Introduction

The gig economy has reshaped how millions of Americans earn their living. Whether you’re driving for a rideshare platform, making deliveries, freelancing online, or piecing together multiple part-time gigs, your income likely looks very different from the steady paycheck of a traditional employee. One month you might earn $4,500; the next, just $2,000. This unpredictability creates a legitimate question: how inconsistent gig earnings affect credit card approval.

The short answer is that inconsistent income doesn’t automatically disqualify you from getting a credit card. But it does complicate the process. Credit card issuers want to understand whether you can reliably make your monthly minimum payments. When your income bounces around month-to-month, lenders perceive higher risk—not because gig work is inherently unstable, but because their approval algorithms and underwriting guidelines were built primarily with W-2 employees in mind.

Understanding how the approval process actually works gives you a real advantage. You’ll know what documentation matters most, why certain factors weigh heavily, and how to present your financial picture in the clearest possible light.

On This Page

- Introduction

- What Is Considered Inconsistent Gig Income?

- How Credit Card Issuers Evaluate Gig Worker Income

- Why Income Stability Matters More Than Total Earnings

- How Inconsistent Gig Earnings Affect Credit Card Approval in Practice

- Does Inconsistent Gig Income Automatically Mean Rejection?

- Factors That Help Gig Workers Get Approved Despite Irregular Income

- Gig Workers vs Freelancers: Income Stability Comparison

- Credit Card Limits and Irregular Gig Income

- How Freelancers and Gig Workers Differ in Credit Card Approval

- Frequently Asked Questions

- Conclusion

- See the Complete Approval Guide

What Is Considered Inconsistent Gig Income?

Inconsistent gig income isn’t a fixed definition used in banking regulations. Rather, it describes the natural reality of gig work earnings. Here’s what it typically includes:

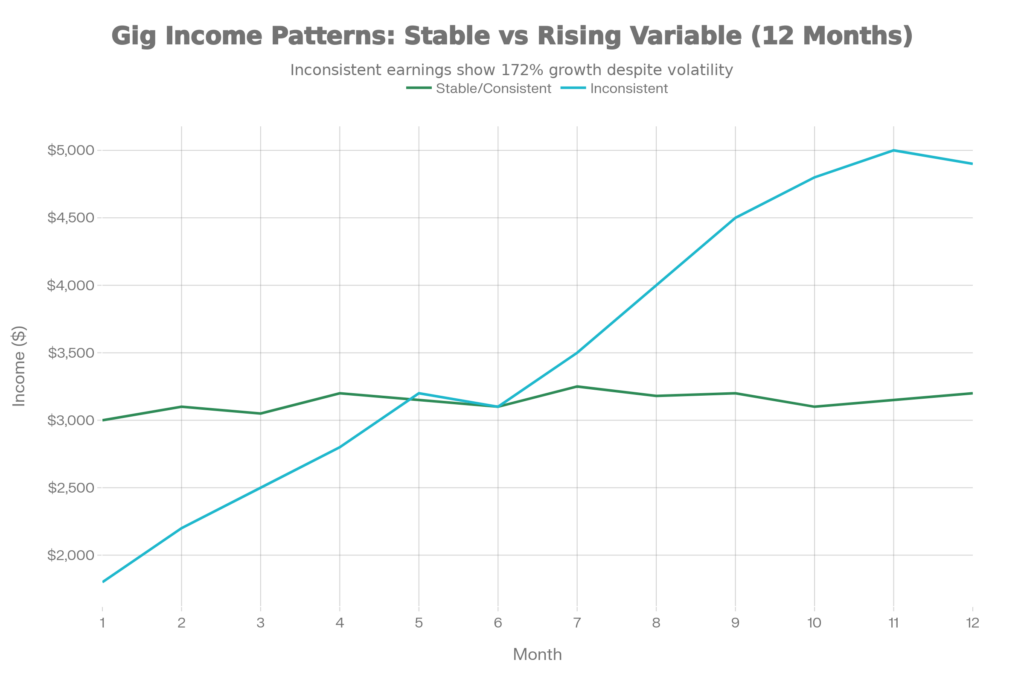

Comparison of stable monthly income versus inconsistent gig earnings over a 12‑month period, showing why lenders focus on income trends rather than single high‑earning months.

