Introduction

Getting your first credit card as a freelancer in the US can feel like navigating a system designed for salaried workers. Building credit as a freelancer feels like you’re playing by different rules. When you walk up to the credit card approval process, you don’t have the paycheck stubs, the W-2 form, or the steady employer that traditional workers lean on. Your income comes from clients, projects, and platforms. It’s legitimate, often abundant, but it looks different on paper—and that difference can confuse lenders who are trained to spot steady paychecks.

Here’s the truth: freelancers absolutely can get credit cards. In fact, thousands do every month. But the path requires knowing what card issuers actually look for, how to present your income in a way that makes sense to them, and what to expect along the way.

This guide walks you through the real process—no hype, no promises, just honest information about eligibility, challenges, card types, and timelines. Whether you’re new to freelancing or you’ve been doing it for years without touching credit, you’ll find the framework to move forward.

On This Page

- Introduction

- Why Freelancers Face More Credit Card Approval Challenges

- What Card Issuers Look for in First-Time Freelancers

- Can Freelancers Get a Credit Card With No Credit History?

- Best First Credit Card Options for Freelancers

- How to Improve Approval Chances as a Freelancer

- Common Mistakes Freelancers Make When Applying

- How Long It Takes to Build Credit as a Freelancer

- Frequently Asked Questions

- What to Do If You Get Rejected

- Long-Term Credit Building for Freelancers

- Conclusion

- Disclaimer

Why Freelancers Face More Credit Card Approval Challenges

The core challenge isn’t your income. It’s how your income looks to a lending algorithm.

When a card issuer reviews a traditional employee’s application, they see a salary amount, a start date, and the implied likelihood that the next paycheck will arrive on schedule. For a freelancer, the picture is messier. You might earn $3,000 in January, $6,500 in February, and $2,200 in March. You have multiple clients instead of one employer. Your income depends on project flow, client retention, and market demand. To a risk-assessment system built on predictability, that variation signals uncertainty.

This isn’t bias—it’s math. Lenders quantify risk by looking at consistency. Variable income is statistically harder to predict than fixed income. But variable income is not the same as unreliable income. The distinction matters, and understanding it is your first advantage.

The second barrier is documentation. An employee submits a paystub; you submit bank statements. An employee lists an employer; you list multiple platforms or client names. Card issuers have to verify what they’re seeing, and freelance income requires a different verification process.

The third barrier is the credit file itself. Many freelancers starting out have what’s called a “thin credit file”—very few accounts, minimal payment history, or no credit history at all. This doesn’t mean bad credit. It means they don’t have enough data points for standard credit models to evaluate. A thin file isn’t a disqualifier; it just means you’re starting from a blank slate instead of a track record.

None of these barriers are insurmountable. They’re just different from the salaried path.

What Card Issuers Look for in First-Time Freelancers

Understanding the checklist that card issuers use helps you prepare a stronger application. Here’s what they evaluate:

| Approval Factor | Why It Matters | Freelancer Impact |

|---|---|---|

| Credit history presence | Shows past ability to borrow and repay. Even a thin file is better than none. | You may have no history yet, but any existing credit (store card, loan, authorized user status) helps. Starting from zero is still approvable. For freelancers, even a thin credit file can influence approval outcomes, because credit scores play a key role in how card issuers assess risk. |

| Bank account activity | Proves income deposits and financial stability. Regular deposits signal consistent earnings. | Your bank statements become your paystub. 3–6 months of regular deposits demonstrate reliability more than a single document can. |

| Income consistency | Lenders want confidence you can make minimum payments. Consistency matters more than amount. | Monthly variations are normal. But showing deposits over several months—even if amounts differ—proves income exists. One month of data isn’t enough. |

| Identity verification | Ensures you are who you claim to be. | Straightforward for freelancers. You’ll provide SSN, address, contact info, just like salaried workers. |

| Stated income accuracy | You declare what you earn; they spot-check. Credit cards use stated income (not strict verification like mortgages do). | Report your actual typical monthly or annual freelance earnings honestly. Bank statements can back this up if questioned. |

A crucial point: credit card issuers typically use stated income for approval decisions. That means you declare your earnings, and unless something looks obviously wrong, they don’t require a 1099 form, tax return, or signed verification. This is different from mortgage or business loan applications, which demand strict documentation. Your bank statements serve as a reasonable secondary proof if needed.

