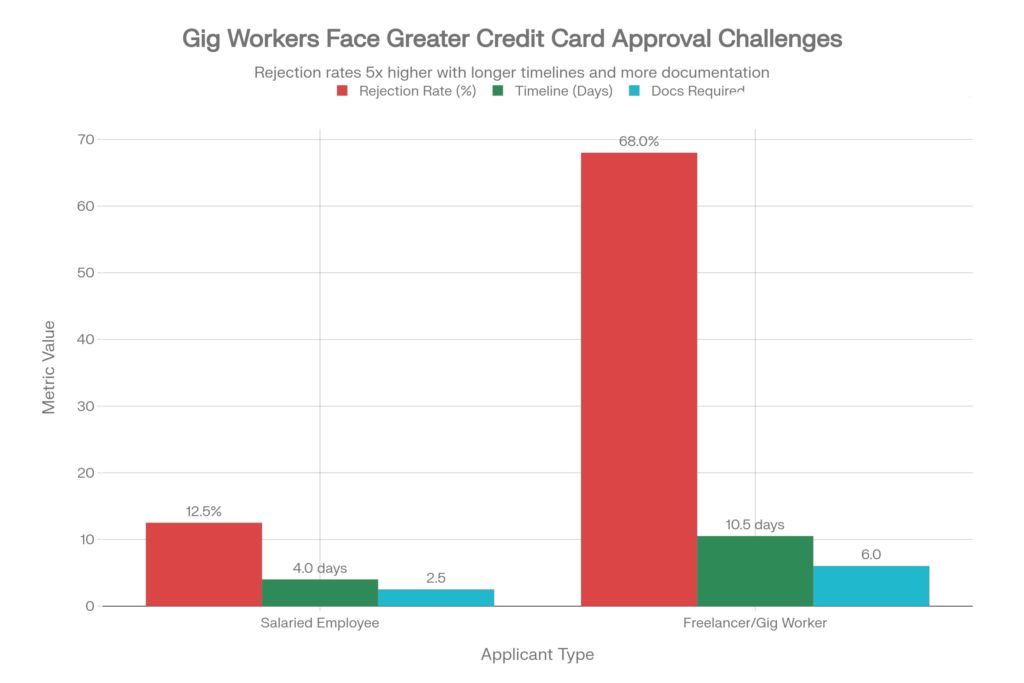

Why Freelancers and Gig Workers Face Extra Challenges

If you’re self-employed, a freelancer, or work gig economy jobs, getting a credit card when you have no credit history is more complex than it is for salaried employees. Lenders view your income differently, and that difference can tip the scales toward denial.

The income variability problem. A W-2 employee has predictable, verifiable income. An employer provides pay stubs showing consistent monthly earnings. A gig worker might earn $3,000 one month and $1,500 the next. Months with no income aren’t uncommon. Lenders worry: Can this person reliably pay a credit card bill when their income fluctuates? For self‑employed applicants, this is especially relevant because credit card approval for 1099 income often involves additional scrutiny around consistency and documentation.

Thin files plus self-employment stigma. Combine variable income with no credit history, and lenders see double risk. You’re both unpredictable in earnings and unproven in credit management. This combination makes approval harder than for a salaried person with no credit.

Why documentation matters more. Here’s where the advantage lies if you prepare properly. Lenders underwriting self-employed applicants increasingly use alternative data: your bank account deposits, invoices, contracts, and tax returns. These tell a story of your actual cash flow, not just stated income.

What helps your application as a self-employed person:

- Tax returns. If you filed taxes for the past two years, this is your strongest proof. Lenders look at your net profit averaged over two years. Even if one year was lower, demonstrating consistency matters.

- Bank statements. Three to six months of statements from your business checking account show deposits and spending patterns. Consistent deposits indicate reliable income.

- Invoices and contracts. If you have signed contracts showing ongoing work or a list of invoices showing recent billings, this demonstrates income predictability going forward.

- Payment history on other accounts. If you have utility bills, rent payments, or other recurring bills that you’ve paid on time, that demonstrates responsibility even without credit history.

