Introduction

Many gig workers find that getting approved for a traditional unsecured credit card is harder than expected, even when they are working full time and earning a reasonable amount overall. Lenders are often set up to evaluate people with steady paychecks and predictable pay periods, not drivers, delivery workers, or freelancers whose earnings can swing from week to week. This mismatch can lead to confusing denials or low credit limits, even when the applicant feels their income is strong over the course of the month.

Traditional salaried workers usually have a single employer, fixed pay dates, and standardized income documents such as regular pay stubs, which make it easier for lenders to confirm income and evaluate risk. Gig workers, by contrast, may be paid by the task, by the ride, or per project, with money coming in from multiple platforms or clients and fluctuating significantly from month to month. That irregular pattern makes it more challenging for lenders to judge how reliably the person will be able to make credit card payments.

Because of these obstacles, secured credit cards for gig workers are often suggested as a starting point or fallback option when traditional unsecured cards are hard to get. A secured card requires a cash deposit up front, which functions as collateral and usually sets the credit limit, making lenders more comfortable approving people with thin histories or irregular income.

Used carefully, this kind of card can help build a consistent payment record and demonstrate responsible borrowing behavior over time. For many independent earners, secured credit cards for gig workers become a practical starting point when traditional options are not easily available. If you are completely new to borrowing, it may help to first understand how credit cards work before deciding which option fits your situation.

On This Page

- Introduction

- Why Gig Workers Get Rejected for Unsecured Credit Cards

- What Is a Secured Credit Card? (Simple Explanation)

- When Secured Credit Cards Are a Good Option for Gig Workers

- When Secured Cards Are NOT a Good Option

- Costs and Tradeoffs Gig Workers Should Understand

- Secured vs Unsecured Credit Cards for Gig Workers

- How Secured Cards Help Build Credit for Gig Workers

- Common Mistakes Gig Workers Make

- Final Verdict

- Frequently Asked Questions

- Conclusion

- Looking for the Complete Credit Card Guide?

- Disclaimer

Why Gig Workers Get Rejected for Unsecured Credit Cards

Unsecured cards—those that do not require a deposit—are usually designed for people with established credit profiles and income that can be easily verified. Gig workers often run into several overlapping issues when they apply.

Income documentation challenges

Many lenders still rely heavily on traditional income documents like pay statements from a single employer to verify earnings. Gig workers may instead have app statements, bank deposits from multiple sources, or project invoices, which do not fit neatly into those systems. Irregular income can also make it harder for a lender’s formulas to calculate a stable monthly amount they are comfortable using for approval decisions.

Thin or limited credit history

Some gig workers are new to credit, have mostly used debit cards, or have only one small credit account, leading to a “thin file” with limited information for the lender to evaluate. Others may have had credit difficulties in the past and are trying to rebuild after late payments or collections. In both cases, unsecured cards marketed to people with strong credit may be out of reach, even if the applicant’s current income is reasonable.

Risk perception

Because gig income can rise and fall with demand, location, and schedule, lenders may view these applicants as more likely to miss payments during slow periods, especially if they already carry other debts. This perceived risk can lead to more rejections, lower starting limits, or higher interest rates on any credit that is approved.

Hard inquiries and repeated applications

Each time you apply for a new credit card, the lender usually places a “hard inquiry” on your credit report, which can cause a small, temporary dip in your scores. If a gig worker gets denied several times in a short span and keeps applying, those multiple inquiries can start to add up and make future approvals even more difficult. This is one reason it can be helpful to consider a more realistic option—such as a secured card—before submitting a long string of applications. Each application can result in a hard inquiry, which may temporarily affect your credit profile.

What Is a Secured Credit Card? (Simple Explanation)

A secured credit card is a regular credit card in how it works day to day, but with one key difference: you give the lender a refundable cash deposit before you can use the card. This money is held in a separate account as collateral and is not used to pay your monthly bill; you still have to make payments just as you would with any other credit card.

In most cases, the secured credit card deposit is equal to the credit limit the lender gives you. For example, if you provide a deposit of a few hundred dollars, your starting credit limit is typically the same amount, although some lenders may later raise your limit based on good payment behavior without requiring an additional deposit.

This structure reduces lender risk because, if you stop paying and the account is eventually closed with a remaining balance, the lender can use the deposit to help cover what you owe. Knowing they have this backstop makes many lenders more willing to approve applicants with limited or imperfect credit histories and irregular income patterns. For gig workers, that can translate into a higher chance of approval than with many unsecured options, though approval is never guaranteed.