Can Freelancers Get a Credit Card With No Credit History?

Yes. Here’s why it’s possible even though it feels risky from a lender’s perspective.

When you have no credit history, you fall into a category called a “thin credit file.” You haven’t yet proven you can manage debt responsibly, but you also haven’t proven you can’t. You’re unproven, not rejected. Many freelancers start with limited credit files, and exploring credit card options for people with low or no credit history can make the first approval much easier.

Card issuers have products specifically designed for this situation. They assume more risk by either limiting your credit line or requiring a security deposit. In exchange, they gain the opportunity to see how you actually behave with credit. If you pay on time, that payment activity gets reported to the credit bureaus, and you build a history. It’s a transaction: they take a small risk, you get access to credit and the chance to build your file.

The approval process typically works like this: you apply, the issuer pulls your credit report, finds a thin or nonexistent file, and then evaluates your income and identity. If income and identity check out, approval often follows—but the credit line may be modest (perhaps $300–$1,000 initially). As you use and pay the card responsibly, your limit may increase over time.

One limitation to expect: with no credit history, you won’t qualify for premium cards (travel rewards, high cash back, no annual fee). You’ll start with “starter” cards that have simpler features and may charge higher interest rates. That’s normal. Think of it as the entry point, not the destination.

Best First Credit Card Options for Freelancers

Your first card doesn’t need to be perfect. It needs to be approvable and usable. Here are the realistic categories:

| Card Type | Requirements | Typical Approval Odds | Best For |

|---|---|---|---|

| Secured Credit Card | Security deposit ($200–$1,000+), which becomes your credit limit. Must prove income and identity. | Very high (80%+) with income proof | Fastest approval when you have minimal or no credit history. Deposit is refundable once you establish payment history. |

| Entry-Level Unsecured Card | No deposit. Some credit history preferred, but not required. Stated income. | Moderate to high (60–75%) if income and identity clear | Direct credit access without deposit. Higher interest rates are common trade-off. |

| Business Card (Sole Proprietor) | No business license or formal business registration needed. Self-employed income accepted. Higher approval standards for new business owners. | Moderate (50–65%) for very new freelancers; higher if established | Separation of business and personal spending. Rewards structures often better than personal cards. May require personal guarantee. |

The reality: Secured cards have the highest approval rate for freelancers with no or thin credit because the deposit reduces the issuer’s risk. If approval is your immediate goal, starting here makes sense. Many freelancers use a secured card for 6–12 months, build payment history, and graduate to unsecured cards. The deposit is returned, and you haven’t lost money—you’ve built credit. Some cards are specifically designed for independent earners, and exploring credit cards for gig workers and freelancers can help you find options that better match variable income.

Entry-level unsecured cards exist for exactly your situation. They’re designed for people with no credit history. Interest rates are higher than premium cards, but if you pay the full balance each month (which you should), interest is irrelevant.

Business cards for sole proprietors have become more friendly to self-employed workers. Some issuers explicitly market to freelancers and gig workers. But approval standards for very new businesses are stricter than for established ones. If you’ve been freelancing for less than a year, a personal card may be easier.

How to Improve Approval Chances as a Freelancer

Preparation increases approval odds. Here’s what to do before and during the application:

1. Gather Your Documentation

Have these items ready before applying:

- Three to six months of personal bank statements showing income deposits

- Most recent tax return or 1099 forms (if you have them; not always required)

- Valid government-issued ID (driver’s license, passport)

- Social Security number

- Current address

Banks don’t always ask for all of this upfront, but having it available speeds things up if they request proof of income. Bank statements are your most powerful document—they show deposits over time and prove income without requiring official tax documents.

2. Report Your Income Accurately

When the application asks for monthly or annual income, be honest. If your freelance income averages $4,000 monthly but fluctuates, put down $4,000 (or your actual 12-month average, divided by 12). Don’t inflate it. Card issuers sometimes request verification, and lying on a credit application has legal consequences. Accuracy also builds trust when you’re in a thin-file category—the issuer will want to see that your bank statements match your stated income. Credit applications generally rely on stated income, but applicants should be prepared to support their numbers if verification is requested.

3. Maintain a Healthy Bank Balance

Banks notice your account balance. A consistent balance of several hundred to a thousand dollars signals financial stability. It doesn’t need to be huge, but zero-balance or perpetually negative accounts raise flags. Aim to keep your main operating account in decent shape.

4. Space Out Your Applications

Each credit card application generates a “hard inquiry” on your credit report. Hard inquiries temporarily lower your credit score by a few points and stay on your report for 12 months. Applying for three cards in two weeks looks like financial desperation and triggers rejection from some issuers.

Wait at least 6 months between applications for different cards. If you’re rejected, wait 6 months before trying again. This isn’t just about score recovery—it’s about lender patterns. Multiple recent applications signal risk.

5. Choose the Right Card for Your Profile

Don’t apply for a premium travel rewards card if this is your first card. You’ll be denied. Instead, target starter products explicitly designed for your situation—secured cards, entry-level unsecured cards, or cards marketed to new borrowers. As your credit history grows, your options expand.

6. Check Your Credit Report First

You’re entitled to a free annual credit report from the three major bureaus. Check it before applying. Look for errors (accounts you don’t recognize, wrong balances, identity issues). If you spot errors, dispute them in writing. Before applying, freelancers should review their credit reports for errors, missing accounts, or identity issues using the official free annual credit report service. A clean report improves approval odds. These steps make the process of getting your first credit card as a freelancer smoother and more predictable over time.

Common Mistakes Freelancers Make When Applying

Applying for premium cards too early. New credit builders often apply for high-status cards and get rejected. This rejection doesn’t improve your odds—it just uses up your quota of applications. Start low, build history, move up.

Overstating income. Lying on an application is fraud. It also backfires: if the issuer checks, you’re rejected and flagged. Honesty is better strategy than exaggeration.

Applying too frequently. Multiple applications in a short window trigger automated rejection. Space them out.

Ignoring bank statements. If the issuer requests income proof and you don’t have a 1099 or recent tax return, bank statements often suffice. Have them ready.

Closing old accounts. Once you’ve built credit and upgraded to better cards, you might want to close an old secured card. Resist the urge. Keeping old accounts open lengthens your credit history and improves your profile. Just stop using the card if you want.

How Long It Takes to Build Credit as a Freelancer

Credit building isn’t instant, but it follows predictable stages. Here’s the realistic timeline:

| Time Period | Credit Progress | What Happens | Next Card Opportunities |

|---|---|---|---|

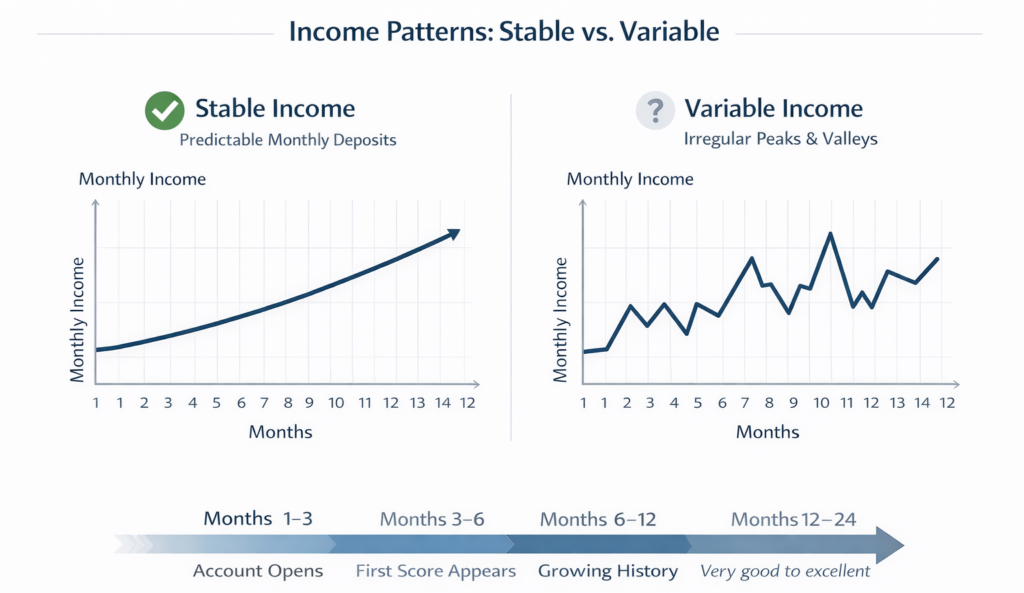

| Months 1–3 | Account opens; first deposits reported | The card issuer starts reporting your account to credit bureaus. No score yet. | Wait. You’re building the foundation. |

| Months 3–6 | First credit score may appear | After 3–6 months of activity, a credit bureau may generate your first score (FICO requires 6 months typically; VantageScore may appear sooner at 1 month). Score is likely fair, not good yet. | Some lenders accept 3–month history. Most want 6. |

| Months 6–12 | Fair-to-good credit range | With consistent on-time payments, your score moves toward the 600–700 range. Your account has a meaningful history now. | Many issuers approve for second card. Entry-level unsecured cards become realistic. |

| Months 12–24 | Good-to-very-good credit | If you’ve paid on time for 12+ months with low card balances, your score likely enters the 700+ range. Lenders see established responsibility. | Premium cards (travel rewards, higher cash back, no annual fee) become realistic. |

| 2+ Years | Excellent credit potential | Multiple years of perfect payment history builds strong profiles. Older account age works in your favor. Score can reach 750+. | Best-in-class cards, excellent loan terms, higher credit lines become available. |

Important note: You won’t have a numerical credit score until you’ve had credit activity for several months. This is normal. Don’t stress about missing a score number—focus on making on-time payments. The number will come. Building credit takes time because payment history and account age are gradually reported and evaluated by scoring models used across the lending industry. Approval speed also varies widely, and understanding how long credit card approval takes can help freelancers set realistic expectations when applying.

The most critical period is months 1–12. This is where you prove to lenders that freelance income, despite its variability, is reliable enough to support credit responsibility. One year of perfect payments is the threshold where most issuers stop thinking of you as “high-risk” and start treating you like a normal applicant. This is the exact situation many people face when getting your first credit card as a freelancer with no prior borrowing history.

Frequently Asked Questions

Can freelancers get a credit card without any credit history?

Yes. Secured cards are designed for this. You put down a deposit, use the card responsibly, and after 6–12 months of perfect payments, you can graduate to unsecured cards. Some entry-level unsecured cards also accept no-credit applicants, though approval is easier with a deposit.

What income should freelancers report on the application?

Report your actual typical monthly earnings or 12-month average divided by 12. If you earned $50,000 total last year, report roughly $4,167 monthly. Honesty is both ethical and practical—banks often cross-check stated income against bank statements or tax documents.

Are secured cards worth it?

Yes. The security deposit feels like losing money, but it isn’t. It’s collateral held in a separate account. Once you prove responsible use (typically 6–12 months of on-time payments), the issuer refunds the deposit and may upgrade you to an unsecured card. The cost is effectively zero if you make payments on time. You get credit-building access without requiring a credit file.

Does gig work income count toward the income requirement?

Yes. Income from platforms (rideshare, food delivery, freelance marketplaces, etc.) counts. You may need to show bank statements or platform payment histories to prove it, but issuers accept gig work as legitimate income.

How long should I wait before reapplying if I get rejected?