Some lenders now use “alternative income verification” specifically for gig workers. They analyze your transaction data directly, bypassing the traditional tax return requirement entirely. This matters because many gig workers, particularly part-time or new gig workers, may not have tax returns yet. As your credit profile improves, you can explore suitable credit cards for gig workers and freelancers in the US that align with variable income and flexible work arrangements.

Credit Score vs. Credit History Length

A critical distinction exists between having a credit score and having sufficient credit history. Understanding this difference prevents disappointment when your application gets denied despite your responsible behavior.

Why a credit score may not exist yet. As mentioned earlier, most credit scoring models require at least six months of account history before generating a score. If you opened your first card three months ago, you won’t have a credit score yet. Credit bureaus will note your account exists, but they won’t convert that into a numerical score.

This creates a timing problem: you need a credit score to qualify for many cards, but you can’t generate a score without having open accounts. However, this is precisely why secured cards and retail cards exist—they approve without requiring a score, then help you generate one.

Why time matters more than income at the beginning. In the early months of credit building, your income is almost irrelevant compared to the passage of time. A person earning $100,000 with three months of credit history will have the same scoring challenge as someone earning $30,000 with three months of history. Both are unscorable. What matters is that six-month threshold. Lenders also evaluate credit history length because a longer record makes it easier to assess how consistently someone manages credit over time.

Once you cross that threshold and generate your first score, then income matters more—for qualifying for increases, additional cards, and loans.

Timeline: What Changes at Each Milestone

Credit building isn’t linear, but several predictable milestones occur as you build history. Here’s what generally happens:

| Credit History Length | What Changes | New Opportunities | What You Can’t Do Yet |

|---|---|---|---|

| 0–3 months | Account opened, activity reported | Monitor account, establish payment habit | Generate credit score, apply for better cards |

| 3–6 months | Payment history accumulating, utilization reported | Request credit limit increase from same issuer | Qualify for traditional unsecured cards from major issuers |

| 6–12 months | First credit score generated (typically 600–650s if perfect payments), score improves with each on-time payment | Apply for second card, qualify for cards with rewards, better APR rates available | Access premium cards, negotiate best rates on loans |

| 12+ month | Score continues improving, longer account age helps | Significant rate improvements on new cards, broader approval odds, qualify for better loan terms | Isn’t usually the limiting factor anymore—other factors dominate |

Common Reasons Applications Get Denied with No Credit History

Even when you follow all the right steps, denial still happens. Understanding why helps you improve your next application.

1. No score generated yet. You applied for a traditional unsecured card at six months when you only have three months of history. Issuers pulled your report, found no score, and denied you because their systems require a minimum score. Solution: Wait until the six-month mark, or apply for a secured card that doesn’t require a score.

2. Insufficient history. Slightly different from having no score—this means you have a score, but it’s based on limited data (one account, one type of credit). Issuers worry they don’t have enough history to predict behavior. Solution: Keep your first card open and use it consistently for 6–12 months before applying for additional cards.

3. High utilization on first card. You have a $500 limit, you’re carrying a $450 balance, and you apply for a new card. The new issuer sees your 90% utilization ratio and denies you for risk. Solution: Pay your balance down before applying. Keeping utilization under 30% dramatically improves approval odds.

4. Too many applications in a short time. Each application generates a hard inquiry on your credit report. Multiple inquiries in 30 days signal to lenders that you’re “credit shopping” aggressively. Several inquiries within 90 days significantly reduce approval odds. Solution: Space applications at least 3–6 months apart. If denied, wait six months before trying again.

5. Income verification issues. For self-employed applicants especially, your stated income doesn’t match your documentation. This red flag leads to automatic denial. Solution: Be conservative with stated income. Understate rather than overstate. If asked for documentation, provide tax returns and bank statements showing your actual average income.