When Secured Credit Cards Are a Good Option for Gig Workers

Secured credit cards for gig workers tend to work best when the cardholder has clear goals, a realistic budget, and a plan to use the card as a credit‑building tool rather than as extra spending money. Several situations are especially suited to this approach. In these situations, secured credit cards for gig workers offer a structured and lower‑risk way to begin building a positive credit history.

- New to credit: If you have little or no credit history, a secured card can be an entry point that allows you to show lenders how you handle borrowing and repayment

- Recently denied for an unsecured card: If you applied for a standard card and were turned down, stepping back and opening a secured card can be a way to build a stronger profile before trying again.

- Rebuilding after past issues: If you have late payments, charge‑offs, or collections in your past, a well‑managed secured card can demonstrate a fresh pattern of reliable payments over time.

- Able to afford the deposit without hardship: The deposit should be money you can comfortably set aside for a year or more without putting essential bills or emergency savings at risk.

Used in this way, secured credit cards can support credit building for gig workers by creating a steady stream of on‑time payments and low balances that show up on credit reports month after month. If you also earn through freelance projects, you may find our guide on secured credit cards for freelancers helpful.

When a Secured Card Fits a Gig Worker

| Gig Worker Situation | Secured Card Good Fit? | Why |

|---|---|---|

| New to credit, no prior accounts | Often yes | Easier approval, creates first active credit line. |

| Declined for an unsecured card recently | Often yes | Provides a more attainable path to start building history. |

| Past late payments, trying to rebuild | Often yes | Can show new pattern of on‑time payments over time. |

| Income is variable but generally predictable | Sometimes | Works if you can budget for minimum payments consistently. |

| Can tie up a modest deposit comfortably | Often yes | Deposit makes approval more likely and sets your limit. |

When Secured Cards Are NOT a Good Option

Secured cards are not ideal for every gig worker. In some cases, tying up cash in a deposit or taking on new credit responsibilities can create more risk than benefit.

- Extremely unstable income: If your earnings swing so widely that you are not confident you can cover even small minimum payments during slow months, adding any new credit card may increase your risk of missed payments and fees.

- No savings cushion at all: When you are living day‑to‑day with no emergency buffer, locking up a deposit might make it harder to handle essential expenses or unexpected repairs.

- Existing unmanaged debt problems: If you already struggle to keep up with other credit cards, loans, or past‑due bills, adding another account—even a secured one—can complicate things further.

- Already qualify for a solid unsecured card: If your credit is strong enough that you can qualify comfortably for an unsecured card with reasonable terms, there may be little reason to tie up cash in a deposit.

In these situations, secured credit cards for gig workers offer a structured and lower‑risk way to begin building a positive credit history.

Costs and Tradeoffs Gig Workers Should Understand

Before opening a secured card, it is important to understand the financial tradeoffs involved, especially when your income is irregular. Even though secured credit cards for gig workers improve approval chances, they still come with important costs and limitations.

Deposit requirement

The most obvious cost is the secured credit card deposit itself. Many secured cards require at least a few hundred dollars up front, and your credit limit is usually set at or near that amount. While the deposit is typically refundable if the account is closed in good standing or upgraded later, it may be unavailable for everyday use for a year or more.

Low limits and utilization risk

Because limits on secured cards are often modest, it is easy to run up a balance that is high relative to the available limit, especially if you use the card for many gig‑related expenses like fuel or supplies. Credit scoring models pay attention to your “utilization ratio,” the percentage of your available credit that you are using, and higher utilization can be viewed less favorably than lower utilization. With a small limit, you may need to make frequent payments or keep individual purchases modest to help keep that ratio in a healthy range.

Interest and fees

Secured cards usually charge interest on balances that are not paid in full, and their rates can be as high—or sometimes higher—than those on many unsecured cards. Some secured cards may also include annual fees or other charges, which can add to the cost if you keep the card open for several years. For gig workers, who may already face variable expenses from week to week, planning to pay the balance in full each month is often the safest way to avoid interest costs.

