Introduction

Minimum credit score required for credit cards in the US is one of the most common questions freelancers, gig workers, and self‑employed professionals ask before applying: what credit score do I actually need? The short answer is that there’s no single universal minimum, but most card issuers expect at least a 650 to 700 credit score for general approval. That said, plenty of options exist at lower scores, and the real picture is more nuanced than a simple number.

What makes credit card approval harder for freelancers and gig workers isn’t necessarily a hidden higher minimum. Instead, it’s the way lenders evaluate your income stability and financial documentation. A salaried employee with a W-2 can verify income in seconds. A freelancer with variable monthly income looks riskier on paper, even if earning more overall. This extra scrutiny sometimes means you’ll need a slightly higher credit score or a cleaner payment history to offset income verification concerns—but it’s not a written-in-stone requirement.

This article breaks down the real minimum credit score requirements for credit cards, explains how the process differs for independent earners, and shows you what actually matters beyond the number itself.

On This Page

- Introduction

- What “Minimum Credit Score” Really Means to Card Issuers

- Credit Score Ranges and Typical Expectations

- Minimum Credit Score Ranges for Different Types of Credit Cards

- Why Freelancers and Gig Workers Often Need Slightly Higher Scores

- Credit Score vs Credit History Length

- Payment History and Its Impact on Minimum Score Requirements

- Credit Utilization and Existing Debt

- Score Alone vs Full Credit Profile Review

- Common Myths About Minimum Credit Scores

- Common Credit Score Mistakes That Raise Minimum Requirements

- How Freelancers and Gig Workers Can Meet Minimum Score Requirements

- Frequently Asked Questions

- Conclusion

- Understand the Bigger Approval Picture

- Disclaimer

What “Minimum Credit Score” Really Means to Card Issuers

When a credit card company publishes a card’s eligibility requirements, the minimum credit score listed is not a hard cutoff. It’s a risk threshold—a statistical marker that helps the issuer make faster decisions. Think of it as a starting point in their underwriting process, not the final word.

