Introduction

Minimum credit profile freelancers need to qualify for credit cards is often misunderstood, especially by freelancers and independent contractors whose income does not come from a traditional salary. Your income likely varies month to month. You may not have traditional pay stubs. You file taxes rather than receiving a Form 16. These differences don’t automatically disqualify you, but they do mean credit card issuers evaluate your application through a slightly different lens. The real issue, though, isn’t what you do for work—it’s what your credit profile shows about how you handle money and repay debt.

Credit card issuers care far more about your financial behavior than your job title. They’re not really concerned whether your income comes from freelance clients, hourly wages, or a salary. What they care about is demonstrable proof that you pay your bills on time, manage existing credit responsibly, and don’t borrow beyond your means. Freelancers who earn through ongoing clients are often evaluated differently than those working on short-term projects, which is why understanding client-based income vs contract work helps clarify how lenders view stability.

That said, freelancers often start from a weaker position because they typically have thinner credit files and more complex income documentation requirements. Understanding what issuers actually need to see—and why they need to see it—puts you in a much stronger position when you apply. This article breaks down the minimum credit profile freelancers need to qualify so applicants know exactly where they stand before applying.

On This Page

- Introduction

- Minimum Credit Profile Freelancers Need to Qualify for Credit Cards

- Minimum Credit Score Freelancers Typically Need

- Credit History Length and Why It Matters

- Payment History vs. Income: What Matters More

- Credit Utilization and Existing Debt

- Thin Credit Files and New Freelancers

- Entry-Level vs. Mainstream Credit Cards

- Common Reasons Freelancers Get Denied

- Common Freelancer Credit Profile Mistakes

- How Freelancers Can Strengthen Their Credit Profile

- How Minimum Credit Requirements Differ for Gig Workers

- Frequently Asked Questions

- Conclusion

- See the Complete Credit Card Guide

- Disclaimer

Minimum Credit Profile Freelancers Need to Qualify for Credit Cards

When a credit card issuer refers to a “minimum credit profile,” they’re not talking about a single number or metric. They’re describing a complete picture of your creditworthiness. This picture includes several overlapping factors, and each one sends a signal to the issuer about how likely you are to make your payments on time. Understanding the minimum credit profile freelancers need to qualify helps explain why approval decisions often depend more on credit behavior than income level. Credit scores summarize long-term borrowing behavior and are one of the clearest ways lenders assess risk, which is why understanding how credit scores reflect overall credit profiles matters for freelancers.

Your credit score is the most visible part of that picture. It’s a three-digit number ranging from 300 to 850 that summarizes your credit history into a single, easy-to-understand rating. Credit scoring models use historical data to predict future behavior. The most commonly used scoring model is the FICO score, and most major lenders reference it when making approval decisions. But your credit score doesn’t exist in isolation. Issuers also look at what’s behind that number: the specific accounts you’ve opened, how you’ve managed them, and what the pattern looks like over time.

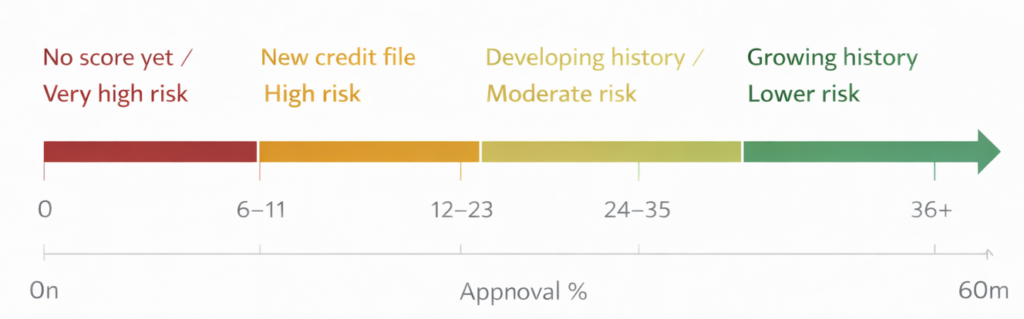

Credit history length matters because time is proof. A person with five years of on-time payments demonstrates consistency in a way that three months of perfect payments cannot. Issuers use credit history to answer a simple question: If this person has been responsible for years, will they likely keep being responsible? The longer your history, the more confidence the issuer can have in your answer.

For freelancers specifically, issuers care deeply about payment history because they view self-employment as inherently less stable than traditional employment. Without the safety net of a regular paycheck, they reason, you need an even stronger track record of meeting financial obligations. This isn’t fair or entirely accurate, but it’s a real bias in how many traditional lenders approach freelancer applications. The way to overcome this bias isn’t to argue against it—it’s to have a credit profile so clearly strong that it’s impossible to ignore.

| Credit Profile Factor | Why It Matters | Impact on Approval |

|---|---|---|

| Payment history | Shows whether you’ve paid bills on time | Most important; 35% of FICO score |

| Credit score | Summarizes overall creditworthiness | Determines approval likelihood and interest rate |

| Credit history length | Demonstrates consistency over time | Higher weight for thin-file applicants |

| Credit utilization | Shows how much available credit you’re using | 30% of FICO score; affects approval odds |

| Debt-to-income ratio | Measures total debt against total income | Determines whether you can afford new credit |

| Recent inquiries | Shows how often you’ve applied for credit recently | Multiple inquiries signal financial stress |

| Account mix | Variety of credit types you manage | Positive indicator of credit management skills |

Minimum Credit Score Freelancers Typically Need

Credit card issuers don’t all use the same approval thresholds, and the minimum score you need depends on which card you’re targeting. There is no universal cutoff, but understanding the ranges gives you a realistic sense of your options at different score levels.

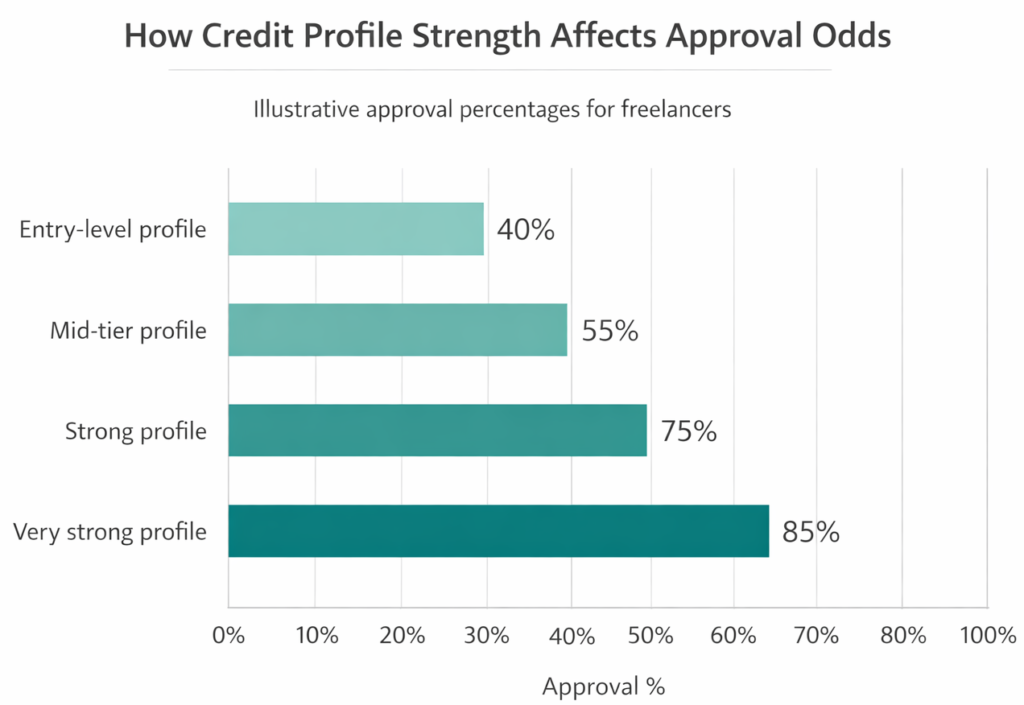

Entry-level credit cards typically accept applicants with scores in the 650 to 700 range. These cards are designed for people who are new to credit or rebuilding from past damage. They usually come with higher interest rates, lower credit limits, and minimal rewards. But they serve an important purpose: they’re the bridge that connects thin credit files to mainstream approval. While income matters, the minimum credit profile freelancers need to qualify is driven primarily by credit score, history length, and payment consistency.

Mid-tier credit cards generally require scores between 700 and 749. These cards offer better terms than entry-level options—moderate interest rates, reasonable credit limits, and basic rewards programs. This tier is where most creditworthy consumers with established credit history land.

Premium credit cards typically want scores of 750 or higher. These cards offer the best interest rates, high credit limits, excellent rewards programs, and additional benefits like airport lounge access or travel protection.

Freelancers sometimes need slightly stronger scores than their salaried counterparts for the same card tier. If a salaried employee might get approved for an entry-level card with a 650 score, a freelancer with the exact same score might face a denial. Why? Because issuers view income stability as a tiebreaker when credit profiles are marginal. Self-employment income can fluctuate, so lenders compensate by requiring a stronger credit history to offset that perceived risk.

The good news is that this isn’t a permanent barrier. Once you’ve built a couple years of solid credit history, your freelancer status becomes less of a limiting factor. Your demonstrated payment history speaks louder than your job title.

Credit History Length and Why It Matters

Credit history length accounts for 15 percent of your FICO score, but its importance extends beyond that single number. For freelancers especially, a longer credit history can be the decisive factor that tips an application from rejection to approval.

To generate a FICO credit score at all, you need at least six months of credit history. You can’t get a score before that point. The credit bureaus simply don’t have enough data about you yet. But six months is barely the starting line. Most lenders prefer to see at least two to three years of credit history before they feel confident in an approval decision.

Thin credit files refer to profiles with few active credit accounts. Different lenders define “thin” differently—some say fewer than two accounts, others say fewer than five. But the concept is the same: without multiple accounts to look at, lenders don’t have enough information to assess your creditworthiness with confidence. They don’t know whether you can manage a mortgage and a car loan together. They haven’t seen how you behave during financial stress or if an unexpected expense derails your payments. A thin file is essentially a lack of track record.

New freelancers often have naturally thin files for a simple reason: they haven’t had time to build one. Maybe you’ve been self-employed for a year and you’re still establishing your client base and income stability. You might have one credit card with decent history, but that’s not enough for most issuers to feel comfortable extending new credit. The solution isn’t to rush into multiple applications—that would backfire—but to understand that time is your ally. In six to twelve months of responsible credit management, you’ll have a noticeably stronger profile.

Experienced freelancers who have been self-employed for years might still have thin files if they’ve prioritized paying cash and avoiding credit. While that shows financial discipline, it creates an approval challenge. Issuers can’t see a payment history they don’t have. If this describes your situation, the path forward is to build credit systematically using tools like secured credit cards or credit-builder loans, not to rush approval and risk damage to your credit from hard inquiries on weak applications.

Payment History vs. Income: What Matters More

This is where many freelancers get their strategy wrong. Most assume that the key to credit card approval is proving a high income. They gather tax returns, bank statements, and invoices, ready to demonstrate that they earn well above minimum income thresholds. Then they’re shocked when an application gets rejected despite strong income numbers. While income itself does not drive approval decisions, understanding how banks verify self-employed income explains why documentation and patterns still matter during reviews.

The reason is straightforward: payment history matters more than income, and it’s not close. Payment history is 35 percent of your FICO score. Your income, by contrast, doesn’t directly factor into your score at all. Income matters to lenders for determining how much credit they’ll extend to you, but it doesn’t determine whether they approve you in the first place. Lenders consistently prioritize repayment behavior over earnings, which explains why payment history carries the most weight in credit approval decisions.

Consider two freelancers applying for the same credit card. Freelancer A earns $120,000 annually but has a history of late payments, carries maxed-out credit cards, and missed a payment six months ago. Freelancer B earns $45,000 annually but has paid every bill on time for five years, keeps credit card balances well below 30 percent, and has never missed a payment.

Freelancer B gets approved. Freelancer A gets rejected. The same outcome applies if you reverse the income numbers. Issuers will extend less credit to the lower earner—maybe a $2,000 limit instead of $5,000—but they’ll still approve them, because payment history is the foundation of creditworthiness.

A missed payment stays on your credit report for seven years, though its impact diminishes over time. Pay a bill 30 days late, and your score takes a hit. Pay one 90 days late, and the damage is significantly worse. A payment that’s 120 days or more overdue, or one that goes to collection, can reduce your score by 100+ points in a single event. This damage persists even if you’ve since built years of on-time payments.

For freelancers, the implication is clear: building a strong payment history is your highest priority. It’s more important than proving high income, more important than minimizing debt, more important than anything else you can do for your credit profile. One month of very careful, on-time payments won’t fix years of late payments, but it will start building the foundation. Twelve months of flawless payment history will noticeably improve your position. Two years is a game-changer.

| Scenario | Income | Credit History | Recent Payments | Approval Likelihood |

|---|---|---|---|---|

| High income, weak credit | $100,000+ | Thin file, late payments | Mixed | Low |

| High income, strong credit | $100,000+ | 5+ years, perfect history | All on-time | High |

| Lower income, weak credit | $40,000 | Thin file, late payments | Mixed | Very low |

| Lower income, strong credit | $40,000 | 5+ years, perfect history | All on-time | Moderate to high |

Credit Utilization and Existing Debt

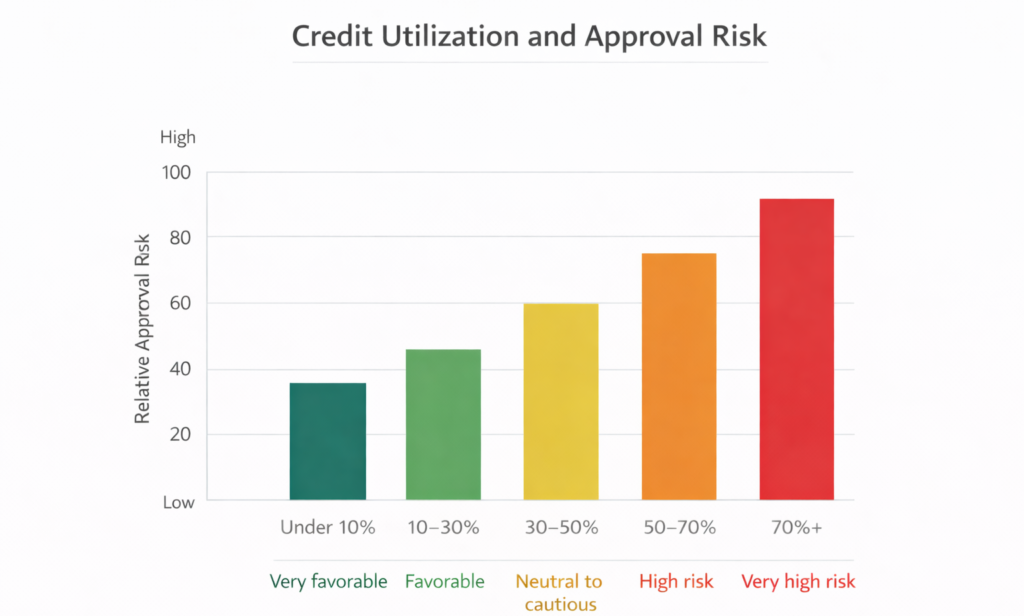

Credit utilization—the percentage of available credit you’re actually using—is one of the easiest factors to control, yet many people ignore it until their application gets rejected. High balances signal financial stress to lenders, which is why understanding how credit utilization affects approval risk is critical for freelancers.

If you have a credit card with a $5,000 limit and you’re carrying a $3,000 balance, your utilization is 60 percent. If you reduce that balance to $1,500, your utilization drops to 30 percent. Nothing else changes about your creditworthiness, but that single reduction improves your credit score and dramatically increases your approval chances for new credit.

Financial experts recommend keeping utilization below 30 percent for optimal credit health. Staying under 10 percent is ideal, but 30 percent is the widely accepted threshold that issuers use when evaluating applications. If your utilization is above 50 percent, you’re signaling to lenders that you’re overly dependent on credit and struggling to manage your debts. Utilization above 70 percent is a major red flag.

For freelancers, credit utilization can be especially critical because it demonstrates your ability to manage variable income. If you have high balances when income is tight, you’re showing lenders exactly what they worry about: a freelancer who relies on credit to cover cash flow gaps. If you keep balances low even during lean months, you’re proving that you have adequate reserves and sound financial discipline.

Before you apply for a new credit card, take a hard look at your existing balances. If your utilization is above 30 percent across all your cards, spend a month or two paying down balances before submitting applications. This costs nothing but time and significantly improves your odds. Conversely, if your utilization is already low and you haven’t applied for credit in over a year, your financial responsibility is more obvious to lenders.

Thin Credit Files and New Freelancers

A thin credit file is both a temporary condition and a real barrier to approval. If you’re a new freelancer just starting to establish credit, a thin file is almost inevitable. The question isn’t whether you have one, but what you do about it.

Most lenders consider a file “thin” if you have fewer than three to five active credit accounts. You might have one credit card, but that’s it. You don’t have a car loan, a mortgage, or any other type of credit reporting to the bureaus. From the lender’s perspective, one data point isn’t enough to make a high-confidence approval decision. They don’t know how you’d handle multiple types of credit. They haven’t seen your behavior across different economic conditions or life circumstances.

The reality is that freelancers often end up with thinner files than salaried workers, simply because they tend to be more cautious about debt. You might have delayed buying a home, avoided auto loans, or paid cash for most purchases. These are financially responsible decisions, but they come with a cost: a weak credit profile in the eyes of traditional lenders.

The path forward is systematic credit building, not rushing into multiple applications. Opening new accounts too quickly—applying for a credit card, then a car loan, then a store card, all within three months—does more harm than good. Each application triggers a hard inquiry that temporarily reduces your score, and multiple inquiries in a short timeframe signal to lenders that you’re desperate for credit, which increases their perceived risk. You’re better off applying strategically for one card, using it responsibly for several months, then applying for the next line of credit.

Entry-Level vs. Mainstream Credit Cards

Credit card issuers segment their product offerings into distinct tiers, and the approval criteria differ significantly across those tiers. Understanding this structure is crucial for a realistic application strategy.

Entry-level cards are designed for people with limited or no credit history, or those rebuilding from past credit problems. The approval standards are more lenient—lower minimum credit scores, less stringent income verification, willingness to work with thin files. But these cards come with tradeoffs. Interest rates are higher, often in the 25-30 percent range. Credit limits are lower, frequently starting at $300 to $500. Annual fees may apply. Rewards programs are minimal or nonexistent. The goal of an entry-level card isn’t to provide rich benefits; it’s to give you a chance to prove you can use credit responsibly.

Mainstream cards require a more established credit profile. Minimum credit scores are higher—typically 670+. They want to see at least two to three years of credit history. Income verification is more rigorous, especially for self-employed applicants. But if you meet these standards, the benefits are much better. Interest rates are lower, in the 15-25 percent range. Credit limits are higher. Rewards programs offer meaningful cashback, points, or miles. Annual fees may be minimal or waived for strong applicants.

Premium cards sit at the top tier. These require excellent credit scores (750+), strong income, and often an existing relationship with the card issuer. They offer the best rewards, premium benefits, and lowest interest rates—but they’re only available to applicants with proven, long-term creditworthiness.

For most freelancers starting from scratch or building credit, the optimal strategy is to begin with an entry-level card, use it responsibly for 12-18 months, then graduate to a mainstream card. This isn’t settling or compromising—it’s building a foundation. Each successful card in your history strengthens your profile for the next application. After two to three cards managed well, mainstream approvals become routine.

Common Reasons Freelancers Get Denied

Understanding why applications get rejected helps you avoid pitfalls before submitting. The reasons fall into several predictable categories.

Insufficient credit history is perhaps the most common rejection reason for new freelancers. You don’t have any credit history yet, or the history you have is too short for the card you’re applying for. The solution is to start smaller—with a secured card or entry-level card designed for new credit—and build your profile.

High balances on existing cards signal over-leverage. If you have $15,000 in credit limits and you’re using $12,000 of it, you’re showing the issuer that you’re already stretched thin. Why would they extend more credit? Before applying for new cards, pay down existing balances to get utilization under 30 percent.

Recent negative marks on your credit report are a clear rejection trigger. This includes late payments, collections, charge-offs, or bankruptcy. Depending on what happened and when, you might need to wait before reapplying. A 30-day late payment from three months ago is more damaging than one from three years ago. Time is the best healer here.

Frequent recent applications create the appearance of desperation. Multiple hard inquiries in a short period—three applications in two months, for instance—tell lenders you’re either in financial distress or don’t understand credit etiquette. Each hard inquiry stays on your report for twelve months, so a cluster of recent inquiries means future applications will face higher scrutiny.

Income too low relative to existing debt creates a high debt-to-income ratio. Lenders want to see that your gross monthly income is high enough to comfortably cover all your monthly debt payments, plus the new credit you’re requesting. For a freelancer with variable income, this can mean providing multiple years of tax returns to prove average earnings.

Unstable employment or residence history worries lenders. If you’ve changed jobs five times in three years or moved six times in two years, that signals instability. For freelancers, the solution is to establish a clear, documented history of self-employment and consistent income through tax returns and business records. Many denials stem from confusion around documentation, especially when applicants are unsure do freelancers need income documents for credit card applications.

Common Freelancer Credit Profile Mistakes

Knowing the common mistakes means you can avoid them.

Applying too early is the most common timing error. You’ve been freelancing for two months. Your income is solid. You’d benefit from a credit card. But you don’t have a credit score yet. Applying now won’t help; it will generate a hard inquiry that follows you for a year, and you’ll almost certainly get rejected. The better approach: get a secured card backed by a deposit, use it for six months, then apply for unsecured cards when you have a score to show.

Ignoring utilization until applying means you’re already behind. If you carry $8,000 in balances across $12,000 in limits—a 67 percent utilization—your score is being artificially suppressed. You should be working to lower this proactively, months before you plan to apply for new credit. Waiting until you’re ready to submit an application to tackle high balances is reactive and often too late.

Focusing exclusively on income when building your case misses the real factor that matters. You spend time gathering all your tax returns and business documentation to prove you earn $80,000 annually. But if you’ve missed two payments in the past year, that documentation won’t overcome the damage. Issuers care about demonstrated payment responsibility first and income second.

Rapid application attempts after rejections hurt your chances further. You get denied, so you immediately apply with a different card issuer, thinking maybe that one will be more lenient. Now you have two hard inquiries in the same week and you’ve signaled to all lenders that multiple institutions have already turned you down. Wait at least three months between applications, use the time to strengthen your profile, and reapply with better odds.

Not monitoring credit reports means you might be applying with incomplete or inaccurate information in your file. Errors do happen. Maybe a payment was reported as late when you actually paid on time. Maybe an old account is still listed as open when you closed it years ago. These errors can significantly damage your score. Check your credit reports before applying—you’re entitled to free reports from the major bureaus annually.

| Mistake | Why It Damages Your Application | Better Approach |

|---|---|---|

| Applying too early (before 6 months) | No credit score generated yet; hard inquiry wastes time | Build initial credit with secured card first |

| Multiple applications in short time | Hard inquiries compound, signal financial stress | Wait 3+ months between applications |

| Ignoring high utilization | Reduces score, signals over-leverage to lenders | Pay down balances to 30% before applying |

| Missing or late payments | Most damaging factor; shows irresponsibility | Prioritize on-time payments above all else |

| Not verifying income documentation | Self-employed income needs clear proof | Maintain organized records and tax returns |

How Freelancers Can Strengthen Their Credit Profile

Building a strong credit profile is a deliberate, multi-month process. You can’t rush it, but you can execute it systematically.

Start with a secured credit card if you don’t yet have a credit score. A secured card is backed by a cash deposit you provide—usually between $200 and $3,000. That deposit becomes your credit limit. The card functions like any other credit card, but the deposit protects the issuer if you don’t pay. Since the risk to the issuer is minimal, secured cards have lenient approval standards. After 12-18 months of responsible use, many issuers will convert your secured card to a regular unsecured card and return your deposit. That’s when you know your credit profile is strengthening.

Make every payment on time, every month—not just credit card payments, but all bills. Your utilities, phone bill, loan payments, everything. Payment history is 35 percent of your score. One missed payment can undo months of responsible behavior. Use automatic payments if it helps you stay consistent. Set phone reminders. Do whatever it takes to make this non-negotiable.

Keep credit card balances well below your limits. Aim for 10 percent if possible, but don’t exceed 30 percent. If you have a $2,000 limit, keep your balance under $600. This requires discipline but pays enormous dividends in credit score improvement.

Build a track record of income stability for freelancer-specific approval odds. If you’re just starting out, know that you’ll likely need 2-3 years of tax returns before major issuers feel confident in your self-employment income. Don’t try to rush this. File your taxes on time. Keep detailed records. The documentation you’re building now will matter in future applications.

Limit new applications to one every three months or so. Each application triggers a hard inquiry. Too many inquiries signal to lenders that you’re seeking credit aggressively, which increases their perceived risk.

Monitor your credit reports at least annually. You can get free reports from the major bureaus (Experian, TransUnion, Equifax) at annualcreditreport.com. Look for errors. If you find something incorrect, dispute it. Errors can seriously hurt your score and your approval odds.

Keep old accounts open, even if you don’t use them. The age of your oldest account matters. If you have a credit card you opened five years ago but no longer use, don’t close it. That account is building your credit age and increasing your available credit, both of which help your score.

How Minimum Credit Requirements Differ for Gig Workers

Minimum credit requirements can feel slightly higher for gig workers compared to traditional freelancers, largely because income patterns are more irregular. While lenders use the same credit scoring models for all applicants, they often look more closely at credit history depth, utilization levels, and recent payment behavior when reviewing gig worker applications.

A shorter or thin credit file may raise concerns if income fluctuates significantly from month to month. In these cases, lenders prefer to see consistently low credit card balances, no recent late payments, and a longer track record of responsible credit use. Even when income is sufficient, gig workers with higher utilization or limited history may be approved with lower limits or stricter terms. Understanding these differences helps applicants set realistic expectations and focus on strengthening the parts of their credit profile that matter most before applying, especially when reviewing minimum credit requirements for gig workers.

Frequently Asked Questions

What is the minimum credit profile freelancers need?

There’s no single minimum that applies to all freelancers or all cards. Entry-level cards typically want a 650+ credit score and 6 months of credit history. Mid-tier cards want 700+ and 2-3 years. Premium cards want 750+. Beyond the score, issuers look at payment history (your most important factor), credit utilization (keep it below 30%), and income documentation. For freelancers specifically, having clear tax returns showing consistent income helps offset any bias against self-employment.

Is income more important than credit score?

No. Payment history is significantly more important than income for approval decisions. Your credit score determines whether you get approved; your income determines how much credit they’ll extend to you. A high income can’t overcome a poor payment history, but a strong payment history can overcome a lower income. That said, you do need sufficient income to afford the credit being offered. If you earn $30,000 annually and you’re applying for a premium card with a $10,000 limit, the issuer will worry whether you can handle the payments.

Can freelancers get approved with a thin credit file?

Yes, but it’s more challenging than with a thick file. Secured cards are specifically designed for thin-file applicants. If you don’t yet have a credit score, apply for a secured card, use it responsibly for 6-12 months to build a score, then apply for entry-level unsecured cards. After another 12-18 months of good behavior, mainstream cards become accessible.

Does self-employment hurt approval chances?

It can, but not because self-employment is inherently risky. The issue is that your income is harder to verify and perceived as less stable than a salary. Some lenders are simply biased against self-employment. To overcome this, prepare strong documentation (tax returns, business records, bank statements showing deposits) and focus relentlessly on demonstrating responsible credit behavior. Two years of perfect payment history can overcome significant freelancer bias.

How long should freelancers wait before applying for credit?

If you have no credit history, give yourself 6 months. Open a secured card and use it responsibly. After six months, you’ll have a credit score. After 12-18 months with perfect payments, you can graduate to entry-level unsecured cards. After another 12-18 months of responsible use of unsecured cards, mainstream approvals become realistic. So from zero to mainstream approval typically takes 2-3 years of consistent, disciplined behavior.

Conclusion

The minimum credit profile freelancers need is ultimately the same as anyone else needs: a demonstrated history of paying bills on time, managing credit responsibly, and borrowing within your means. Your job title doesn’t change the fundamental criteria. What changes is that you may need slightly higher standards in other areas to offset lender bias against self-employment. The minimum credit profile freelancers need to qualify for credit cards is built over time through consistent payments, low balances, and responsible credit use.

The most important thing to understand is that credit card approval isn’t about how much money you earn. It’s about whether lenders believe you’ll repay your obligations. That belief is built through months and years of on-time payments, low balances on existing credit, and a clear, documented income history. For freelancers without an established credit profile, the path forward is to start small with a secured or entry-level card, build a track record of responsible credit use, and graduate to better products over time.

Your self-employment status is not a permanent barrier to approval. It’s simply a factor that requires slightly stronger fundamentals in other areas. Focus on those fundamentals—especially on-time payments—and the approval path opens up.

See the Complete Credit Card Guide

Your credit profile is one part of the approval process. To understand how credit cards work overall for gig workers and freelancers in the US — including income evaluation and approval logic — explore our complete guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This content is for educational purposes only and is not financial, legal, or tax advice.

Credit card approval criteria vary by issuer and individual applicant profile.

Readers should review their own financial situation or consult a qualified professional before applying for credit.