Key Cost Factors for Gig Workers

| Cost Factor | What It Means | Why It Matters for Gig Workers |

|---|---|---|

| Security deposit | Cash held as collateral, usually equal to your limit. | Ties up money that could cover slow weeks or emergencies. |

| Low starting credit limit | Limit often only a few hundred dollars. | Easy to hit high utilization if you put many expenses on the card. |

| Interest on carried balance | Interest charged if you do not pay in full. | Irregular income can make revolving balances more expensive. |

| Possible fees | Annual or other fees in some cases. | Reduces the net benefit if the card is kept for only a short time. |

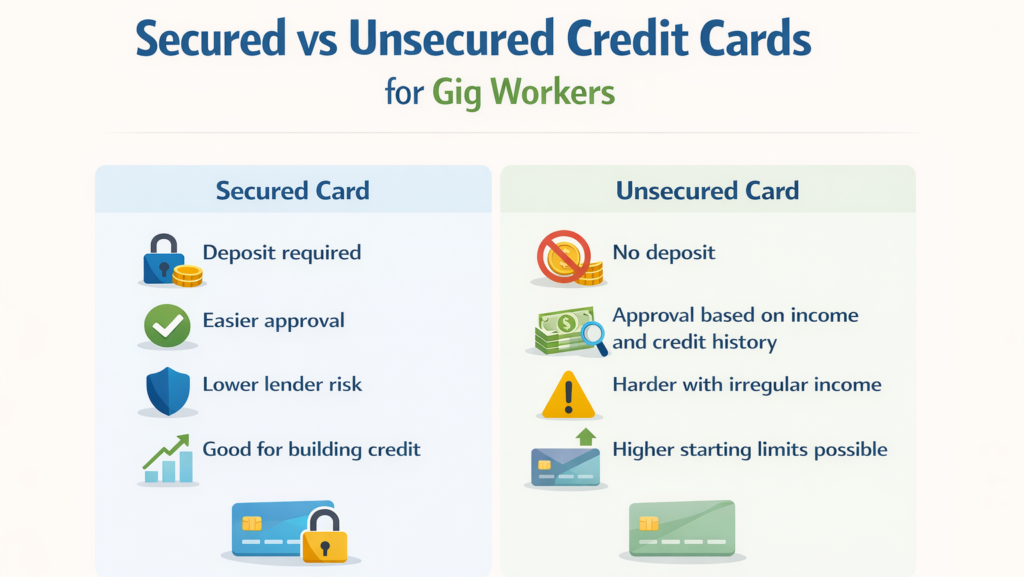

Secured vs Unsecured Credit Cards for Gig Workers

The difference between secured vs unsecured credit cards for gig workers comes down to tradeoffs in approval odds, upfront cost, and long‑term flexibility.

Approval difficulty

Secured cards are generally designed for people with limited or damaged credit, so the approval standards tend to be more flexible than those for many mainstream unsecured cards. Lenders are more comfortable approving these applications because the deposit helps offset their risk. In contrast, unsecured cards aimed at applicants with strong credit often require a well‑established history and income that fits traditional patterns, which can be a barrier for gig worker credit card approval.

Upfront cash requirement

The main downside of secured cards is the need to provide that deposit, sometimes for several hundred dollars or more. Unsecured cards do not require any upfront deposit, which preserves your cash for savings, business expenses, or emergencies. For a gig worker with very limited savings, this difference can be significant.

Long‑term flexibility

Both secured and unsecured cards can help build credit if used responsibly, because the scoring models primarily look at your payment history, utilization, and account age, not whether a card is secured. Over time, many borrowers who handle a secured card well are able to move on to unsecured products, often closing the secured account and getting their deposit back or upgrading to a different type of card. Unsecured cards may offer higher limits and more features sooner, but they can be harder to obtain at the beginning of a gig worker’s credit journey.

Secured vs Unsecured in the Gig Context

| Feature | Secured Card (Gig Context) | Unsecured Card (Gig Context) |

|---|---|---|

| Typical approval difficulty | Often easier with limited or imperfect credit. | Often harder without strong credit and traditional income. |

| Upfront cash requirement | Requires refundable deposit, usually a few hundred dollars. | No deposit required. |

| Starting credit limit | Often modest, based on deposit. | Can be higher, based on credit profile and income. |

| Impact on credit when used well | Can build or rebuild credit over time. | Can build credit as well; card type is not the key factor. |

| Best use case for gig workers | New to credit or rebuilding with some savings for a deposit. | Already have solid credit and reasonably documented earnings. |

How Secured Cards Help Build Credit for Gig Workers

The main reason to consider secured credit cards for gig workers is their potential to support steady, long‑term credit building when used carefully. The card itself is just a tool; how you use it is what shows up on your credit reports.

