Executive summary

Debt-to-income ratio affect credit card approval decisions because lenders evaluate how much of your income is already committed to existing debt payments. When people apply for a new credit card, they tend to focus on credit scores and payment history. Yet many lenders also look closely at a simple number called the debt-to-income ratio (DTI), which compares monthly debt payments to gross monthly income. This ratio helps lenders judge how much additional debt an applicant can realistically handle.

A lower DTI generally signals that an applicant has room in their budget for new obligations, while a higher DTI suggests that income is already stretched by existing loans and credit card balances. For credit card applications, DTI can influence whether the application is approved at all and, if it is, what starting credit limit the issuer is comfortable offering.

This report explains what DTI is, how it is calculated, what ranges lenders often prefer, and how it interacts with other factors in credit card approval. It also highlights special considerations for freelancers and gig workers, who often have variable income that can complicate DTI calculations. Finally, it outlines practical strategies applicants can use to improve their DTI before applying for a card. Understanding how debt-to-income ratio affect credit card approval helps applicants evaluate whether their current debt levels are likely to influence a lender’s decision.

On This Page

- Executive summary

- Why Debt-to-Income Ratio Affect Credit Card Approval

- What is debt-to-income ratio?

- How debt-to-income ratio is calculated

- What debt-to-income ratios lenders prefer

- How Debt-to-Income Ratio Affect Credit Card Approval Decisions

- Debt-to-income ratio for freelancers and gig workers

- How to improve your debt-to-income ratio

- Common mistakes applicants make

- Applying with unusually high balances

- Ignoring existing loan obligations

- Misunderstanding minimum payments

- Why does debt-to-income ratio affect credit card approval?

- What DTI is considered “safe” for credit card approval?

- Can freelancers qualify with a higher DTI?

- Does income volatility matter, or only the average?

- How applicants should think about DTI before applying

- Conclusion

- Disclaimer

Why Debt-to-Income Ratio Affect Credit Card Approval

Credit scores summarize how someone has handled credit in the past: whether bills were paid on time, how long accounts have been open, and how much of available credit is being used. However, a score does not show how much income a person currently earns or how heavily that income is already committed to debt payments.

Lenders therefore often pair a credit score review with an assessment of the applicant’s current capacity to take on more debt. DTI gives them a quick snapshot of this capacity by measuring the share of income being used for required debt payments each month. Two people with identical credit scores can have very different DTIs, and the one with the lower DTI will usually look safer to a cautious lender.

A common misunderstanding among applicants is assuming that a strong credit score guarantees automatic approval for any credit card. In reality, if an applicant’s DTI is high—because of large student loans, an auto loan, a mortgage, or high existing card balances—some lenders may either decline the application or approve it with a lower initial limit.

What is debt-to-income ratio?

The debt-to-income ratio is the percentage of an individual’s gross monthly income that goes toward paying debts. “Gross” income means income before taxes and other deductions. DTI is expressed as a percentage rather than a dollar amount so lenders can compare applicants with different income levels using the same yardstick. Debt‑to‑income ratio is widely used by lenders when evaluating whether a borrower can manage additional debt obligations.

In simple terms, DTI answers the question: “Out of every dollar of income before taxes, how many cents are already spoken for by debt payments?” A lower percentage leaves more room in the budget for new payment obligations; a higher percentage leaves less room.

DTI is different from a credit score. A credit score reflects past behavior with credit accounts, while DTI focuses on the current relationship between income and required payments. Someone can have excellent credit but a high DTI if they carry several large loans, and another person can have modest credit but a low DTI if they have little existing debt.