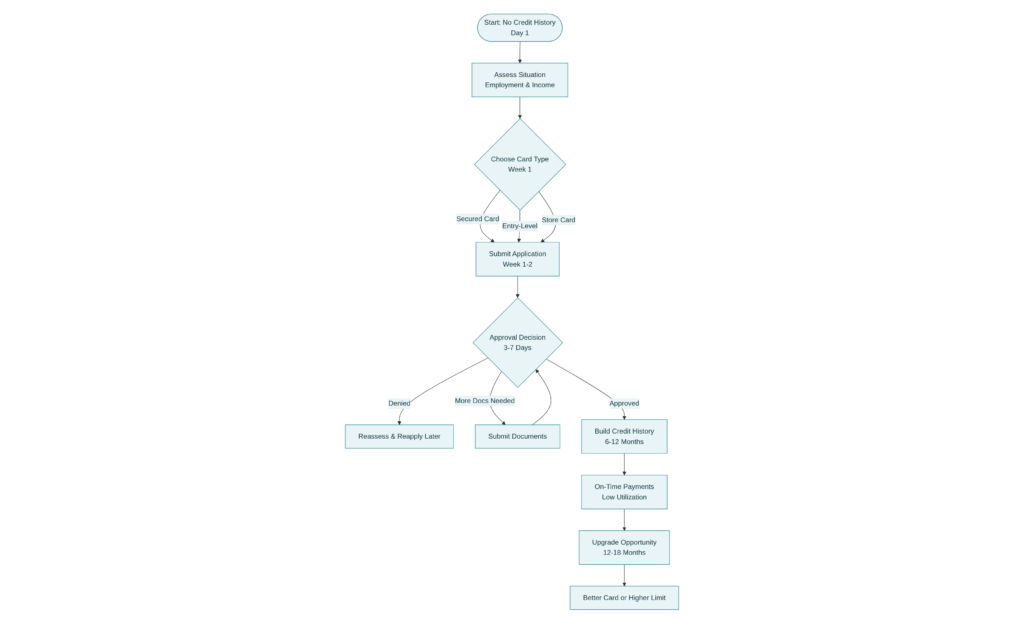

How to Build Credit from Scratch: Step-by-Step

Once you understand your options, here’s how to actually build credit responsibly.

Step 1: Choose Your First Card

Determine which category best fits your situation. If you have less than $1,000 to spare, a secured card is likely your best option. If you have stable employment and documented income, an entry-level unsecured card might work. If you’re a frequent shopper at a particular retailer, start there. The goal is approval—don’t aim for the “best” card, aim for the card you can actually get.e

Step 2: Apply with Accurate Information

Provide truthful information on your application. Income especially: be accurate or slightly conservative. Overstating income can be considered fraud, and it creates expectations you can’t meet. For self-employed applicants, calculate your average monthly net income from your most recent tax returns and use that figure. List all income sources you have, including side income, freelance work, or household income you’re responsible for.

Step 3: Use It Strategically

Don’t use your new card recklessly. Instead, use it for small recurring charges you’d make anyway—a monthly subscription, groceries, or gas. The goal is to create account activity that reports to credit bureaus monthly.

Most importantly: make small purchases you can pay off in full. This is the critical habit. If your card has a $500 limit, charge $50 on it, then pay it off in full when the bill arrives. Do this consistently, every month. Over six months, you’ll have six months of perfect payment history reported to credit bureaus.

Step 4: Pay On Time, Every Month

Payment history is the single most important factor in credit scoring (35% of your score). A single late payment can damage your credit significantly, especially when you’re starting from zero. Set up automatic payments or calendar reminders. Pay at least the minimum, but ideally pay the full balance.

Step 5: Keep Utilization Low

Credit utilization—the percentage of your available credit you’re using—accounts for 30% of your credit score. If you have a $500 limit and a $450 balance, your utilization is 90%, which hurts your score. Keeping utilization under 30% (so a $150 balance on that $500 limit) helps your score grow faster. This is why paying off your balance each month matters so much.

Step 6: Monitor Your Progress

After six months, check your credit report. Most credit scoring models require six months of reported activity to generate a first score. You can also monitor through free tools offered by many card issuers. Seeing that first score is encouraging, even if it’s not high (typically 600–650 if you’ve had perfect payments).

Once your profile improves, you can explore suitable credit cards for gig workers and freelancers in the US that match your income structure and credit stage.