Wait 6 months. The hard inquiry will fade from your report, your credit score will recover, and you’ll have time to build a thicker file. Use that 6 months to build payment history on another account (secured card, becoming an authorized user, credit-builder loan) so your next application looks stronger.

What to Do If You Get Rejected

Rejection stings, but it’s not final. Here’s how to move forward:

First, request the issuer’s written reason for denial. Federal law requires them to provide this within 30 days. Common reasons for freelancers include “limited credit history” or “insufficient income documentation.” Understanding the specific reason tells you how to improve.

If the reason is limited credit history, a secured card is your next step. You bypass the credit file issue and start building immediately. Six months later, with payment history in place, reapply for the card you wanted.

If the reason is insufficient income documentation, gather better documents next time. Provide recent bank statements (3–6 months), tax returns if you have them, and client contracts or invoices showing ongoing work.

If the reason is “too many recent inquiries,” simply wait. Each inquiry’s impact fades after 12 months, and combined impact is minimal after 6 months. Using this time to build other forms of credit (authorized user status, credit-builder loan) makes your next application stronger.

Consider alternative credit-building tools while you wait to reapply:

- Secured credit card: A different issuer might offer better terms.

- Authorized user status: Ask a family member or trusted friend with good credit to add you to their card. Their positive payment history helps your file immediately.

- Credit-builder loan: Some credit unions and online lenders offer small loans ($500–$1,500) specifically designed to build credit. You make payments for 6–12 months, and the lender reports to credit bureaus.

Rejection is not failure. It’s feedback. Use it.

Long-Term Credit Building for Freelancers

Getting your first credit card is the starting point, not the finish line. Your real goal is building credit that opens doors—for better interest rates, higher credit limits, easier approval for loans, and financial flexibility.

The path looks like this:

Months 1–6: Get your first card (secured or entry-level unsecured). Use it for regular, small expenses. Pay the full balance every month, on time. Don’t carry a balance. This builds your payment history and keeps your credit utilization (the percentage of available credit you’re using) low. Both factors help your score.

Months 6–12: Check your credit score once it appears. If your score is improving, consider applying for a second card—possibly an unsecured card, or an upgrade of your secured card to unsecured. If your first card was secured, the issuer may offer automatic graduation to unsecured. Continue paying on time and in full.

Year 1+: By 12 months of perfect payments, most lenders see you as established. Your credit file is no longer thin. You can pursue premium cards with better rewards, lower interest rates, or special features. You also become eligible for personal loans, higher credit limits, and better terms on other credit products.

Years 2–3: As your accounts age and your payment history deepens, your credit score reaches “very good” or “excellent” levels (typically 750+). At this point, you have access to the best products the market offers. Freelance status is no longer a barrier.

Conclusion

Getting your first credit card as a freelancer is possible. It’s not as automatic as it is for salaried workers, but the barriers are surmountable, and the timeline is reasonable. You don’t need perfect documentation or a flawless financial history. You need consistent income, honest reporting, and a willingness to prove yourself over several months.

Start with a product designed for your situation—a secured card if credit-building is urgent, or an entry-level unsecured card if you have some history. Use it responsibly, pay on time, and watch your credit file grow from thin to established to strong.

Getting your first credit card as a freelancer is a process of building trust over time, not a one‑time approval test. The first card is not a test. It’s a tool. Approach it with calm planning rather than urgency or anxiety. Many thousands of freelancers before you have successfully moved from “no credit” to “good credit” to “excellent credit.” You can too. For more practical guides on building credit, approval timelines, and freelancer‑friendly card options, explore the latest resources on UncoverCards.

Disclaimer

This article is for educational purposes only and should not be considered financial, legal, or investment advice. Credit card approval criteria vary significantly by issuer, applicant profile, current economic conditions, and individual circumstances. The timelines and processes described here are typical but not guaranteed. If you are considering applying for a credit card, review the specific issuer’s eligibility requirements and consult with a financial advisor if you have questions about your individual situation. This content does not constitute a recommendation to apply for any particular credit product.