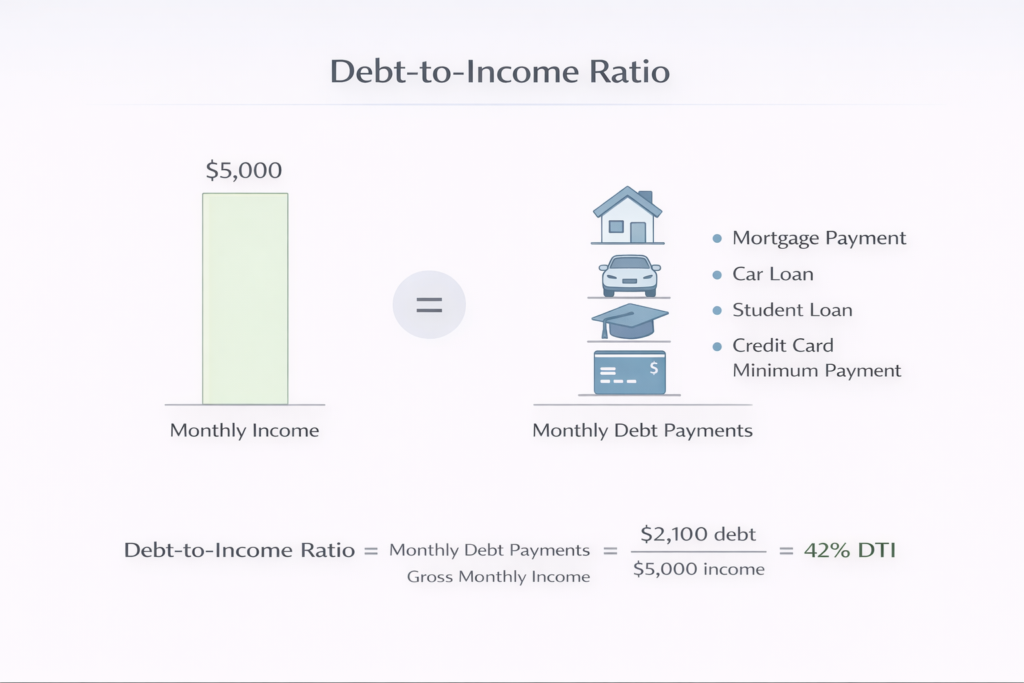

Example: monthly income vs. monthly debt

The following example illustrates how DTI compares income and debt.

| Item | Monthly amount |

|---|---|

| Gross monthly income | 5,000 |

| Mortgage or rent payment | 1,400 |

| Auto loan payment | 300 |

| Student loan payment | 250 |

| Credit card minimum payments | 150 |

| Total monthly debt payments | 2,100 |

In this example, total monthly debt payments are 2,100 and gross monthly income is 5,000. The DTI is 2,100 ÷ 5,000, or 42 percent. That means 42 percent of the person’s gross income is already committed to debt payments each month.

How debt-to-income ratio is calculated

The standard formula for DTI is:

Debt-to-income ratio=Gross monthly incomeTotal monthly debt payments×100%

To apply this formula, a lender first totals the applicant’s recurring monthly debt obligations, then divides that total by the applicant’s gross monthly income. Many financial education resources explain that calculating DTI helps borrowers understand how lenders evaluate debt capacity before approving new credit.

What counts as “monthly debt payments”

When lenders calculate DTI, they generally include:

- Housing payments: rent or mortgage payments.

- Installment loans: auto loans, personal loans, and student loans.

- Credit card obligations: usually the required minimum payments, not the full balance.

- Other formal debt payments: such as personal loans from financial institutions, and required payments like alimony or child support where applicable.

They do not usually include everyday living expenses like groceries, utilities, insurance premiums, or transportation costs in DTI, even though those still affect a person’s budget.

Revolving vs. installment debt

DTI captures both revolving and installment debt, but they behave differently.

- Installment debt includes loans with fixed payments over a set time, such as mortgages, auto loans, and most student loans. The monthly payment amount is usually stable until the loan is repaid.

- Revolving debt includes credit cards and some lines of credit. Payments can vary based on the balance, and the borrower can carry a balance from month to month.

When calculating DTI, lenders use the current required monthly payment amounts. For credit cards, they typically use the minimum payment required on the statement, even if the borrower normally pays more.

Because credit card minimum payments are often calculated as a small percentage of the balance, large card balances can raise DTI even if the borrower only sees a modest minimum due on each account.