Monthly income fluctuations.

A rideshare driver might earn $3,500 in a busy month but only $2,200 during a slow period. A freelancer might land a large project in June ($5,000) but struggle to find work in July ($1,200). These swings are normal in gig work but unusual in traditional employment.

App-based earnings.

Platforms like Uber, Lyft, DoorDash, Instacart, and TaskRabbit don’t guarantee minimum weekly or monthly earnings. Compensation depends on hours worked, demand, tips, and promotions. Many gig workers also report different income from multiple platforms simultaneously, making a single consistent income stream unlikely.

Tips, bonuses, and incentives.

Unlike a salaried employee whose gross pay is predictable, gig workers depend on tips and platform bonuses that vary significantly. A delivery driver’s earnings might increase 30% during peak hours or weather events, then return to baseline.

Lack of a fixed pay schedule.

Salaried employees know their paycheck arrives on the 15th and last day of the month. Gig workers often receive payment on different schedules: weekly ACH transfers, biweekly payouts, or only when they reach a minimum threshold. This fragmented payment structure makes income timing unpredictable too.

Income gaps.

Many gig workers take time off between jobs, during illness, or when they need a break. These gaps create months with zero or minimal earnings—a pattern that concerns lenders evaluating long-term earning capacity.

How Credit Card Issuers Evaluate Gig Worker Income

Credit card issuers operate under a federal requirement called the “ability to repay” standard, mandated by the 2009 Credit CARD Act. This law requires issuers to assess whether you can afford to make the required minimum periodic payments on a new credit card. Gig earnings are treated as self‑employment income according to the IRS, which is why income patterns matter more than fixed paychecks for gig workers.

Credit card issuers are required to follow the ability to repay requirement when evaluating applications, including those from gig workers with irregular income.

But what does “ability to repay” actually mean in practice? It’s not a single test. Issuers use a combination of strategies:

Stated income reliance.

Most credit card applications simply ask you to state your annual or monthly income. In the majority of cases, card issuers don’t verify this information during the initial application process. They rely on your self-reported number. This is where gig workers have an advantage: you can include all legitimate income sources on the application—ride-share earnings, delivery income, freelance fees, or any other income you have a reasonable expectation of receiving.

Income trend analysis.

Rather than focusing on a single high-earning month, issuers analyze your income pattern over 6 to 12 months. They’re asking: Is your income growing, stable, or declining? A gig worker whose earnings consistently average $3,200 per month—even with fluctuations between $2,500 and $4,000—presents less risk than someone whose income is trending downward or shows unexplained gaps.

Debt-to-income ratio calculation.

Lenders examine what portion of your monthly income goes toward existing debt obligations: credit cards, car loans, student loans, mortgage, etc. The CARD Act requires issuers to consider this ratio as part of their ability-to-repay assessment. Mathematically, if you earn $4,000 per month and have $1,500 in existing monthly debt payments, your debt-to-income ratio is 37.5%—reasonable for most issuers, who prefer to see ratios under 40-50%.

Why Income Stability Matters More Than Total Earnings

Here’s a counterintuitive fact: a gig worker earning a steady $3,000 per month faces a better chance of credit card approval than a gig worker earning $5,000 one month and $1,500 the next, even if the latter’s average is higher.

This matters because of how credit risk is modeled. A lender’s primary concern isn’t your income ceiling; it’s your income floor. They need confidence that even in a slower month, you’ll still be able to make at least the minimum payment. If your lowest month in the past year was $1,500, that’s the figure they mentally anchor to when calculating whether you can comfortably afford a new monthly obligation.

Seasonal patterns are acceptable. Many gig-based businesses have built-in seasonality. Holiday delivery drivers earn substantially more in November-December but little in June-August. Tutors see income spikes when school starts and summer break approaches. Wedding photographers have peak seasons. Issuers understand these patterns and factor them in; what matters is that you can document the pattern clearly (usually through consistent behavior over 2+ years) and that your year-round average supports your claimed income.

