Introduction

How long does credit card approval take in the US is one of the most common questions applicants ask after submitting an online application. When you apply for a credit card online, that moment of hitting “submit” often comes with a simple question: how long will this actually take? The answer depends on far more than just filling out a form. Understanding what happens during credit card approval—and why timelines vary so dramatically—can help set realistic expectations and even improve your chances of getting approved faster.

The truth is that approval timelines have become less mysterious and more standardized over the past decade, but they’re still not as straightforward as many applicants assume. The process involves multiple stages, different decision-making systems, and specific rules that apply differently depending on who you are and what your financial profile looks like.

On This Page

- Introduction

- What Happens After You Apply for a Credit Card

- Instant Credit Card Approval: When It Happens

- Same-Day and 1–3 Day Approvals

- Manual Review: Why Approval Takes Longer

- Income Verification and Document Requests

- Approval Time for People With Low or No Credit History

- How Long Approval Takes for Freelancers and Gig Workers

- What to Do While Your Application Is Pending

- Common Myths About Credit Card Approval Time

- Frequently Asked Questions

- How long does credit card approval usually take?

- Can approval really be instant?

- Why do freelancers and gig workers wait longer?

- Does income verification delay approval?

- How long should I wait before reapplying if I’m denied?

- What if my application says “pending” or “under review”?

- Should I apply for another card while one application is pending?

- Conclusion

What Happens After You Apply for a Credit Card

The moment your application is submitted, an automated system springs into action. This isn’t a person sitting at a desk reading your form—it’s a computer algorithm designed to make rapid lending decisions using established criteria. Consumer protection guidance from the Consumer Financial Protection Bureau explains that most credit card decisions begin with automated underwriting systems that evaluate credit data within seconds.

The automated system checks several things almost instantly: your credit score, your reported income, your existing debt obligations, and whether your personal information can be verified against credit bureau records. The system is looking for patterns and red flags. It’s testing your application against the card issuer’s specific approval criteria, which differ from one issuer to another. Some cards are stricter than others. Some prioritize credit history heavily while others weight recent income more significantly.

Once the automated system has analyzed your data—usually within 60 seconds—one of three things happens. You receive an instant approval. You receive an instant denial. Or your application gets flagged for manual review, moving you into a different timeline entirely.

The vast majority of applications are decided by this automated system. Estimates suggest that roughly 70-80% of credit card applications receive decisions within the first minute of submission, with most of those being approvals for applicants who clearly meet the issuer’s criteria.

Instant Credit Card Approval: When It Happens

Many applicants searching how long does credit card approval take expect an instant decision, but approval speed depends on credit profile and verification needs.

Instant approval is real, but it’s not universal. When you get it, it means the automated system found nothing concerning in your application. Your credit score met the threshold. Your income appeared stable and sufficient. Your debt levels seemed manageable. Your personal information matched up. The algorithm gave you a green light.

Instant approval most commonly goes to applicants with these characteristics: an established credit history of at least a few years, a credit score above 680-700, visible and verifiable employment income (particularly salaried income), and minimal recent credit inquiries or credit-seeking behavior.

What “instant” actually means is that you’ll know your decision within seconds or minutes of submitting your application. Many card issuers now offer virtual card numbers that you can use immediately for online purchases, even before your physical card arrives in the mail in seven to ten business days.

The critical thing to understand: instant approval does not mean you’ve bypassed any verification. It means the verification happened automatically and passed. It also doesn’t mean the approval is conditional. Once you receive that instant approval notification, the card is yours—barring unusual circumstances like fraud detection or application errors discovered later. Applicants who meet the minimum credit score required for credit cards are far more likely to receive instant approval through automated systems.

Applicant Profile vs. Instant Approval Likelihood

| Profile | Instant Approval Rate | Timeline |

|---|---|---|

| Salaried, 720+ credit score | 60-70% | Seconds-60 seconds |

| Salaried, 650-720 credit score | 30-40% | 1-3 days |

| Freelancer, strong credit | 15-25% | 5-10 days |

| No credit history (thin file) | 5-10% | 10-30 days |

The rates shown reflect typical patterns, but individual results vary widely based on card requirements and individual circumstances.

Same-Day and 1–3 Day Approvals

If you don’t get instant approval, you might still be in good shape. Many applications that don’t qualify for automated approval still move through quickly because they require minimal additional review.

Same-day decisions usually happen when the automated system needs to make one additional verification check—often a quick income verification call or email. The issuer’s human team might need to confirm that your stated employer actually exists or that your job title matches what you reported. This verification step is faster than a full manual review because it’s targeted and specific. They’re not re-evaluating your entire application; they’re checking one specific detail that triggered a flag.

One-to-three-day approvals typically indicate slightly more complexity. Perhaps your income verification required a phone call and you weren’t immediately available. Perhaps there’s a small discrepancy between your application and your credit report that needs a quick clarification—maybe you moved recently and your address isn’t updated everywhere, or you were married or divorced and your name appears on documents differently than expected.

The key difference between these quick decisions and instant approvals is that a human has looked at your application at some point. But that human review was fast and surgical, addressing only the specific questions the automated system flagged.

Manual Review: Why Approval Takes Longer

Manual review is where timelines expand significantly. When your application is escalated to manual review, you’ve entered a different process entirely.

A human underwriter now has your application. They’re not just checking one fact; they’re reassessing your overall financial profile and whether you meet the card’s underwriting standards. Manual review typically takes five to ten business days, though federal law gives card issuers up to 30 days to make a decision.

Why do some applications get manual review? Usually because the automated system encountered something outside its normal parameters. The most common trigger is income verification. Self-employed people, freelancers, gig workers, and people with non-traditional income sources almost always get manual review. The automated system can verify a W-2 salary in seconds, but it can’t instantly evaluate whether your Etsy business revenue is stable enough or whether the income you reported from freelance consulting actually exists.

Other manual review triggers include: significant gaps in your work history, inconsistencies between your application and credit report, a credit report that hasn’t updated recently, signs of identity fraud concerns, or simply a high number of recent credit applications (which suggests you might be desperately seeking credit, a red flag for lenders). According to the Federal Trade Commission, identity verification delays are common when application data does not perfectly match credit bureau records.

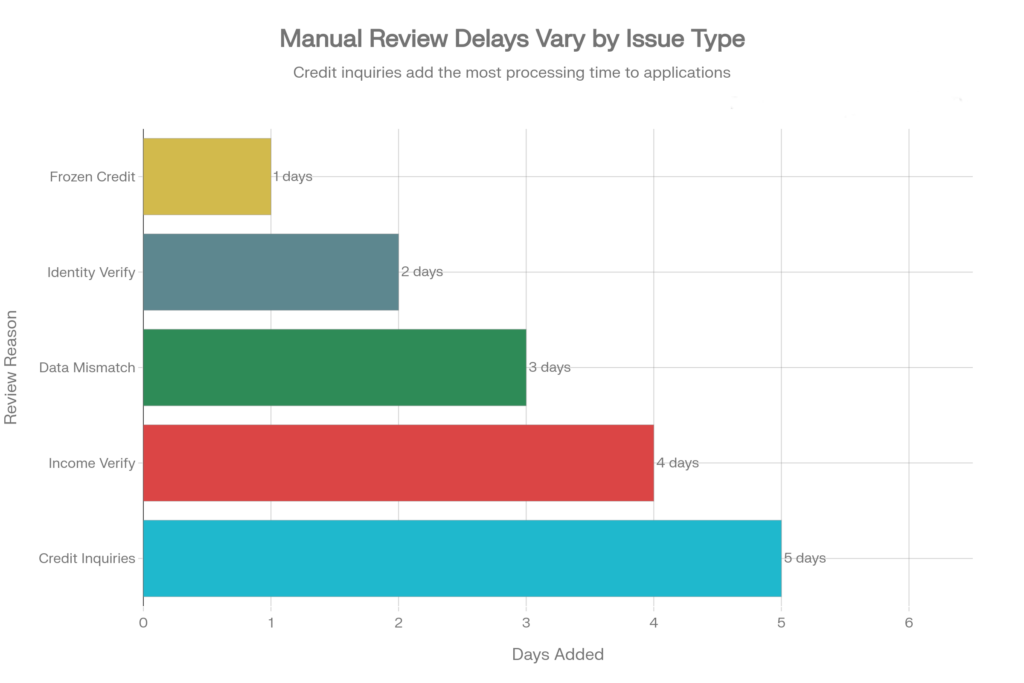

Triggers That Typically Lead to Manual Review

| Trigger | Typical Delay | Notes |

|---|---|---|

| Income verification needed | 3-7 days | Most common; requires document review |

| Identity verification | 2-5 days | Personal information mismatch |

| Employment verification | 2-4 days | Confirming job exists |

| Multiple recent credit inquiries | 5-14 days | May delay or result in denial |

| Application discrepancies | 2-3 days | Errors or outdated information |

| Frozen credit reports | 1-2 days | Requires unfreezing first |

When a human underwriter reviews your file, they have more flexibility than the algorithm. They can make exceptions. They can request additional documentation and factor it into their decision. They can look at your overall financial story rather than just your numbers.

But this flexibility comes with time. The underwriter is handling many applications, and they need time to make each decision carefully.

Income Verification and Document Requests

Income verification is the single most common reason applications move into manual review and extended timelines. Understanding how this works—especially if you’re self-employed or a gig worker—can help you prepare better.

When a card issuer needs to verify income, what they’re actually doing is confirming you have the financial capacity to repay what you borrow. For salaried workers, this is nearly instant. The system can check your reported employer against known databases, cross-reference your position and salary, and move forward. For self-employed and freelance income, the process is much more involved.

Card issuers typically want to see six to twelve months of bank statements showing regular deposits from your business or freelance work. They want to see tax returns or business records confirming the income you reported is real and recurring. They’re not just asking if you make money; they’re asking if you make money consistently enough that they can predict your future income.

A freelancer with one month of high income looks risky. A freelancer with twelve months of steady, monthly income looks stable. That’s the difference they’re assessing.

Other income sources that trigger verification: investment income, rental property income, commission-based sales jobs, or multiple income streams. For all of these, the card issuer will likely request documentation.

Common Documents Requested During Review

| Document Type | Who Usually Needs It | Processing Time |

|---|---|---|

| Pay stubs (recent) | Salaried employees | 1-2 days |

| Tax returns (prior 2 years) | Self-employed, freelancers | 3-7 days |

| Bank statements (6-12 months) | Gig workers, irregular income | 3-5 days |

| Profit/loss statements | Business owners | 3-7 days |

| Employment verification letter | Some salaried workers | 2-3 days |

| Proof of identity (updated) | All applicants (sometimes) | 1-2 days |

The timeline for these varies based on how quickly you respond. If you’re ready with documents and send them immediately, the process moves faster. If it takes you a week to gather documents, the timeline extends accordingly.

Approval Time for People With Low or No Credit History

Having little to no credit history puts you in what’s called a “thin file”—and it almost always means longer approval timelines.

When you have a thin file, lenders have less information to evaluate. Your credit score might be too new to exist yet, or it might not reflect enough activity. The automated system has fewer data points to work with, so it defaults to manual review almost every time.

This doesn’t necessarily mean you’ll be denied. Many people with thin files—including young adults, immigrants new to the US financial system, or people returning to credit after years away—do get approved. But the approval process requires more human judgment and verification.

Lenders compensate for lack of credit history by looking at alternative data. They examine your bank transaction history, looking for patterns of income and responsible spending. They might check utility payment history. Some will accept rental payment history as evidence of your ability to manage recurring obligations. Digital payment history through services like PayPal or Square is increasingly accepted as alternative evidence of creditworthiness.

Building a credit score typically takes three to six months of credit account activity. During those early months, every new credit application you make triggers a hard inquiry, which temporarily lowers your score slightly. This is why waiting between applications is important when you’re building credit. You want time for your recent application to age before you apply again. Applicants with thin files often experience longer timelines, which is common when applying for a credit card with low or no credit history.