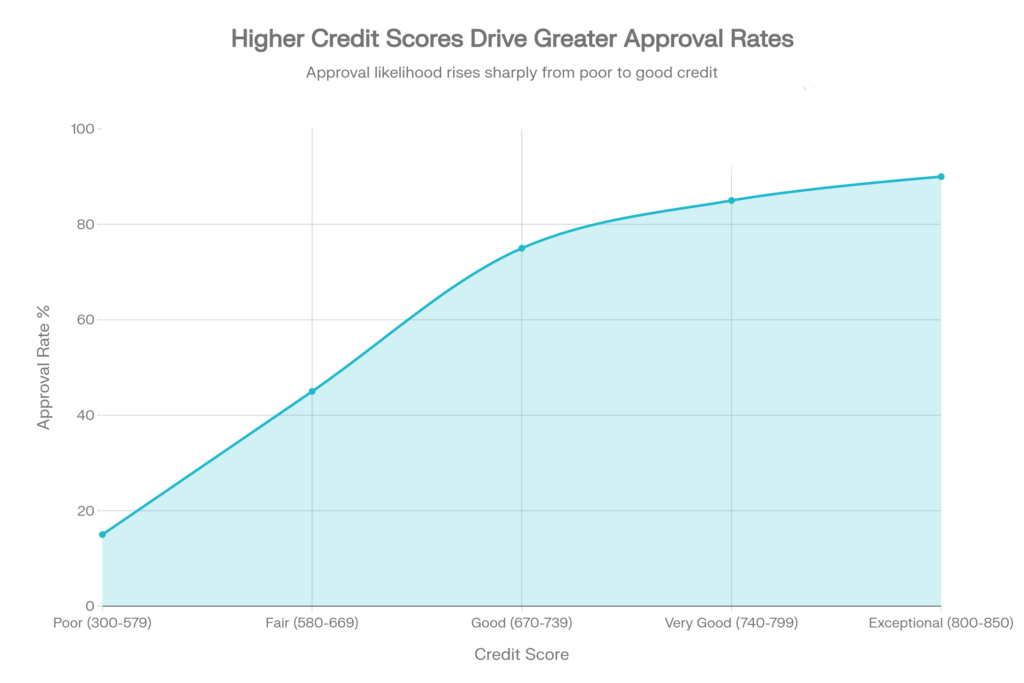

Credit Score Range vs Credit Card Approval Likelihood

Credit scores range from 300 to 850, calculated by credit bureaus using payment history, amounts owed, length of credit history, recent credit inquiries, and your credit mix. When you apply for a card, the issuer pulls your credit report and score, then weighs that score against dozens of other factors: your stated income, employment stability, outstanding debt, recent account applications, and their own proprietary risk models.

To understand why lenders rely so heavily on credit scores, it helps to know how credit scores are calculated and which factors influence approval decisions.

Here’s the key insight: there is no universal cutoff. Different issuers set different thresholds. One bank might approve 95% of applicants with a 700 score; another might approve only 60% at that same score level. Why? Because they have different risk appetites, target different customer segments, and use different underwriting algorithms.

A secured credit card, for example, may require no credit score at all—only a cash deposit. A premium rewards card might unofficially expect a score of 750+. A retail card designed for store loyalty might approve scores in the 620s. The minimum isn’t universal; it’s issuer-specific and product-specific.

Credit Score Ranges and Typical Expectations

Most mainstream credit cards operate roughly within these ranges:

| Credit Score Range | FICO Rating | Typical Approval Likelihood | Card Types Available |

|---|---|---|---|

| 300–579 | Poor | 10–20% | Secured cards only; no unsecured options |

| 580–669 | Fair | 40–50% | Secured cards; some subprime cards; retail cards |

| 670–739 | Good | 75–85% | Mainstream cards; some rewards cards; intro APR offers |

| 740–799 | Very Good | 85–90% | Most premium cards; best rates and rewards available |

| 800–850 | Exceptional | 90%+ | All cards available; best terms and benefits |

The ranges above represent realistic approval rates across the industry based on applicant data and historical outcomes. However, your actual approval depends on your full profile, not just this table.

Minimum Credit Score Ranges for Different Types of Credit Cards

Credit cards aren’t one-size-fits-all. Different card categories target different credit profiles, and each has different risk tolerance. The minimum credit score required for credit cards also depends on the type of card you apply for, since entry‑level, mainstream, and premium cards follow different risk standards.

Entry-Level and Secured Cards

If your credit score is below 620, traditional unsecured credit cards will be difficult or impossible to get. Instead, secured credit cards are designed for you. These cards require a refundable security deposit (typically $300–$2,500) that becomes your credit limit. Because the issuer holds your cash, they accept applicants with poor credit, thin credit files, or even no credit score at all.

Secured cards are not “bad” products—they’re strategic bridges. You deposit money, use the card responsibly for 6–12 months, make on-time payments, and the issuer eventually converts your account to a standard unsecured card and returns your deposit. The goal is to build credit history and demonstrate payment reliability, moving toward better options down the road.

Mainstream Cards (Fair to Good Credit)

Cards targeting the “fair to good” range (typically 620–740 FICO) make up the majority of the market. These include:

- No-annual-fee cards with introductory APR offers on purchases (commonly 6–12 months at 0%, then standard rates)

- Cash-back cards with modest rewards (often 1–2% back on purchases)

- Balance-transfer cards allowing transfers of existing debt at low or 0% introductory rates

- Student and beginner cards explicitly marketed to people building credit

Approval rates for this tier range from 50–80%, depending on your exact score, income, and credit profile. Your odds improve significantly as you move from the lower end (620s) to the higher end (730s) of the good-credit range.