Upward trends are favorable. If your income has been growing over the past year—starting at $2,500 monthly and trending toward $3,500—that’s actually a positive signal. It suggests you’re building your gig business, attracting more clients, or improving your platform standing. Issuers view this more favorably than flat or declining trends.

Downward trends raise red flags. Conversely, income that’s declining month-over-month signals trouble. Even if you started strong at $4,000 per month and averaged $3,200 over the year, if the trend is visibly pointing downward, issuers interpret this as a worsening ability to repay. They worry that by next year, you won’t be earning enough to make payments.

How Inconsistent Gig Earnings Affect Credit Card Approval in Practice

Understanding theory is helpful, but what actually happens when you apply?

Approval delays are common. A salaried employee with a regular paycheck might be approved within minutes or hours. A gig worker might experience a 1-2 week approval window while the issuer’s underwriting team reviews documentation. Some issuers require bank statements or tax returns upfront; others request them only after a preliminary approval. This isn’t rejection—it’s additional scrutiny.

Credit limits start lower. Issuers use income to calculate your initial credit limit, typically offering 2 to 3 times your monthly income. A salaried employee earning $4,000 monthly might receive a $10,000 credit limit. A gig worker with the same stated income might receive $6,000 initially, then $8,000 after 6-12 months of good payment history. This isn’t punitive; it’s risk management while the issuer gathers data about your actual spending and payment behavior.

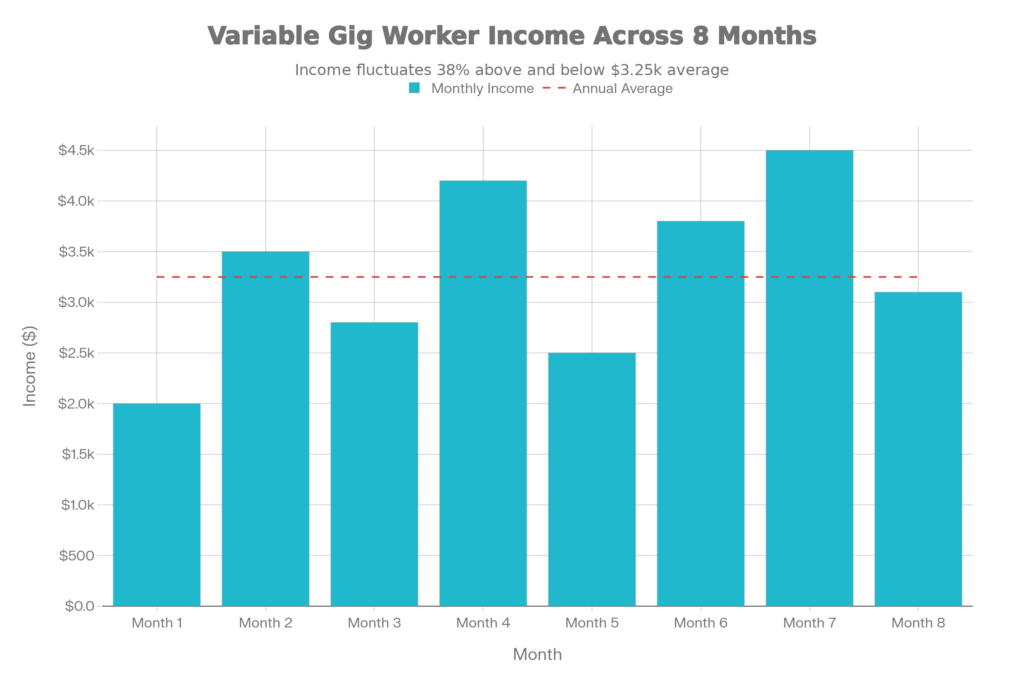

Monthly gig income fluctuating above and below the annual average, illustrating why lenders prefer predictable earnings when setting credit limits.