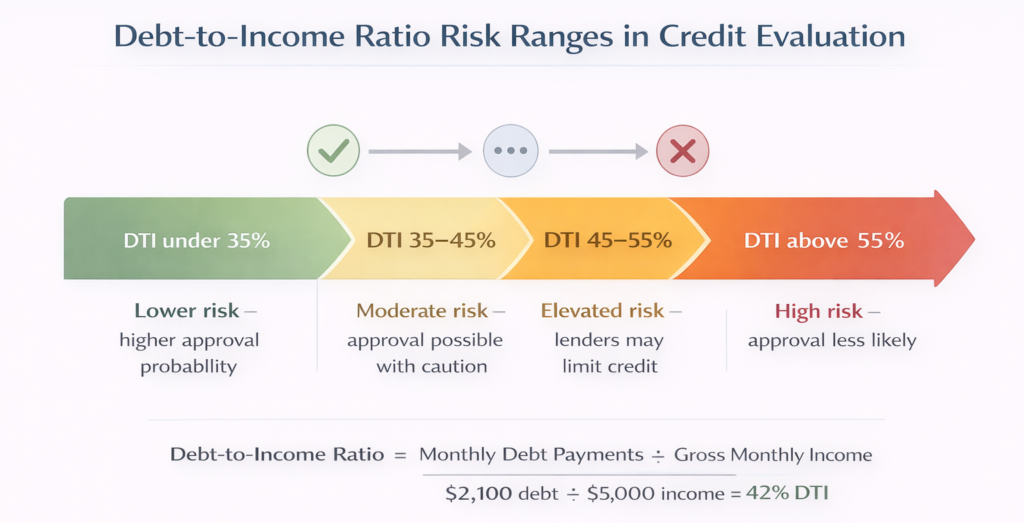

What debt-to-income ratios lenders prefer

There is no single nationwide DTI cutoff that all lenders follow, and credit card issuers may have internal guidelines that differ by product and risk appetite. However, certain patterns are common across many types of consumer credit.

Lower DTIs are generally viewed as safer. Ratios in the lower 30s or below often signal that a borrower has room in the budget to take on more debt, especially if other aspects of the application are strong. Mid-range DTIs may still qualify, but lenders might look more closely at credit history, income stability, and cash reserves. Higher DTIs signal that debt is already taking a large share of income, which increases the risk of missed payments if income falls or expenses rise.

Typical ranges and risk interpretation

The table below summarizes how many lenders tend to interpret broad DTI ranges. Individual policies vary, and these ranges are only general guidelines.

| DTI range | Risk level (general) | Possible approval outcome* |

|---|---|---|

| Under 35% | Lower risk | Strong chance of approval if other factors are sound |

| 35%–45% | Moderate risk | Approval possible; terms or limits may be more conservative |

| Above 45% | Higher risk | Approval may be difficult; if approved, limits may be lower |

*Actual outcomes depend on each lender’s policies, the type of account, and the overall application profile.

For credit card applications, a DTI that is already high can prompt a cautious issuer to decline the application or to approve a smaller credit line to limit additional monthly obligations.

How Debt-to-Income Ratio Affect Credit Card Approval Decisions

This is where debt-to-income ratio affect credit card approval decisions most directly, because lenders compare existing monthly obligations with the applicant’s income capacity.

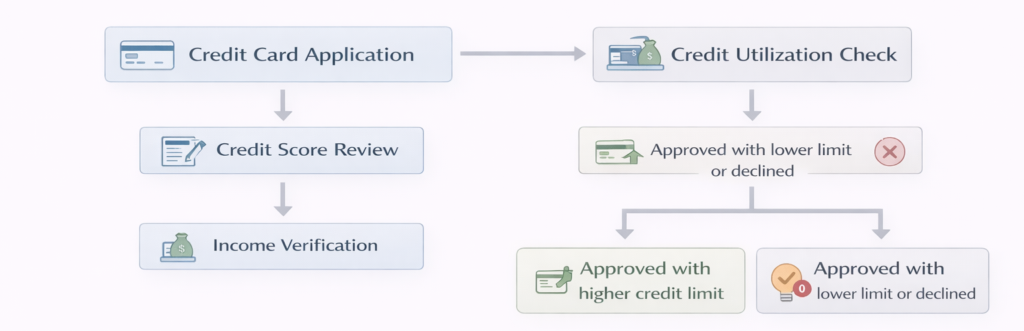

When reviewing a credit card application, a lender typically considers several elements:

- Credit report and score.

- Declared income and employment situation.

- Existing debt levels and required payments.

- Other information from the application.

DTI connects the income and debt components. A higher DTI indicates that, relative to income, a larger portion is already committed to required payments. This can affect both the approval decision and the initial credit limit.