What to Expect: Realistic Timeline

- Months 0–3: Account opens, you establish a payment routine. No score yet, but activity is being reported. Mentally, you’re building the habit of responsibility.

- Months 3–6: Halfway through, you have a quarter of your target history. This is when you might request a credit limit increase from your card issuer. Many will grant one if you’ve been reliable. This helps your utilization ratio.

- Months 6–9: Your first credit score appears. It’s likely modest (600–650 range), but it’s real. You become scorable. You can now apply for a second card or for modest credit increases.

- Months 9–12: Continued improvement. Each month of perfect payments boosts your score incrementally. By month 12, your score might be in the 650–700 range if you’ve been disciplined.

- Beyond 12 months: After a year, you’re no longer in the “first-timer” category. Better cards become available. Loans are easier to qualify for. Your thin file becomes a legitimate credit history.

How Long It Takes to Qualify for Better Cards

One of the most practical questions: when can I get a “good” card with rewards, lower rates, or no annual fee?

At 3 months: You probably can’t get approved for mainstream cards yet. However, some issuers consider you for their entry-level “step-up” cards or higher limits on your existing card. A credit limit increase (even $100–$200 more) helps your utilization ratio and shows issuers you’ve managed credit responsibly.

At 6 months: When your first credit score generates, you become eligible for a broader range of cards. Entry-level unsecured cards from major issuers become possible. These might have no annual fee and 1–1.5% cashback on purchases. If you have a secured card, you might convert it to unsecured. This is when you can apply for your second card.

At 12 months: Your score is likely in the 650–700 range if you’ve been perfect with payments. Now “good credit” cards become available. These might offer 2–3% rewards on certain categories, no annual fees, or slight rate discounts on future loans. You qualify for cards that most mainstream consumers use.

Important note: Approval odds improve with time, but they’re not guaranteed to jump overnight. Even at 12 months, you won’t get instant approval for a premium card with a $5,000 limit and travel benefits. But doors that were completely closed are now open.

How to Handle Denial: Next Steps

If your application gets denied despite your preparation, don’t panic. Denial is common, and it’s not permanent.

Request the adverse action letter. By federal law, the issuer must explain why you were denied. You’ll receive a letter within 7–10 days. It might say “insufficient credit history,” “low income,” or “too many recent inquiries.” This letter tells you exactly what to fix.

Review your credit report. Pull your free credit reports from the official source. Check for errors. Sometimes denial occurs because of incorrect information on your report (like a duplicate account or wrong address). If you find an error, dispute it immediately.

Wait before reapplying. Don’t apply for the same card again immediately. Each application creates a hard inquiry that stays on your report for 12 months and temporarily lowers your score. Wait at least three to six months before applying to the same issuer again. Meanwhile, apply your energy to the card you do have—use it responsibly, build history, and improve your score.

Consider alternatives while waiting. If you were denied by a traditional issuer, apply for a secured card or retail card instead. Getting any approval and building more history is better than waiting and hoping. Once you have more history, the card that denied you before might approve you.

Common Myths About No Credit History

Myth has a way of spreading about credit, especially among people navigating it for the first time. Let’s correct the most damaging ones.

Myth: “No credit history is worse than bad credit.” This is false. Bad credit is objectively worse. Bad credit shows concrete evidence you mismanaged debt: late payments, defaults, collections. That’s a proven problem. No credit history is an unknown—you might be perfectly responsible. Lenders prefer the unknown to proven irresponsibility. Plus, you can build credit from zero much faster (six months to a decent score) than you can rebuild from bad credit (two to five years or more).

Myth: “My income is more important than credit history when I’m first starting.” Not really. In the beginning, time matters more than income. A person earning $25,000 with one year of credit history is more likely to get approved for a card than someone earning $60,000 with two months of history. Income matters more once you have some history. Early on, lenders are primarily asking: “Have you shown responsibility over time?” Your income determines the amount they’ll lend, not whether they’ll lend at all.

Myth: “Once I get one credit card, I should immediately get more.” Not necessarily. Getting one card and using it responsibly for 6–12 months is better than opening multiple cards rapidly. Multiple inquiries in a short time damage your score and signal risk to lenders. Build a foundation with one card first, then thoughtfully add a second around the 6–12 month mark.

Myth: “I should carry a small balance on my credit card to build credit faster.” This is absolutely false. Carrying a balance costs you money in interest and doesn’t help your score. In fact, carrying a high balance (high utilization) hurts your score. Perfect credit building means paying off your balance in full each month. You build credit through responsible use and perfect payment history, not through paying interest.

Frequently Asked Questions

Q: Can you actually get approved for a credit card with zero credit history?

A: Yes. Secured cards approve people with zero history regularly. Entry-level unsecured cards approve people with demonstrated income and clean records. Store cards are often the easiest. Approval isn’t guaranteed, but it’s definitely possible, especially with a secured card.

Q: How fast can you build credit from zero?

A: You can generate your first credit score in six months if you open an account and make perfect payments. From there, meaningful improvement happens over 6–12 months. Going from “no score” to a 700+ score typically takes 12–18 months of perfect payment behavior.

Q: Are secured credit cards worth it?

A: You can generate your first credit score in six months if you open an account and make perfect payments. From there, meaningful improvement happens over 6–12 months. Going from “no score” to a 700+ score typically takes 12–18 months of perfect payment behavior.

Q: Are secured credit cards worth it?

A: Yes, if you’re starting from zero. The deposit ties up your money temporarily, and fees are real. But within 6–12 months, you’ll graduate to an unsecured card and get your deposit back. For the cost and inconvenience, you get proven credit building. If you can’t qualify for an unsecured card, it’s worth it.

Q: Does self-employment make it harder to get a credit card with no history?

A: Yes, slightly. But not prohibitively. Self-employment makes approval harder primarily if you can’t document income (no tax returns, inconsistent bank deposits). If you can show bank statements, tax returns, or invoices, modern lenders have tools to evaluate you. Freelancers and gig workers get approved regularly; it just requires more documentation than a W-2 employee needs.

Q: If I have no credit score, can income alone help me get approved?

A: Income helps, but it’s not enough alone. Lenders might look at whether your income is sufficient to cover a credit limit. They might even pre-approve you for a specific limit based on income. But income doesn’t replace credit history. Alternative approval criteria consider income plus bank account history, employment stability, and other factors. Income is one piece, not the whole puzzle.

Q: How many times should I apply for a credit card?

A: Apply once to one issuer at a time. Each application creates a hard inquiry. Space applications at least three to six months apart. If denied, wait at least six months before reapplying. Multiple applications in rapid succession damage your score and signal desperation to lenders.

Conclusion

Getting a credit card with low or no credit history is absolutely achievable. It’s not the easiest path—lenders are appropriately cautious about unknown borrowers—but it’s a proven path. Thousands of young adults, freelancers, recent immigrants, and others start this journey every year and succeed.

The key isn’t finding a magical card that instantly approves anyone. The key is understanding which options are actually open to you, choosing the most appropriate one, and then using it as a deliberate tool to build credit. A secured card, an entry-level unsecured card, or a retail card isn’t the card you’ll have forever. It’s the card that helps you get to the cards you actually want.

Patience and consistency are the real determinants of success. Six months of perfect on-time payments is more powerful than almost any other factor. One year of consistent, responsible use transforms your financial standing. By that point, doors that were completely closed begin to open.

No credit history is a temporary condition, not a permanent limitation. Start with what’s available to you today, use it responsibly, and watch your options expand over the coming months. The credit system is built to allow people to enter it—you just need the right starting point. A credit card with low or no credit history is possible when you build consistency and avoid common beginner mistakes.

For more practical guides on building credit and choosing the right cards, visit UncoverCards.

Disclaimer

This article is provided for educational purposes only and should not be construed as financial, legal, or tax advice. Credit card approval criteria, terms, and availability vary significantly based on individual circumstances and issuer policies. Readers should consult directly with lenders regarding their specific eligibility and terms. The information in this article reflects general credit market practices but is not a guarantee of approval or specific terms. Individual financial situations are unique, and outcomes will vary. Seek professional financial advice if you have questions specific to your circumstances.