Underwriting scrutiny increases. Gig income doesn’t have the same documentation as W-2 employment. When an issuer requests verification, they’re not doubting you—they’re confirming that the stated income is reasonable and supported by actual deposits. Some issuers are more likely to request financial reviews or income verification later in the relationship, especially if your spending patterns seem inconsistent with your stated income.

Employment status matters in the conversation. When asked about employment status on an application, you’ll typically see options like “Salaried,” “Self-Employed,” or “Freelancer.” Selecting “Self-Employed” or “Freelancer” may trigger additional questions compared to “Salaried,” but it doesn’t result in automatic rejection. It simply flags your application for the issuer’s self-employment team, which may have different approval criteria.

Does Inconsistent Gig Income Automatically Mean Rejection?

No. This is crucial: irregular income is not a disqualifying factor by itself.

The federal rule requiring “ability to repay” doesn’t demand perfect income consistency or a minimum income level. It requires only that the issuer evaluate whether you can make the minimum payment. If you earn $2,400 per month on average through gig work and your proposed credit card would have a $150 minimum monthly payment, you clearly have the ability to repay.

Approval is still possible in many scenarios.

Consider these realistic examples:

A DoorDash driver with $3,500 average monthly income, a credit score of 740, no existing debt, and 18 months of consistent delivery history will likely be approved. The income stability over time outweighs the monthly fluctuations.

A freelance web designer earning $4,200 per month on average, with a 710 credit score and demonstrated steady client relationships documented in invoices will likely be approved, though perhaps with a moderate starting credit limit.

A rideshare driver with a lower 650 credit score but very stable $2,800 monthly income and perfect payment history on an existing credit card may be approved, but at a lower limit until the issuer sees responsible use.

The common thread: approval depends on the full financial picture, not income consistency alone.

What Factors Increase Credit Card Rejection Risk for Gig Workers?

Conversely, these scenarios create genuine challenges:

A gig worker with no credit history and inconsistent income faces the toughest path; the absence of prior responsible borrowing makes issuers cautious.

Someone whose income is rapidly declining month-over-month while they’re also carrying high existing debt (debt-to-income ratio above 50-60%) presents clear risk.

An applicant with a history of late payments or defaults will struggle regardless of current income level; past behavior is a strong predictor of future behavior.

Factors That Help Gig Workers Get Approved Despite Irregular Income

If inconsistent income alone doesn’t disqualify you, what factors actually improve your approval odds?

Credit score is often the primary lever. Your credit score is a three-digit summary (typically 300-850) of your borrowing and payment history. A score above 750 is considered excellent and can overcome income inconsistency concerns. Even a gig worker with fluctuating monthly income earns approval more easily with a strong score because it demonstrates a track record of responsible debt management.

The reason is straightforward: a high credit score tells the issuer you’ve successfully managed money in the past. They’re betting you’ll continue. With inconsistent income, they’re relying heavily on that historical behavior signal.

Credit utilization matters substantially. This is the percentage of your available credit that you’re actively using. If you have two existing credit cards with a combined $6,000 limit and you’re using only $1,200, your utilization ratio is 20%—excellent. Issuers prefer to see utilization below 30% and view higher utilization (above 70%) as a warning sign. When you apply for a new card and you already demonstrate low utilization, it signals financial responsibility and reduces the perceived risk of irregular income.

Banking behavior shows financial stability. Even before formal income verification, issuers can see some of your banking behavior through their own internal systems if you hold an account with them, or through credit bureau reports. Consistent positive balances, regular deposits (even if variable in amount), and lack of overdrafts all paint a picture of stability. A gig worker with $8,000 in savings and regular deposits to a checking account—even if the deposit amounts vary—appears more stable than someone with frequent overdrafts or depleted accounts.

Length of gig income history matters. How long have you been doing this gig work? A gig worker with only 3 months of history faces more skepticism than one with 2+ years. Time is your ally; the longer you’ve been earning through a specific platform or method, the more confident issuers become that it’s a reliable income source. Financial institutions often prefer gig workers who’ve been in the same business line for at least 2 years.