Impact on approval decisions

If an applicant has a strong credit history but a high DTI, a lender may be concerned that even a modest additional payment could strain the budget. From a risk perspective, this raises the chance that the borrower could struggle to make payments if anything unexpected happens, such as a temporary income drop or an emergency expense.

In such cases, some lenders may decline the application despite a good credit score. Others may approve but remain conservative with the credit limit so that the potential new minimum payment does not push DTI into an uncomfortably high range.

Impact on starting credit limits

DTI can also influence the size of the credit line offered. Applicants with lower DTIs and stable income may qualify for higher starting limits than applicants with similar credit scores but higher DTIs.

When a lender models potential worst-case scenarios, a larger credit line could lead to a larger possible balance and higher minimum payments. If the applicant’s existing DTI is already elevated, the lender may cap the limit to keep the projected DTI within its comfort zone.

Interaction with credit utilization

DTI and credit utilization are separate concepts but can reinforce one another. DTI focuses on required payments versus income, while credit utilization measures how much of available revolving credit is currently in use.

High credit card balances tend to increase both utilization and DTI. Utilization matters for credit scores, and higher utilization can signal heavier reliance on credit. Higher balances also raise minimum payments, which in turn raise DTI. When both ratios are elevated, lenders may view the application more cautiously. Understanding how lenders review credit reports and existing obligations can help applicants prepare stronger credit applications.

Debt-to-income ratio for freelancers and gig workers

Freelancers, independent contractors, and gig workers face extra challenges when it comes to DTI because their income can fluctuate from month to month. Lenders aim to understand an average or sustainable level of income rather than just taking the highest recent month at face value. For applicants with irregular earnings, debt-to-income ratio affect credit card approval even more because income stability becomes part of the lender’s risk assessment.

Freelancers and gig workers often deal with irregular income, which can make credit approval more complicated compared with traditional salaried applicants. To understand suitable card options, you can explore credit cards for gig workers and freelancers

Variable income and averaging

For applicants with nontraditional income, lenders often look at income over a longer period—commonly the last one or two years—and calculate an average monthly figure. They may base this on tax returns, year-to-date earnings, and other verified documentation.

If income trends are upward and stable, the lender may be more comfortable using a recent average. If income is highly volatile or trending downward, the lender may take a more conservative view, which effectively raises the DTI calculation.

Documentation lenders may review

Freelancers and gig workers should be prepared to document income clearly. Depending on the lender, this can include:

- Tax returns for recent years.

- Forms that summarize non-employee compensation.

- Bank statements showing regular deposits from clients or platforms.

- Invoices, contracts, or other records that support ongoing work and income.

The goal is to demonstrate that income is consistent enough to support existing debts and any new credit obligations. Clear documentation can make it easier for a lender to calculate an accurate DTI and to see that the applicant is managing variable income responsibly. Understanding how lenders evaluate variable income can help gig workers choose the best credit cards for gig workers with variable income.

How to improve your debt-to-income ratio

Because DTI is a ratio, applicants can improve it either by reducing monthly debt payments or by increasing gross income. In practice, many people focus first on steps that reduce debt, because those are often more within immediate control.

Practical strategies to lower DTI

Common approaches include:

- Paying down revolving balances so minimum payments fall over time.

- Avoiding new loans or large purchases on credit before applying.

- Considering consolidation or refinancing where it leads to a genuinely lower monthly obligation.

- Increasing or stabilizing income through additional work hours, side income, or more predictable contracts.

The table below summarizes how these strategies affect DTI.

| Strategy | Why it helps DTI | Best time to use it |

|---|---|---|

| Pay down credit card balances | Reduces minimum payments and total monthly debt | Several months before applying if possible |

| Pay off smaller installment loans | Eliminates whole payment from the DTI calculation | When close to the payoff point on a small loan |

| Avoid taking on new debt | Prevents DTI from rising before application | In the months leading up to an application |

| Consolidate or refinance at lower rate | Can lower total required monthly payments | After comparing total costs and terms |

| Increase or stabilize income | Raises the denominator in the DTI ratio | When sustainable income changes are realistic |

For most applicants, small improvements can add up. Paying down even a few hundred dollars of revolving balances, or postponing a new loan until after a card application, can prevent DTI from creeping into a range that worries lenders. Applicants with limited credit history or unstable income sometimes consider secured credit cards for freelancers as a safer starting point.

Common mistakes applicants make

Many applicants unintentionally work against themselves by overlooking how their current behavior affects DTI at the moment they apply.

Applying with unusually high balances

Some people apply for a new credit card right after a period of heavy spending, such as holidays or a major purchase. Even if they plan to pay down those balances soon, the lender sees higher minimum payments at the time of application, which raises DTI. Applying when balances are lower usually presents a stronger picture.

Ignoring existing loan obligations

Applicants sometimes focus on the new card’s potential limit and rewards while overlooking how their existing auto, student, or personal loans affect their overall capacity. A lender factors in all recurring payments, not just credit cards, when calculating DTI. Large loan payments can offset the positive impression created by a good credit score.

Misunderstanding minimum payments

Another common misunderstanding is treating minimum payments as insignificant because they are small compared with the total balance. For DTI, what matters is the required payment amount, not how much the borrower chooses to pay above that.

High card balances translate into higher minimum due amounts, which raise DTI even if the borrower usually pays more than the minimum. Keeping balances modest relative to limits can help keep those minimums lower.

Why does debt-to-income ratio affect credit card approval?

Yes. While DTI does not appear on a credit report and is not part of a credit score calculation, many lenders use it as part of their internal decision process when evaluating whether an applicant can reasonably handle more debt. A lower DTI generally helps, and a higher DTI can lead to denials or lower limits even when credit scores are solid.

What DTI is considered “safe” for credit card approval?

There is no universal threshold, and lenders set their own comfort levels. Many consider DTIs in the lower 30s or below to be relatively comfortable for taking on additional debt, assuming other application factors are strong. Ratios in the mid-30s to mid-40s may still be acceptable, but lenders are likely to examine the application more carefully. Ratios much above that can make approval more challenging and may lead to smaller starting limits if a card is issued.

Can freelancers qualify with a higher DTI?

Freelancers and gig workers can qualify for credit cards, but lenders often place special emphasis on income stability and documentation. If income is well-documented and trending upward, some lenders may be more flexible about DTI, especially if other risk factors are low. However, a very high DTI still signals that a large share of income is already committed to debts, which can limit approval odds regardless of employment type.

Does income volatility matter, or only the average?

Income volatility does matter. Lenders want to be confident that the applicant can make required payments during slower months as well as during strong ones. Even if the average income over a year appears high, large swings from month to month can make it harder to manage debt comfortably. This is one reason lenders often average income over a period and may apply more conservative assumptions for highly variable earnings.

How applicants should think about DTI before applying

Before applying for a new credit card, it is helpful to calculate a personal DTI estimate using current monthly debt payments and gross income. This makes it easier to see how a lender might view the application from a capacity standpoint.

If DTI is already in a higher range, taking a few months to pay down balances or avoid new loans can improve the picture. Applicants should also consider whether they truly need additional credit at that moment or whether it would be wiser to focus first on reducing existing obligations.

For freelancers and gig workers, reviewing income records and organizing documentation ahead of time can make the application process smoother. Demonstrating consistent earnings and thoughtful debt management can help offset the uncertainty that comes with variable income.

Conclusion

Debt-to-income ratio is a straightforward but powerful measure that complements credit scores in credit card underwriting. It shifts the focus from past behavior alone to current capacity, helping lenders gauge how easily an applicant can absorb new monthly payments.

Understanding how DTI is calculated, what ranges lenders tend to prefer, and how DTI interacts with other factors such as credit utilization puts applicants in a better position to plan. By managing both debt levels and income thoughtfully, consumers can improve their chances of credit card approval while also maintaining greater financial flexibility and resilience over time. Understanding why debt-to-income ratio affect credit card approval allows applicants to plan debt reduction and improve approval odds before submitting a credit application.

Readers who want to explore more guides about credit cards can visit UncoverCards credit card education guides.

Disclaimer

This report is for educational purposes only and does not constitute financial, legal, or tax advice. Individual credit decisions depend on each lender’s policies and on a full review of the applicant’s circumstances. Consumers should consider consulting a qualified professional for guidance tailored to their specific situation.