Cards with premium features—high cash-back or travel rewards, annual credits, concierge services, high sign-up bonuses—typically expect scores of 740 or above. Some high-end cards unofficially expect 760 or higher. These cards also scrutinize your outstanding debt more carefully; if you’re already carrying high balances, you may be declined even with an excellent score.

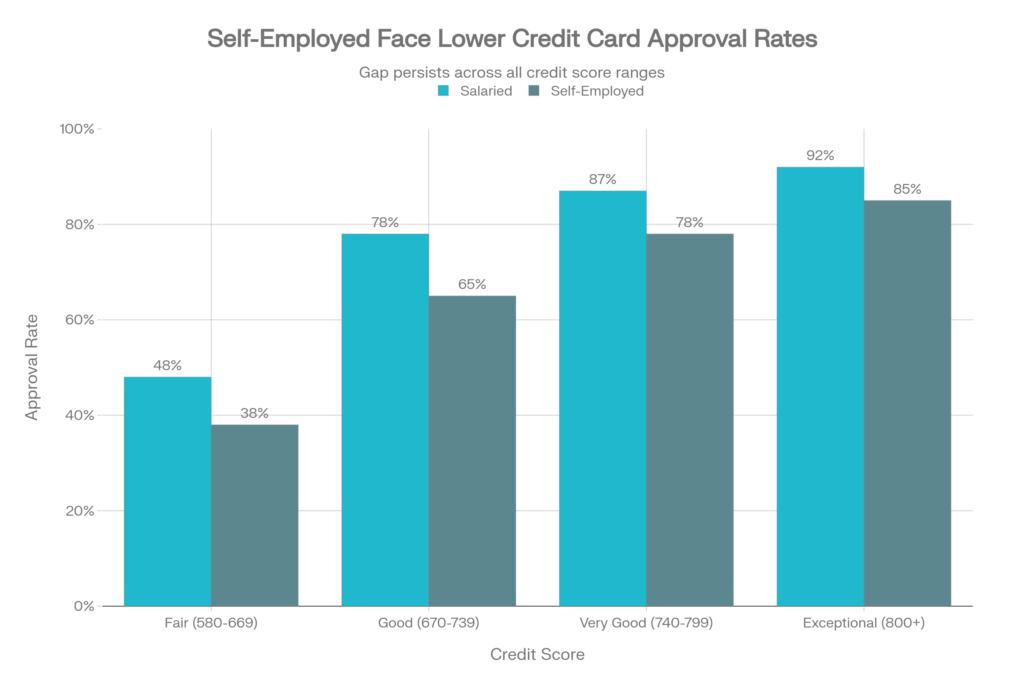

Why Freelancers and Gig Workers Often Need Slightly Higher Scores

This is where self-employment and credit card approval intersect in a real way. Freelancers and gig workers don’t face a written minimum score requirement that’s 30 points higher than everyone else’s—the credit card companies don’t publish different scales. But statistically, they do face additional scrutiny that makes approval harder at every score level.

Self-Employed vs Salaried Approval Rates by Credit Score Range

Income Variability and Documentation

A W-2 employee earning $50,000 per year can prove it with a single pay stub. A freelancer earning $100,000 per year must prove it differently—typically with two years of tax returns, bank statements, invoices, or payment verification letters.

Income variability is the core issue. A lender sees:

- Salaried employee: Paycheck arrives every two weeks like clockwork.

- Freelancer: Income fluctuates month to month, project to project.

Lenders model risk around certainty. The freelancer might earn $10,000 one month and $2,000 the next. This doesn’t mean they’re a bad risk—it means their income picture is messier to analyze. To offset that perceived uncertainty, card issuers sometimes compensate by expecting cleaner credit history or a higher credit score.

Risk Perception Differences

Studies and financial data show self-employed applicants face approval rates roughly 10–15% lower than salaried applicants at the same credit score. This isn’t discrimination; it’s statistical risk modeling. Industries using mainly independent contractors (delivery, rideshare, freelance work) have historically higher default rates than traditional employment sectors, so lenders build in extra caution.

This doesn’t mean you can’t get approved. It means at a score of 680, a salaried employee might have a 75% approval chance while a freelancer has 60%. By reaching 720, those odds might become 88% versus 75%. The gap narrows as your credit score climbs and your self-employment history lengthens. Understanding the minimum credit score required for credit cards helps applicants avoid unnecessary rejections and apply with realistic expectations.

If you want a deeper breakdown of lender behavior, this guide explains in detail how credit score affects credit card approval for freelancers and why approval thresholds feel higher for self‑employed applicants.

Documentation Requirements

For credit cards specifically, most issuers don’t require formal income documentation—they rely on your stated income during application. Credit card companies rarely verify income the way mortgage lenders do. However, some will conduct a “financial review” if you apply for multiple cards quickly or spend heavily, at which point they’ll ask for tax returns or bank statements.

If that happens and your stated income doesn’t align with your actual income history, your application can be declined or your credit limit reduced. This is why self-employed applicants benefit from keeping good records: tax returns, bank statements showing consistent deposits, and clear income tracking. Understanding the minimum credit score required for credit cards helps applicants avoid unnecessary rejections and apply with realistic expectations.

Credit Score vs Credit History Length

A high credit score with a thin or short credit history presents a different kind of risk to lenders. This matters especially for newer self-employed professionals or gig workers transitioning to independent work.

Understanding Thin Credit Files

A “thin credit file” means you have fewer than four or five accounts on your credit report. If you have only one credit card and no other borrowing history, lenders can’t build a complete picture of how you handle different types of credit. More importantly, a thin file might not generate a credit score at all until you have sufficient account history.

Gig workers with irregular income should also review these credit profile requirements for gig workers to understand how lenders assess short or limited credit histories.

FICO scores typically require at least six months of account history to generate a score. VantageScore can generate a score within one to two months. If you’re brand new to credit, you might not have a score yet, which means card issuers can’t use their standard approval models. Some will decline automatically; others have alternative approval processes.

The Age Barrier for New Applicants

If you have less than one year of credit history, expect higher rejection rates across most cards, even if your score is respectable. Lenders have historically seen higher default rates from applicants with very short credit histories, so many apply stricter approval gates.

However, this isn’t insurmountable. A strong, consistent payment history (even a short one) can often overcome the age barrier with the right card. Secured cards, student cards, and cards from issuers known for approving newer borrowers (like Capital One or Discover) are more forgiving of thin files.

| Credit History Length | Typical Approval Challenge | Workaround |

|---|---|---|

| Less than 6 months | No credit score generated yet | Apply for secured card or issuer with alternative scoring |

| 6–12 months | Higher rejection rates; approval is possible | Aim for 700+ score if generated; apply for beginner-focused cards |

| 1–3 years | Manageable; slightly higher scrutiny | Score of 670+ opens most mainstream cards |

| 3+ years | Standard approval path; no age penalty | Score of 650+ sufficient for most card types |

As your credit history lengthens, the weight of this factor diminishes. After about three years, history length stops being a major rejection trigger (assuming your payment record is clean).

Payment History and Its Impact on Minimum Score Requirements

Here’s an uncomfortable truth about credit scores: a 750 score with perfect payment history looks very different from a 750 score with recent late payments. And a 720 score with one minor slip looks riskier than a 700 score with five perfect years.

Payment history accounts for roughly 40% of your FICO score—the single largest factor. But payment history also signals future behavior. When a card issuer sees recent late payments on your credit report, they’re not just counting points on your score. They’re asking: “Is this person likely to make their payments to us?”

How Late Payments Appear and Impact Approval

Late payments don’t show up on your credit report immediately. Here’s the timeline:

- Day 1–29 after due date: You’re late, but it hasn’t hit your credit report yet.

- Day 30: If not paid, the lender reports it to the credit bureaus as a late payment.

- Day 60 and beyond: The impact worsens the longer you wait.

If you pay within 29 days of your due date, many lenders won’t report it. That’s the grace period built into the system. But once it reports at 30 days past due, it stays on your credit report for seven years, gradually losing impact but remaining visible.

For credit card applications, a single late payment from four to six months ago noticeably reduces your approval odds—even if you’ve paid on time since. A late payment from two years ago has far less impact. And a late payment from five or six years ago is barely a factor.

Building Back After Payment Problems

If you’ve had late payments or missed payments, approval isn’t impossible, but timing matters. Ideally, wait at least three to six months after bringing all accounts current before applying for new cards. Continuing to make all payments on time during that period helps your score recover and shows lenders you’ve stabilized.

| Recency of Late Payment | Impact on New Card Approval | Realistic Timeline to Better Odds |

|---|---|---|

| Within last 4 months | Very severe; rejections likely | 4–6 months of clean payments |

| 4–12 months ago | Significant impact; approval rare | 6–12 months of clean payments |

| 1–2 years ago | Moderate impact; approval possible | Continue on-time payments |

| 2+ years ago | Minimal impact; score-dependent | Standard approval path; score is primary factor |

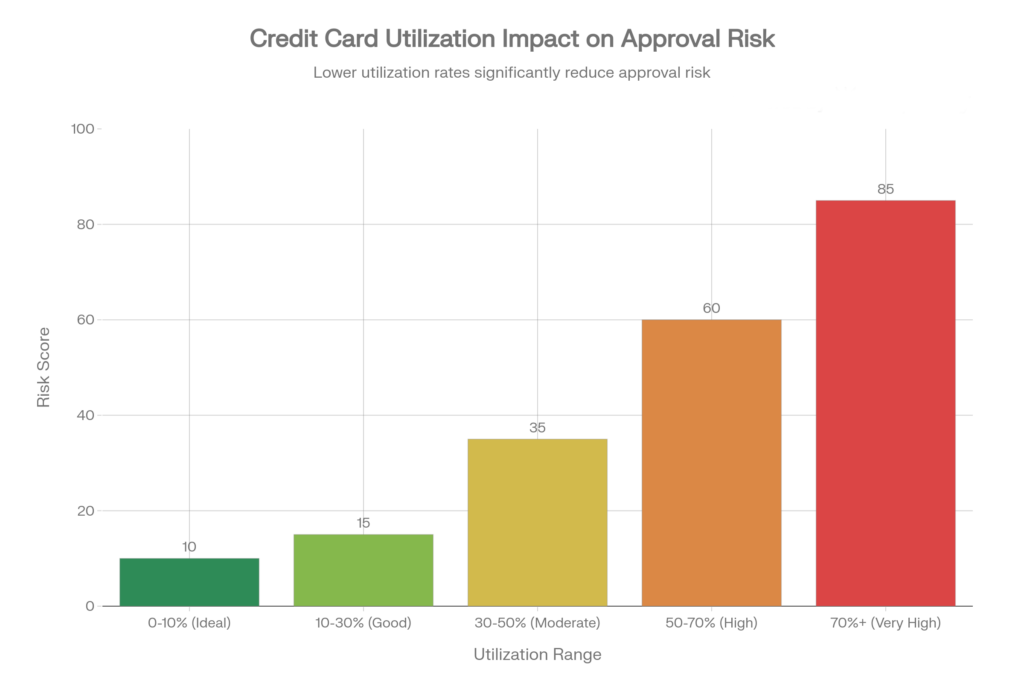

Credit Utilization and Existing Debt

Your credit utilization ratio—the percentage of your available credit limit that you’re currently using—accounts for roughly 20–30% of your FICO score. It’s also one of the fastest ways to improve (or damage) your approval odds for new cards.

Credit Utilization Ratio Impact on Approval Risk

Why Utilization Matters More for Self-Employed Applicants

For any applicant, high credit card balances relative to your limits raise a red flag. But for self-employed applicants, who are already viewed as higher-risk, utilization becomes an even bigger issue. Lenders closely monitor the credit utilization ratio because it shows how much of your available credit you are actively using.

A freelancer with a $5,000 credit limit carrying a $4,500 balance (90% utilization) sends a very different signal than a salaried employee with the same profile. The message is: “This person is running tight financially and may not have a cushion if income drops.” For a self-employed applicant with already-variable income, that looks especially risky.

The 30% Rule and Beyond

The widely accepted guidance is: keep your credit utilization below 30% of your total available credit. This is not a hard minimum from lenders, but it is a statistical sweet spot. Applicants using less than 30% of their credit have approximately 91% approval rates for new cards; those using more than 30% see approval rates drop to around 66%.

But utilization and the minimum score requirement interact. If you carry a high utilization (say 60–70%), you may need a higher credit score to offset that negative signal. Conversely, a person with a 680 score but only 5% utilization might approve where a 680 score with 50% utilization wouldn’t.

For self-employed professionals, the recommendation is stricter: aim for below 20% utilization if possible, and never exceed 30% before applying for new credit. This demonstrates financial discipline and gives you the best odds.

Score Alone vs Full Credit Profile Review

One misconception is that card issuers make binary decisions: score above 700 = approved, below 700 = declined. In reality, the process is more layered.

When Score-Based Decisions Suffice

Most credit card applications go through automated underwriting. The system pulls your credit score and checks it against the card’s minimum threshold. If you pass that check and have no major negative flags (like an active collection account or a very recent bankruptcy), you’re likely approved with a decision made in minutes. The issuer doesn’t dig deeper into your full profile—your score was enough.

This applies to the vast majority of applications. For pre-screened offers (cards you receive in the mail from issuers who’ve already vetted your credit), approval rates are even higher, sometimes 70%+, because you’ve already been pre-qualified.

When Lenders Look Deeper

In some situations, card issuers trigger a manual review or “financial review”:

- Multiple applications in a short time: If you apply for three cards in two weeks, some issuers will review your full profile to assess your debt-taking behavior.

- High income reported vs. modest credit history: If you claim $200,000 annual income but have only $10,000 in credit limits and thin file, that mismatch may trigger scrutiny.

- Significant spending spike: If you’re approved and then suddenly charge $15,000 in the first two months, the issuer might request proof of income to confirm you can support that level of debt.

In these cases, you may be asked to provide documentation: tax returns, bank statements, W-2s, or business registration documents. This is where self-employed applicants need clean records. If your bank statements show irregular deposits but your tax returns show stable income, that’s fine—lenders understand that freelance income arrives unevenly. But if your stated income doesn’t align with your actual deposits, you could face a declined application or a reduced credit limit.

| Scenario | Likely Review Type | Decision Speed |

|---|---|---|

| Standard application; score passes; no red flags | Automated only | Minutes |

| Pre-screened offer; qualified applicant | Automated with pre-qualification | Minutes to hours |

| Multiple applications in short time | Possible financial review | Hours to 1–2 business days |

| High-income claim with thin file | Possible financial review | Hours to 1–2 business days |

| Major spending spike post-approval | Post-approval review | Days to weeks |

Common Myths About Minimum Credit Scores

The world of credit and lending is full of misconceptions. Here are the most common myths about credit score minimums for card approval, and the reality:

Myth 1: Income Replaces Your Credit Score

The Reality: Income is not part of your credit score calculation at all. You could earn $150,000 per year with a 600 credit score, and you could earn $40,000 with a 780 score. Income doesn’t directly change your score.

However, income does matter in the approval decision—it’s considered separately. A lender wants to know if you can afford the credit. But they check that affordability through debt-to-income ratios and other factors, not through the credit score itself. High income helps your case, but it doesn’t override a low score. The two are independent variables in the underwriting process.

Myth 2: One Good Month of Payments Fixes Approval

The Reality: Credit scores update monthly, and you’ll see some changes quickly. Paying off a $5,000 balance could improve your score by 20–50 points within a month if that was driving your utilization sky-high. But improving your score enough to jump from “fair” to “good” territory typically takes 3–6 months of consistent, responsible behavior.

Late payments fall off the report after seven years, not seven days. Recent late payments have the most impact, but they don’t disappear quickly. Patience and consistency matter more than one-time fixes.

Myth 3: High Earnings Guarantee Approval

The Reality: A self-employed person earning $200,000 per year can be denied a credit card if their credit score is 580 or if they have recent late payments. Lenders care about income as a factor in affordability, but credit history reveals how you’ve actually managed credit in the past. Past behavior is the strongest predictor of future behavior, so credit history typically outweighs income level in the approval decision.

That said, very high income can sometimes compensate for a lower score with certain issuers or with a manual review. But it’s not a guaranteed override.

Common Credit Score Mistakes That Raise Minimum Requirements

Certain behaviors don’t just lower your current score—they raise the effective minimum that issuers will accept. Here’s what to avoid:

High Balances Relative to Your Limits

Carrying balances above 30% of your total credit limits is the fastest way to damage both your score and your approval odds. This is especially important for self-employed applicants; if you’re already at higher perceived risk, high utilization compounded that risk.

What to do: Pay down balances to below 30% before applying for new cards. If you have multiple cards, you can move debt around to balance utilization across all cards—one maxed card and one with zero balance is worse than two cards at 50% utilization each.

Rapid Applications for Multiple Cards

Each credit card application generates a “hard inquiry” on your credit report, and these inquiries stay visible for 12 months and impact your score for about three to six months. Apply for three cards within a week, and you’ve signaled to all issuers that you’re actively seeking credit—sometimes a sign of financial distress.

Some scoring models allow for “rate shopping” on mortgage and auto loans within a 2-week window (treating multiple inquiries as one), but credit card inquiries don’t get this treatment. Each one counts separately.

What to do: Space out applications by at least 3–4 months. If you need multiple cards, prioritize the ones you want most and apply strategically. Pre-screened offers (which you can safely apply for without hard inquiries) don’t have this limitation.

Letting Balances Age

An active late payment has more impact than an old one. But letting a balance sit unpaid without ever resolving it is also a signal. Collections accounts or charge-offs that you never paid off appear on your report and signal high risk.

What to do: If you have old unpaid accounts, explore a payment plan or settlement with the creditor. Paying off or settling a collections account doesn’t erase it immediately, but the account status changes, and lenders see movement toward resolution. Over time, this hurts your score less.

How Freelancers and Gig Workers Can Meet Minimum Score Requirements

If you’re self-employed and aiming to improve your approval odds, here’s a realistic action plan:

1. Build Consistent Payment History

This is priority number one. For the next 3–6 months, make every payment on every account on time. Set up autopay if you need to. Late payments, even 30-day late, are the single most damaging factor to your score and approval odds. One on-time payment helps; 12 consecutive on-time payments transform your profile.

2. Pay Down High Balances

If you’re carrying high credit card balances, start paying them down, especially on cards where you’re above 50% utilization. A big payoff in one month can boost your score by 20–100 points if you’re bringing utilization from 80% down to 20%. This is high-impact and worth prioritizing.

3. Clean Up Your Credit Report

You’re entitled to a free credit report from each of the three major bureaus once per year. Pull all three, check for errors, and dispute any inaccuracies. Old accounts that were paid off but still show as open, duplicate late payments, or accounts that aren’t yours can all drag down your score. Errors are surprisingly common and worth fixing.

4. Space Out New Credit Applications

Resist the urge to apply for multiple cards at once. Multiple hard inquiries and new accounts lower your score and signal higher risk. If you need a card, apply for one, get approved, wait 3–4 months, and then apply for the next one. This also prevents you from overextending yourself with new debt.