Multiple income sources signal resilience. If you earn through three different platforms or have a mix of gig work plus part-time traditional employment, that diversification is attractive to lenders. It suggests that if one income source dries up, you have backup earnings. This is precisely why some gig workers strategically mention all legitimate income sources on their applications—not to inflate numbers, but to demonstrate that their earning capacity isn’t dependent on a single platform or client.

Organized documentation impresses issuers. If you’re ever asked to verify income, presenting well-organized documents—multiple months of consecutive bank statements clearly showing gig deposits, tax returns with Schedule C self-employment income, or even a simple profit-and-loss statement—demonstrates that you take your finances seriously. Disorganized or incomplete documentation triggers more detailed scrutiny and delays.

To better understand the approval process, it also helps to know how credit card companies evaluate freelancer income when earnings are not salaried.

Gig Workers vs Freelancers: Income Stability Comparison

While the terms “gig worker” and “freelancer” are often used interchangeably, credit card issuers sometimes evaluate them slightly differently. A comparison clarifies how perception shapes approval:

The table below explains how credit card issuers typically view different types of non‑salaried income based on stability and predictability.

| Income Type | Stability Level | How Issuers Typically View It |

|---|---|---|

| App-based gig work (Uber, DoorDash) | Variable | Monthly earnings vary; risk depends on tenure and trend |

| Traditional freelancing (web design, writing, consulting) | Moderate | Income tied to client relationships; stability increases with long-term retainer clients |

| Contractor income (1099-MISC) | Variable to Moderate | Depends on contract duration and whether work is ongoing or project-based |

| Part-time W-2 employment + gig income | More Stable | Demonstrates diversified income; W-2 component provides baseline income |

| Portfolio-based income (photography, coaching, etc.) | Variable | Highly dependent on how actively the person pursues work; passive income is viewed as less reliable |

The key difference: freelancers often have stronger client relationships and retainer agreements, which make income more predictable, while app-based gig workers are more dependent on platform availability and algorithmic distribution of work, which feels more volatile to lenders. However, both can succeed with strong credit histories and documented income trends.

Credit Card Limits and Irregular Gig Income

Your initial credit card limit is a direct function of your stated income, credit score, and existing debt. It’s important to understand that this limit doesn’t define your borrowing capacity forever.

Starting limits reflect caution. A gig worker with $3,500 average monthly income might receive an initial limit of $7,000 (about 2x monthly income) rather than the $10,000-$12,000 a salaried employee with similar income might receive. This isn’t a penalty; it’s risk management. The issuer is saying, “We’re confident you can afford this, but because we’re still learning about your income stability, we’re starting conservatively.”

Limits increase over time with good behavior. The critical factor here: after 6-12 months of on-time payments, regular card usage, and demonstrated income consistency, issuers typically increase credit limits automatically or upon request. This is where gig workers actually have an advantage. If you consistently pay on time despite variable monthly income, you’re proving the exception to the issuer’s initial cautious stance. Many gig workers report receiving unsolicited credit limit increases after a year of responsible use—sometimes without even asking.

Account activity demonstrates real income. When you use the card and pay the full balance or make consistent partial payments, you’re providing real-time proof of your earning capacity. The issuer sees that your actual spending patterns align with your stated income. This data often leads to higher limits faster than the standard annual review timeline.

How Freelancers and Gig Workers Differ in Credit Card Approval

Freelancers and gig workers often face different approval experiences even when their total income appears similar. Freelancers typically work with ongoing clients or repeat contracts, which can create a more stable income pattern over time. This consistency may reduce the level of income verification required during a credit card review.

Gig workers, however, usually earn through task‑based or short‑term work that can change week to week, leading lenders to focus more on recent deposits and income trends. Because of this, gig workers may need stronger credit signals to offset income variability. In both cases, credit behavior plays a central role. A solid payment history, low credit utilization, and an established credit file help reassure lenders that the applicant can manage credit responsibly, regardless of how income is earned, especially when meeting freelancer credit card approval standards.