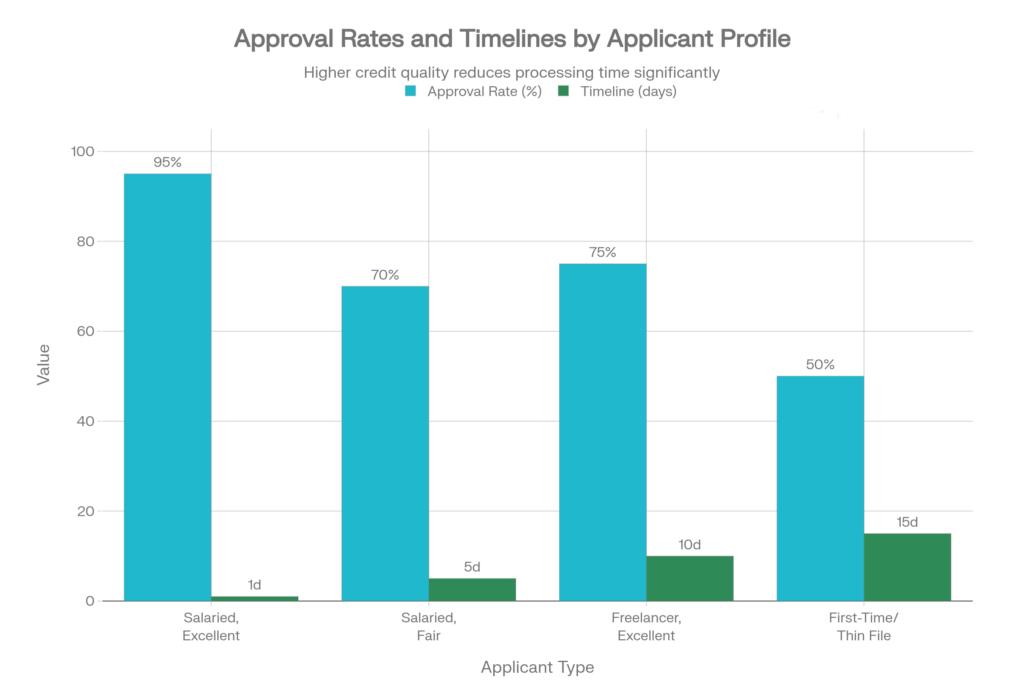

Credit Profile vs. Typical Approval Time

| Credit Situation | Typical Timeline | Approval Rate | Notes |

|---|---|---|---|

| Excellent credit (740+) | 1 day | 85-95% | Instant approval common |

| Good credit (700-740) | 2-5 days | 70-85% | Usually approved with quick verification |

| Fair credit (650-700) | 5-10 days | 50-70% | Manual review likely; income verification needed |

| Poor credit (below 650) | 10-20 days | 20-50% | May require secured card or special programs |

| Thin file/no credit | 10-30 days | 15-40% | Alternative data considered |

How Long Approval Takes for Freelancers and Gig Workers

Freelancers and gig workers operate in a different approval reality than salaried employees. While a salaried employee might receive approval within hours, a freelancer with the exact same credit score and income often faces a 5-14 day timeline.

The fundamental issue is income verification. Your income isn’t tied to a single employer with verifiable payroll records. It’s variable. It comes from multiple sources. It might peak in December and dip in June. Lenders see this variability and immediately classify your application as higher-risk, which triggers manual review.

The reality is that gig economy income can be as stable as salaried income, but lenders have no easy way to verify this automatically. They need to see your documentation. They need to verify that your stated income is real and that the pattern suggests it will continue. Many self‑employed applicants improve approval outcomes by choosing credit cards for gig workers and freelancers in the US that account for variable income.

Here’s what lenders typically want to see from gig workers:

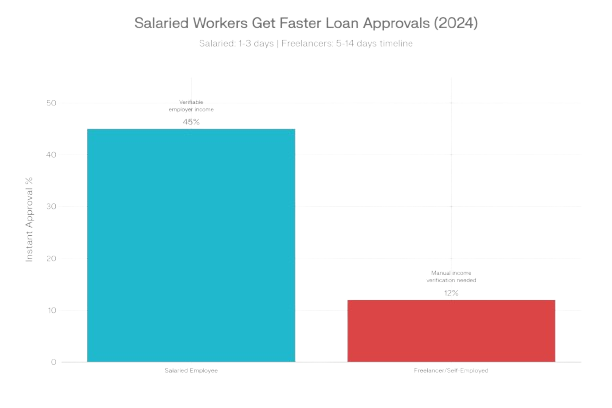

Salaried vs. Freelancer Approval Comparison

| Factor | Salaried Employee | Freelancer/Self-Employed |

|---|---|---|

| Instant approval rate | 40-50% | 10-15% |

| Typical approval time | 1-3 days | 5-14 days |

| Manual review likelihood | 30-40% | 85-90% |

| Primary verification | Employer check | Income documentation |

| Required documents | Pay stub (optional) | 6-12 months bank statements + tax returns |

If you’re a full-time freelancer, the best thing you can do is maintain thorough financial records. Keep regular deposits in a business account. File annual tax returns consistently, even if your income is low. These documents become your proof. Additionally, gig workers should apply for cards that specifically acknowledge self-employed income. Some card issuers have underwriting processes optimized for variable income, and they’ll approve you faster than traditional issuers who are still plugging your information into systems designed for W-2 employees.

Another reality: multiple years of income documentation helps more than you might expect. One year of income history might trigger a long manual review. Three years of consistent income documentation can lead to faster approval, because the pattern is undeniable.

What to Do While Your Application Is Pending

Once your application is submitted, you’re in a waiting period. The federal government gives card issuers 30 days to make a decision, but that doesn’t mean you should wait passively for that full month. For most applicants, how long does credit card approval take depends on how quickly they respond during the pending review stage.

If your application status is listed as “pending” or “under review,” here’s what you should do: First, check the issuer’s website for an application status tracker. Many card companies allow you to log in and see where your application stands. You might see a simple message like “in progress” or more specific information like “awaiting documents.” If specific information is available, that’s your roadmap.

Second, be prepared to provide information quickly if requested. Many delays happen because the issuer reaches out asking for documentation—often by email—and the applicant doesn’t see the request for days. Set up email alerts or check your email regularly when you’ve submitted an application. Similarly, if they call you, answer or call back within 24 hours.

Third, do not submit another application for the same card. Do not apply for other credit cards while your application is pending. Each new application triggers a hard inquiry on your credit report, which lowers your score slightly and signals to lenders that you’re actively seeking credit. This can turn a pending review into a denial. Wait until you have a clear answer about the first application before applying elsewhere.

Fourth, if it’s been more than a week and you haven’t heard anything, and you don’t see any updates online, you can call the card issuer’s customer service line. Ask about your application status. Be prepared to verify your identity. This call might even lead to an approval over the phone if they just needed clarification on one point.

Finally, don’t make any major financial changes during the pending period. Don’t open new accounts, close accounts, take on new debt, or apply for loans. These actions can change your credit profile mid-review and might complicate the decision. The application was evaluated based on your financial profile at submission time; stay consistent with that profile until you get a decision.

Common Myths About Credit Card Approval Time

Several persistent myths exist about credit card approval, and understanding the reality behind them can reduce unnecessary anxiety.

Myth 1: Instant Approval Means Guaranteed Approval

This is the most common misconception. Instant approval means you received a decision quickly, not that the approval is certain or unconditional. Once you’ve received an instant approval notification, the card is yours (barring fraud detection), but it does mean the issuer has moved past the approval stage. The approval is final.

However, “instant approval” is sometimes confused with “conditional approval.” Some issuers do give conditional approvals where they say yes in principle but reserve the right to change their decision if something changes dramatically with your finances. These conditional approvals are less common now, but they do exist with some premium cards.

Myth 2: Longer Wait Means Your Application Is Borderline

Many applicants believe that if their application takes five days instead of being instant, they’re barely approved. This isn’t true. Many perfectly qualified applicants face manual review simply because of employment type or the complexity of their application. Someone with a 720 credit score and self-employment income might take 10 days for manual review of that income, even though their creditworthiness is strong.

Some card issuers simply favor manual review more than others do. Certain large issuers consistently send 50% of applications to manual review, even though most get approved eventually. A longer wait reflects the card issuer’s process, not necessarily your status.

Myth 3: Higher Income Speeds Up Approval

While adequate income is necessary for approval, having higher income doesn’t necessarily speed it up. What matters is whether your income meets the card’s minimum threshold and whether you can verify it. A freelancer making $200,000 annually takes just as long to get approved as one making $80,000 annually if both need to provide the same documentation to prove it. The verification process is the same; the income amount doesn’t change that.

Myth 4: You’ll Know Instantly If You’re Denied

This isn’t always true. Denials sometimes come after several days of review, and occasionally they come after initial approval pending final verification. If a fraud check or verification step uncovers a concern, the issuer can deny you after you thought you were approved.

Myth 5: Applying Multiple Times in a Short Period Improves Your Odds

It doesn’t. Every application triggers a hard inquiry on your credit report. Multiple hard inquiries in a short period damage your credit score and signal financial desperation to lenders. If your application was denied, applying again immediately typically results in another denial. The standard guidance is to wait three to six months before reapplying, using that time to address whatever triggered the initial denial—whether that’s improving your credit score, reducing existing debt, or gathering better income documentation.

Frequently Asked Questions

How long does credit card approval usually take?

How long does credit card approval take depends on whether the decision is automated or requires manual review, with timelines ranging from minutes to several weeks. However, if your application needs manual review—which is common for self-employed and gig workers—expect five to ten business days. The federal maximum is 30 days.

Can approval really be instant?

Yes. About 30-40% of applications receive instant approval. You’ll know within 60 seconds of submitting your application whether you’re approved or if your application is going to require further review.

Why do freelancers and gig workers wait longer?

Automated systems can verify W-2 salary instantly, but they can’t verify self-employment income automatically. Your income requires human review of your business documentation, typically six to twelve months of bank statements and tax returns. This human review takes days.

Does income verification delay approval?

Almost always yes. If income verification is required, expect an additional 3-7 days on top of initial automated review. However, if you provide complete documentation immediately, the review can move faster.

How long should I wait before reapplying if I’m denied?

The standard recommendation is three to six months, with six months being safer. This gives your credit score time to recover from the hard inquiry and gives you time to address whatever caused the denial—like improving your score, reducing debt, or gathering better documentation.

What if my application says “pending” or “under review”?

This doesn’t mean denial is coming. It means the issuer needs more time to review your application. Check for online status updates, watch for requests for additional information, and be ready to provide documents quickly if asked. The issuer has up to 30 days to make a decision by federal law.

Should I apply for another card while one application is pending?

No. Each new application creates a hard inquiry that lowers your score and might turn your pending application into a denial. Wait for a clear decision on the first application before applying elsewhere.

Conclusion

Credit card approval timelines aren’t random or mysterious once you understand the process behind them. Instant approval happens when your application clearly meets the issuer’s criteria and the automated system has everything it needs. Delays happen when additional verification is required—most commonly income verification—or when your application falls outside automated parameters.

The key insight is that approval time reflects the complexity of verification required, not your value as an applicant or the likelihood of approval. A freelancer who takes fourteen days to get approved isn’t less creditworthy than a salaried employee approved in one day; they just required more documentation to prove their income was real and stable.

By understanding what triggers longer review times—particularly if you’re self-employed or have limited credit history—you can prepare better documentation in advance, respond quickly to information requests, and set realistic expectations. The process is predictable once you know what to expect. Understanding how long does credit card approval take helps applicants set realistic expectations and avoid unnecessary reapplications during the review process.

Disclaimer: This article is for educational purposes only and is not financial or legal advice. Credit card approval timelines vary by issuer, applicant profile, and individual circumstances. Requirements change frequently. For specific information about approval timelines, contact your card issuer directly or check their website. This article was written based on general practices in the credit card industry as of early 2026.