5. Time Your Applications Carefully

Apply for a new card when:

- Your score is at a high point (after paying down balances)

- You’ve gone 3+ months without any late payments

- You haven’t applied for other credit recently

- Your utilization is below 30%

Avoid applying when your score has just dropped due to a new account opening or a recent hard inquiry.

6. Document Your Income Properly

As a self-employed applicant, keep clean records: recent tax returns, business bank statements showing consistent deposits, invoices if you have them, and any payment verification letters from regular clients. You won’t need these for most credit card applications (they rarely verify income), but if you trigger a financial review, clean documentation gets you approved. Conversely, messy or inconsistent records can lead to delays or denials.

Once your score and profile improve, you can explore suitable credit cards for gig workers and freelancers in the US that match your income structure and approval level.

Frequently Asked Questions

What is the minimum credit score required for credit cards in the US?

The minimum credit score required for credit cards generally falls between 650 and 700 for most mainstream options, though approvals can happen above or below this range. There’s no single universal minimum. Most mainstream credit cards expect a score around 650–700, but this varies by issuer and card type. Secured cards require no minimum score. Some premium cards expect 750+. If your score is below 600, focus on secured cards first, which let you build history and eventually move to unsecured options.

Can income offset a low credit score?

Income helps with approval but doesn’t directly override credit score. High income can sometimes compensate for a lower score with a manual underwriting review, especially if you have a reasonable explanation. But a very low score (below 600) with a recent late payment won’t be overcome by high income alone. Your credit history is weighted more heavily than income in the approval decision.

Can gig workers get approved with a thin credit file?

Yes, but it’s harder. With fewer than 4–5 accounts, approval rates drop across most card types. Your best path is a secured card from a mainstream issuer or a beginner-friendly card from issuers like Discover or Capital One. Use it responsibly for 6–12 months, build your history, and move to better cards later.

Do freelancers need higher credit scores than salaried workers?

Not officially, but statistically, yes—by about 10–15 percentage points at each score level. A salaried employee with a 680 score has better approval odds than a freelancer with a 680 score. This is because lenders view variable income as higher risk. The gap narrows at higher scores and closes if you can document stable self-employment income.

How fast can credit scores realistically improve?

You can see 20–50 point improvements within a month by paying down high balances. A bigger improvement (100+ points) typically takes 3–6 months of consistent on-time payments and lower utilization. Expect noticeable change by month three, and major change by month six. Fixing errors on your report can happen faster; disputed and corrected errors may fall off within 1–2 months.

Conclusion

The minimum credit score for a credit card isn’t a single number carved in stone. It’s a risk threshold that varies by lender, card type, and your full financial profile. Most mainstream cards expect 650–700; secured cards expect no score; premium cards expect 750+. But your score is just one part of the decision.

For freelancers and gig workers, the challenge isn’t a hidden higher minimum—it’s the reality that self-employment is viewed as higher-risk income. You’ll face slightly tougher odds at every score level. Your advantage is that you can influence several factors: payment history, credit utilization, documentation, and timing. By maintaining perfect payments, keeping balances low, and applying strategically, you can offset income variability concerns and reach approval odds that rival salaried applicants.

The most important insight is this: your credit score reflects only your past credit behavior. It’s not a judgment on your income, your character, or your worthiness as a borrower. It’s a historical record. If your current score is lower than you’d like, that record is changeable. Consistent on-time payments, lower balances, and clean documentation will move the needle. It takes time, but the path is clear. For more practical guides on credit cards, approvals, and self‑employed credit strategies, visit UncoverCards.

Understand the Bigger Approval Picture

While credit score plays an important role, approval decisions also depend on income, risk level, and overall credit profile. To see how these factors apply specifically to gig workers and freelancers, read our full guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, or tax advice. Credit card approval criteria vary significantly by issuer and applicant profile. This information reflects general industry practices and historical trends, not guarantees. Individual applications are evaluated on a case-by-case basis. Consult with a financial advisor or your lender directly for decisions specific to your situation.