Frequently Asked Questions

Will having inconsistent gig income definitely prevent me from getting a credit card approval?

No. Inconsistent gig income alone doesn’t prevent approval. Credit card issuers evaluate your full financial profile: credit score, existing debt, payment history, and income trends. A gig worker with a strong credit score (750+), low existing debt, and a clear income history documented through bank statements is frequently approved despite monthly earnings that fluctuate. The key is demonstrating that you have the ability to repay based on your average earnings, not individual high-earning months.

What documents should I have ready when applying for a credit card as a gig worker?

The most important documents are 6-12 months of bank statements showing deposits from your gig work. If you’re asked to verify income, provide your most recent tax returns (which show your Schedule C self-employment income if you’ve filed taxes on gig earnings). Have invoices or a profit-and-loss statement ready if requested. Some issuers may ask for a letter from a client confirming regular work, but this is less common. Be prepared to explain your income sources clearly—how you earn, which platforms you use, and roughly what your average monthly earnings are.

Does how inconsistent gig earnings affect credit card approval change if I have a part-time W-2 job in addition to gig work?

Yes, absolutely. Having any W-2 income, even part-time, materially improves your approval odds. It provides a baseline income floor that issuers perceive as more stable. If you earn $1,500 monthly from a part-time job plus $2,000-3,500 from gig work, you can truthfully state your income as $3,500-4,500 monthly, with the understanding that at minimum, $1,500 of that is guaranteed. This improves how issuers evaluate your income stability and debt-to-income ratio.

If I get rejected, is there anything I can do?

Yes. First, request an “adverse action letter” from the issuer, which explains why your application was denied. Reasons might be “income not verified,” “insufficient credit history,” or “high debt-to-income ratio.” If the reason is income verification, you can call the issuer’s reconsideration line, provide additional documentation (like tax returns or bank statements), and ask them to reconsider.

Sometimes the underwriter simply made a conservative decision that a human conversation can overturn. Second, work on improving the specific factor cited—whether that’s building credit history, reducing other debt, or gathering better documentation. Third, consider applying for a secured credit card (backed by a cash deposit), which has much lower approval barriers and can help you build credit while you strengthen your profile.

Is my gig income counted differently if it’s from multiple platforms rather than a single source?

Not significantly. Issuers understand that many gig workers use multiple platforms. What matters is the total income and its pattern over time. If you earn $1,500 from Uber, $1,200 from DoorDash, and $800 from Instacart monthly, you report $3,500 total gig income. The fact that it comes from three platforms doesn’t hurt and may actually help because it demonstrates income diversification—if one platform reduces your earnings, you have backup sources.

Conclusion

Inconsistent gig earnings present a challenge in the credit card approval process, but they are far from insurmountable. Lenders have moved beyond rigid requirements for salaried income and now accept that self-employed and gig workers earn money differently—with more volatility but often with legitimate, documentable earning capacity.

What determines approval isn’t income consistency per se; it’s whether you can demonstrate that your average earnings support your ability to make monthly credit card payments. A gig worker with a strong credit score, manageable existing debt, and 6-12 months of documented income history has a genuine pathway to approval. Many gig workers carry multiple credit cards responsibly and build excellent credit profiles entirely through irregular earnings.

The critical steps are straightforward: keep organized financial records (especially bank statements), be honest about your income, understand your debt-to-income ratio, and recognize that starting credit limits may be more conservative—a situation that improves rapidly with responsible payment behavior. An initial limit of $6,000 instead of $10,000 isn’t a rejection of your financial fitness; it’s an invitation to prove yourself and build toward higher limits over the coming months.

The question of how inconsistent gig earnings affect credit card approval has a reassuring answer: less than you might fear, especially if you approach the process with clear documentation and realistic expectations. Understanding how inconsistent gig earnings affect credit card approval helps gig workers approach applications with realistic expectations instead of unnecessary fear.

See the Complete Approval Guide

Irregular income can affect approval decisions in different ways. To understand the full credit card approval process for gig workers and freelancers in the US, explore our complete guide below: