Introduction

Secured credit cards for freelancers can be a practical solution when traditional credit card applications get rejected. Many self‑employed workers discover that getting approved for a regular credit card is harder than expected, especially when income is irregular or difficult to document.

A rideshare driver who earns well but has no pay stubs, a graphic designer whose income spikes around big projects, or a student copywriter juggling a few small clients may all run into the same issue: lenders are unsure how stable that income really is. For many self-employed people, the problem is not how much they earn overall, but how uneven and hard-to-document the cash flow looks on paper.

Traditional credit card approval systems are built around predictable paychecks. Lenders like to see stable monthly income and an existing record of on-time payments. Freelancers and gig workers often have neither: their deposits come in at random times from different clients, and many are just starting out with thin or no credit history at all. This combination makes freelancer credit card approval more difficult, even when the person is very careful with money.

That is where secured credit cards for freelancers can become useful. A secured card requires a cash deposit up front, known as a secured credit card deposit. That deposit usually becomes the credit limit and acts as collateral for the lender. Because the lender’s risk is lower, approval requirements are often more flexible, especially for people with irregular income or limited credit. Used correctly, these cards can be a powerful tool for credit building for freelancers. If you are new to borrowing, it also helps to understand how credit cards work before choosing the right option.

On This Page

- Introduction

- Why Freelancers Get Rejected for Unsecured Credit Cards

- What Is a Secured Credit Card? (Simple Explanation)

- When Secured Cards Do NOT Make Sense

- Costs and Risks Freelancers Should Understand

- How Freelancers Should Use a Secured Card Strategically

- Secured vs Unsecured for Freelancers

- Credit Building Timeline for Freelancers

- Common Mistakes Freelancers Make

- Frequently Asked Questions

- Conclusion

- Explore the Complete Credit Card Guide

- Disclaimer

Why Freelancers Get Rejected for Unsecured Credit Cards

Before deciding whether a secured card makes sense, it helps to understand why freelancers and self‑employed people are often rejected for regular, unsecured credit cards.

Income verification challenges

For salaried workers, verifying income is simple: one or two recent pay stubs usually do the job. For freelancers, lenders often care more about average income over time—sometimes over a year or even two years—rather than what came in last month. Proving that can require tax returns, bank statements, or profit-and-loss summaries, which many new freelancers do not have ready. If the income looks inconsistent or underreported, irregular income credit card approval becomes harder.

Thin or new credit history

Many freelancers are young, recently self‑employed, or coming from a mostly cash-based lifestyle. They may have never had a credit card, car loan, or other account in their own name. Lenders call this a “thin file” or limited credit history. Even if their actual finances are solid, the lender cannot see a track record of on-time payments, so the application for a standard credit card for self-employed people may be declined.

Higher perceived risk by lenders

Lenders often view self-employed income as less predictable than a traditional job, even when the total yearly income is similar. A freelancer might earn very little in January and a lot in June. From the lender’s perspective, that makes it harder to be sure the borrower can make every monthly payment, especially during slow months. As a result, lenders may require stronger credit histories, more documentation, or higher income levels before approving an unsecured card.

Common freelancer approval mistakes

Freelancers sometimes unintentionally hurt their own chances by:

- Guessing or inflating income on applications instead of basing it on tax returns or realistic averages, which can backfire if the lender verifies it.

- Applying for multiple unsecured cards in a short period, causing several hard inquiries and signaling desperation.

- Mixing personal and business finances in confusing ways, making bank statements look messy.

- Ignoring existing debts or late payments on other accounts, which lenders weigh heavily.

Understanding these challenges explains why a different path—like a secured card—can sometimes be smarter for a first step.

What Is a Secured Credit Card? (Simple Explanation)

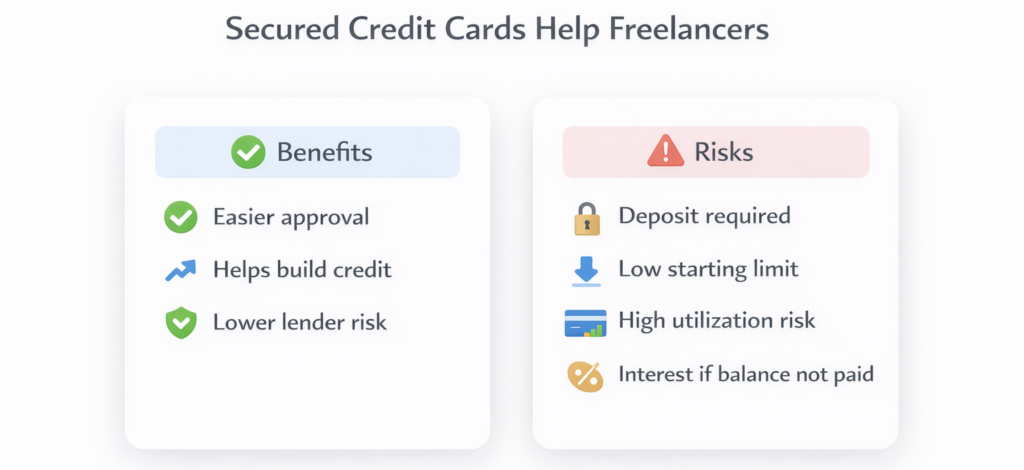

A secured credit card is a credit card backed by a cash deposit you provide when opening the account. That deposit is held by the card issuer as collateral. If you stop paying your bill, the issuer can use the deposit to cover what you owe (up to the deposit amount). Secured credit cards are often recommended for people who are building or rebuilding credit because the deposit reduces lender risk.

How the secured credit card deposit works

- When you open the card, you send a deposit—often a few hundred dollars. Many issuers have minimums in the range of about 200 dollars, and some allow deposits up to a few thousand dollars.

- The issuer holds this money in a separate account. You cannot use it to pay your monthly bill.

- As long as you make payments on time, that deposit just sits there. When you eventually close the card in good standing or “graduate” to an unsecured card with the same issuer, the deposit is usually returned.

Deposit = credit limit (in most cases)

For many secured cards, the amount you deposit becomes your credit limit.

- Deposit 300 dollars → starting credit limit around 300 dollars

- Deposit 500 dollars → starting credit limit around 500 dollars

Some issuers may offer a slightly higher limit than your deposit or allow increases over time, but the core idea is that your available credit is tied directly to money you have put down. If you want a full comparison, read our detailed guide on the difference between secured and unsecured credit cards.

Why the deposit reduces lender risk

The deposit gives the lender a safety net. With a regular, unsecured card, the lender is lending based only on trust in your future payments. With a secured card, the lender has actual cash they can keep if you default. That makes them more willing to approve people with poor, limited, or irregularly documented credit, including many freelancers.

How it compares to unsecured credit cards

- Unsecured credit cards do not require a deposit. Your limit is based on your income, credit history, and overall profile.

- Secured credit cards require a deposit up front, but they are usually easier to get if your credit is weak or nonexistent.

In everyday use—swiping, online purchases, paying a bill each month—a secured card works just like an unsecured card. The main differences are how you qualify and the need to tie up cash as a deposit.

When Secured Credit Cards Make Sense for Freelancers

Secured credit cards for freelancers are not a perfect fit for everyone, but they are often very helpful in several situations.

- New freelancers with no credit history

A recent design school graduate who just started freelancing may have no prior loans or cards. A secured card can be a first tool for building a payment track record that future lenders can see. - Freelancers recently denied for an unsecured card

A rideshare driver might apply for a regular card, get denied due to short work history and thin credit, and then be approved for a secured card with the same basic income. The deposit helps offset the lender’s fear of nonpayment. Gig economy workers can also explore our guide on first credit card options for new gig workers. - Self-employed workers rebuilding damaged credit

A freelance writer who had late payments or collections in the past may struggle to get approved for unsecured cards. A secured card gives them a way to show new, positive behavior over time. - Inconsistent monthly income cases

A wedding photographer may earn most of their income in certain seasons. The irregular pattern can spook lenders, but with a secured card the deposit lowers the risk, making approval more likely even when income swings month to month.

| Freelancer Situation | Secured Card Makes Sense? | Why |

|---|---|---|

| New graphic designer with no credit history | Yes | Builds first credit record using a manageable, deposit-backed limit |

| Rideshare driver denied for unsecured card | Yes | Deposit reassures lender after recent denial |

| Freelance writer with past late payments | Yes | Offers structured way to rebuild damaged credit |

| Seasonal photographer with uneven income | Yes | Deposit reduces lender worry about income gaps |

| Consultant with stable income and long credit history | Usually no | Likely already qualifies for unsecured options |

When Secured Cards Do NOT Make Sense

There are also clear situations where a secured card is probably not the right move for a freelancer.

- Strong, established credit history

If a self-employed consultant has several years of on-time payments and low balances on other accounts, a secured card may add little value. That person can usually qualify for a standard unsecured card without putting down a deposit. - Stable and well-documented income

A long-time independent contractor with several years of tax returns showing consistent net profit and no major credit issues likely meets typical self-employed credit approval requirements for unsecured cards. In that case, locking up savings as a deposit is unnecessary. - Already qualify for low-fee unsecured cards

If a lender pre-approves a freelancer for unsecured cards with no or low annual fees, competitive terms, and a reasonable limit, there is usually no benefit to choosing a secured option instead. - Enough savings but no real need for new credit

A freelancer might have several thousand dollars in an emergency fund and be curious about secured cards. But if they already have at least one healthy credit account, pay bills on time, and do not need more credit, tying up hundreds of dollars as a deposit may not be worth it. In that case, focusing on savings and existing accounts is often smarter.

In summary, secured cards are best viewed as a tool for getting in the door or rebuilding—not a default choice if you can already qualify for solid unsecured options.

Costs and Risks Freelancers Should Understand

Like any financial product, secured cards come with costs and trade-offs. Freelancers, in particular, should pay attention to the following.

Security deposit requirements

Most secured cards require a minimum secured credit card deposit in the low hundreds of dollars, with maximums that can reach into the low thousands depending on the issuer. This money must be set aside and is not available for everyday spending. For freelancers with uneven income, tying up that much cash can strain cash flow, especially during slow months.

Typical credit limits

Because the credit limit is usually based on the deposit, many secured cards start with low limits—sometimes just a few hundred dollars. That is enough for small recurring bills or groceries, but not ideal for large business expenses like equipment.

Annual fees and other charges

Some secured cards charge annual fees, and many have interest rates similar to or higher than unsecured cards. There may also be late fees and other standard credit card charges. A freelancer who carries a balance or pays late can quickly lose the benefits of credit building due to high costs.

High utilization risk with low limits

If a freelancer has a 300-dollar limit and regularly spends 250 dollars each month, credit reporting systems will see that as very high utilization (using most of the available credit). High utilization can hold back credit improvement, even if every payment is on time. Your credit utilization ratio reflects how much of your available credit you are using compared to your total limit, and lenders monitor it closely. This is a common issue for freelancers who put too many expenses on a small-limit card.

Interest considerations

Secured cards accrue interest just like unsecured ones if the statement balance is not paid in full by the due date. For someone whose income swings from month to month, carrying a balance during a slow period can quickly become expensive.

Key Cost and Risk Factors for Freelancers

| Cost / Risk Factor | What Freelancers Should Know |

|---|---|

| Security deposit | Ties up cash that cannot be used for rent, supplies, or emergencies |

| Low starting credit limit | Easy to max out with everyday expenses, raising utilization |

| Annual and other fees | Reduce the net benefit of the card, especially if income is tight |

| Interest on carried balances | Can grow quickly if you cannot pay in full during slow work months |

| High utilization on small limit | Using most of the limit regularly can slow down credit building |

| Closing card early | Can end credit-building progress before it shows a long-term positive pattern |

How Freelancers Should Use a Secured Card Strategically

Treating a secured card as a structured tool—not as extra spending power—is the key to making it work.

Keep utilization under about 30%

A common guideline is to keep your reported balance under roughly one‑third of your limit if possible. For example:

- If your limit is 300 dollars, aim to have no more than about 90 dollars showing as your balance when the statement closes.

- If your limit is 500 dollars, try to stay under about 150 dollars.

This may mean making a small payment mid‑month before the statement date if you have used the card more heavily. This helps reduce the utilization that appears on your credit report, supporting healthier credit over time.

Pay the full statement balance on time, every month

On‑time payments are one of the strongest factors in building credit. Payment history is one of the most important factors in how credit scores are calculated, which is why consistency matters so much. For freelancers with uneven income, this may require planning:

- Use automatic payments from a checking account for at least the statement balance.

- Keep a small buffer in your bank account to cover the card even if a client pays late.

Paying in full avoids interest and keeps the card focused on building credit, not creating debt.

Use the card for predictable monthly expenses

Good candidates include:

- A recurring subscription relevant to your work (design software, writing tools, cloud storage).

- A modest gas or transit budget for a rideshare driver.

- A small, consistent grocery or phone bill portion.

Using predictable expenses makes it easier to keep utilization low and ensure you can pay in full. Avoid using the secured card for large, unpredictable costs like big equipment purchases unless you can immediately pay them off.

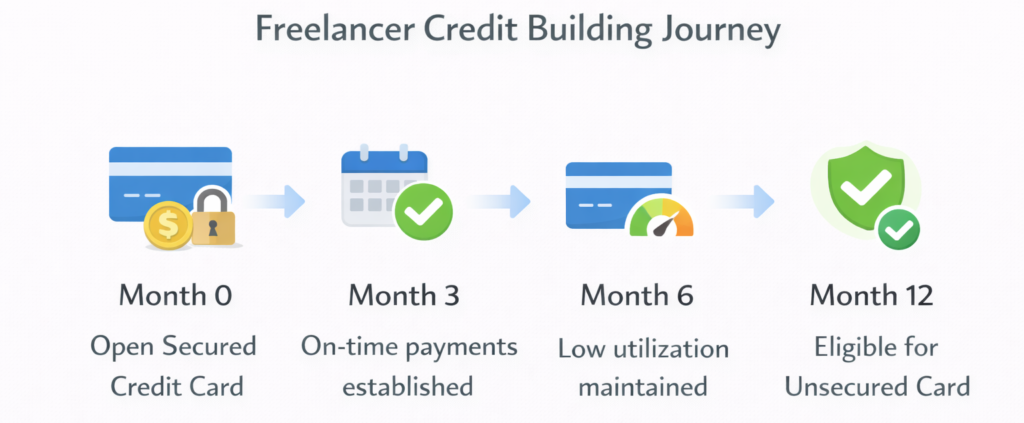

Build at least 6–12 months of positive history

Lenders look for patterns over time. Three months of good behavior helps, but six to twelve months of on‑time payments and low balances provide a much stronger signal that you can handle credit responsibly.

Plan ahead for graduation to an unsecured card

From the beginning, think of your secured card as temporary. As your credit improves, you may:

- Become eligible for an unsecured card with the same issuer, which may convert your secured account and return your deposit.

- Qualify for unsecured cards from other issuers, at which point you can decide whether to keep or close the secured card after your deposit is refunded.

A typical strategic path is:

- Open a secured card with a manageable deposit.

- Use it lightly and pay in full for 6–12 months.

- Check for pre‑qualification offers for unsecured cards.

- Upgrade or switch when you can comfortably move to a no‑deposit card.

Secured vs Unsecured for Freelancers

Both secured and unsecured credit cards for self-employed people can help build credit if used responsibly. The main differences are in how you qualify and how much flexibility you have.

Secured vs Unsecured Cards in the Freelancer Context

| Feature | Secured Card (Freelancer Context) | Unsecured Card (Freelancer Context) |

|---|---|---|

| Deposit required | Yes, cash deposit usually equal to limit | No deposit required |

| Approval difficulty | Easier for thin or damaged credit, even with irregular income | Harder if income is inconsistent or credit history is limited |

| Starting credit limit | Often low, based on deposit | Based on income and credit profile; can be higher |

| Impact on cash flow | Ties up savings in deposit | No deposit, but higher limit can tempt overspending |

| Fees and interest | May be similar or slightly higher than many unsecured options | Wide range; better profiles may get lower costs |

| Best for | New freelancers, recent denials, credit rebuilding | Established freelancers with solid income and credit |

| Credit building effectiveness | Strong if used with low utilization and on-time full payments | Also strong when used responsibly |

| Risk of overspending | Lower limit can naturally cap spending, but easy to hit high utilization | Higher limit increases temptation to overspend |

| Path to future borrowing | Can open the door to unsecured cards after positive history is established | Already positions you for better rates and higher limits if well managed |

Credit Building Timeline for Freelancers

The exact timing of credit improvement varies by person, but freelancers can use a rough timeline to set expectations.

First 3 months

- The new account appears on your credit reports and starts reporting balances and payments.

- As long as you pay on time and keep utilization modest, there may be small early improvements, especially if you had no prior active credit lines.

- At this stage, lenders still see you as new to credit, so major changes are unlikely yet.

3 to 6 months

- A clear payment pattern forms: the card shows multiple cycles of charges and on‑time payments.

- If utilization is consistently low, your profile looks more stable.

- You may begin to see more favorable pre‑qualification offers, especially if you have no other negative items on your reports.

6 to 12 months

- This is often where the secured card does its best work. A full year of on‑time payments and moderate usage sends a strong signal of reliability.

- If you started with absolutely no credit, by this point you may be in a position to qualify for basic unsecured cards, even with freelance income.

- If you were rebuilding from past problems, a year of good behavior will not erase old issues, but it can significantly offset them in the eyes of many lenders.

Throughout this period, remember that:

- Consistent on‑time payments are more important than how fast your income grows.

- Keeping balances low relative to your limit helps show that you are not depending on credit to survive slow months.

Imagine a simple progress chart: a line gradually rising from “Very Limited Credit History” at Month 0 to “Stronger, More Established Credit Profile” by Month 12, with no exact score numbers shown—just steady, step‑by‑step improvement.

Common Mistakes Freelancers Make

Even with the best intentions, freelancers often stumble in similar ways when using secured cards. Avoiding these mistakes can speed up your progress.

- Applying for multiple unsecured cards at once

After getting denied for one card, some freelancers quickly apply for others, hoping something will stick. This can lead to several hard inquiries and more denials, which may slightly hurt approval odds in the short term. A better approach is to step back and consider a secured card instead of repeating the same application pattern. - Using too much of a small credit limit

With a 300‑dollar limit, putting 250 dollars on the card for business supplies feels reasonable, but it looks like heavy usage to the credit system. Regularly maxing out the card, even if you pay it off each month, can slow your credit building. Aim to use a smaller portion of your limit and pay it down before the statement date whenever possible. - Missing payments during low‑income months

Freelancers often have slow seasons. Missing even one payment can seriously damage the very credit you are trying to build. Set up automatic payments for at least the statement balance and keep your recurring charges small enough that you can cover them even in your worst month. - Closing the secured card too early

It is tempting to close the card and get the deposit back after only a few months. But closing too soon may mean you miss out on the strongest benefits of a longer history. In many cases, keeping the card open for at least 12 months gives your credit reports enough time to clearly reflect your new positive habits. - Treating the secured card as extra spending money

A secured card is not a license to spend more; it is a tool to practice disciplined use. Using it to fund large, uncertain business expenses or cover gaps between clients can lead to high balances and interest charges, which work against your long‑term goals.

Frequently Asked Questions

Do secured credit cards work for freelancers?

Yes. Secured credit cards can be especially helpful for freelancers, gig workers, and other self‑employed people who struggle to get approved for unsecured cards. Because the secured deposit lowers the lender’s risk, the approval bar is often lower, even with irregular income or a thin credit file. Used with low utilization and consistent on‑time payments, they can meaningfully support credit building for freelancers.

How much deposit do freelancers usually need?

Deposit requirements vary by issuer, but many secured cards have minimums in the low hundreds of dollars, with maximums that can reach several thousand. Freelancers should choose a deposit amount that:

They can afford to set aside without touching their emergency fund.

Still gives them enough limit to keep utilization relatively low on their planned monthly expenses.

For many beginners, a few hundred dollars is a practical starting point.

Can freelancers qualify for unsecured cards later?

Yes. In fact, that is the main point of using a secured card: to eventually move to unsecured credit once your profile is stronger. After about 6–12 months of responsible use—on‑time payments, modest balances, and no new serious negatives—many freelancers will see better options become available. Some issuers may directly upgrade the secured account; others may require a new application for an unsecured card.

Does irregular income automatically mean rejection?

No. Irregular income on its own does not guarantee rejection, but it does mean lenders pay more attention to credit history and documentation. A freelancer with fluctuating earnings but a solid record of on‑time payments and low debt may still qualify for unsecured cards. For those just starting out or rebuilding, a secured card is often a practical way to prove reliability despite uneven monthly income.

Conclusion

For freelancers, gig workers, and self‑employed people, the traditional credit system can feel unfair. Income comes in waves rather than paychecks, and many are new to credit or recovering from past mistakes. Secured credit cards for freelancers offer a realistic way to bridge that gap: they trade a refundable deposit today for a better chance at credit approval and a structured path to building a positive history.

The key is to see secured cards as stepping stones, not permanent solutions. Used well—low utilization, full payments each month, and steady use over 6–12 months—they can help transform an unpredictable income story into a track record of responsibility that lenders understand and reward. Over time, that opens doors to unsecured cards and other forms of credit without requiring a lifetime of deposits. You can explore more beginner-focused credit education on our homepage.

Ultimately, the specific card type matters less than the habits behind it. Freelancers who approach credit with structure, discipline, and clear limits can build strong financial reputations, even if their income is irregular. A secured card is simply one of the most accessible starting tools to make that happen.

Explore the Complete Credit Card Guide

If you’re comparing secured options and want a broader explanation of how approval works for both gig workers and freelancers in the US, start with our complete guide below:

👉 Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This guide is for educational purposes only and does not provide personalized financial, legal, or tax advice. Credit card approval terms, deposit requirements, fees, and features vary by issuer and by individual financial profile. Freelancers and self‑employed individuals should review specific card terms carefully and consider consulting a qualified professional before making major financial decisions.