On‑time payments

The single most important factor in most credit scoring models is whether you pay your bills on time. With a secured card, each on‑time payment you make is typically reported to the major credit reporting agencies, just as with an unsecured card. For gig workers, this means that even if income is uneven, consistently paying at least the minimum by the due date can gradually build a record of reliability.

Utilization management

Another major factor is how much of your available credit you use relative to your limits. On a small secured card limit, using most of your available credit can make your utilization appear high, even if the dollar amount is modest. Making several smaller payments throughout the month or keeping purchases limited to predictable essentials (such as one recurring bill) can help keep utilization in a more favorable range.

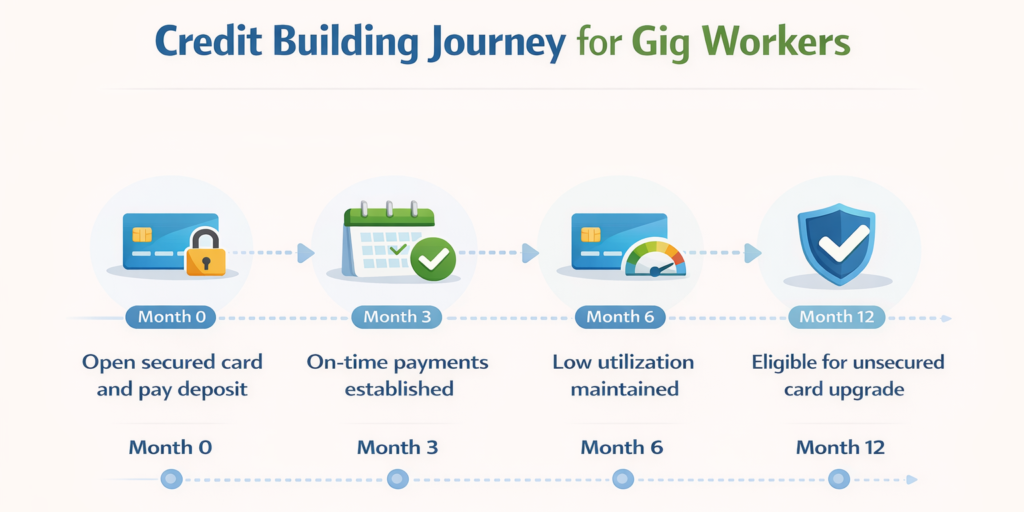

Building history over 6–12 months and beyond

Over time, months of on‑time payments and controlled balances can make your credit reports look very different from where they started. Many people use a secured card for roughly six to twelve months before checking whether their credit profile has improved enough to qualify for better options or to request an upgrade. While there is no fixed timeline and results vary by individual, this period is often enough to show a clear pattern of responsible use, which is what lenders want to see.

Common Mistakes Gig Workers Make

Secured cards can help, but they can also backfire if used carelessly. Some pitfalls are especially common among gig workers.

- Overusing small limits: Charging too many expenses on a small limit can quickly push utilization higher than is ideal, even if you plan to pay it off eventually.

- Missing payments during slow weeks: When income dips, it is tempting to delay or skip a payment; even one late payment can significantly undermine the credit‑building progress you have made.

- Closing the secured card too early: Shutting down the account after only a few months may reduce the long‑term benefit, since lenders like to see stable, ongoing accounts.

- Applying for multiple unsecured cards too soon: After a short period of improvement, some people apply for several unsecured cards at once; the resulting hard inquiries and possible denials can slow or reverse the progress they achieved.

Avoiding these mistakes usually comes down to planning for variability—building a small payment buffer when income is strong and keeping card use intentionally modest.

Final Verdict

Secured credit cards for gig workers can be a smart option when used carefully and with realistic expectations. secured credit cards can be a useful, structured way to begin or restart a credit journey, as long as the card is treated as a tool for building history rather than a source of extra spending money. They are often most appropriate when you have some savings for a deposit, are comfortable budgeting for regular payments, and are focused on long‑term financial access rather than short‑term rewards.

On the other hand, if your income is extremely unstable, you have no cushion at all, or you already qualify for reasonable unsecured options, a secured card may not be the best fit right now. In those situations, stabilizing earnings, building basic savings, or improving existing accounts may provide more benefit than tying up cash in a new deposit. The right answer depends less on the label “secured” or “unsecured” and more on whether you can use the card consistently, pay on time, and avoid carrying costly balances.

Frequently Asked Questions

Do secured credit cards work for gig workers?

Yes, secured credit cards for gig workers can support credit building when you make payments on time and keep balances low, just as they do for salaried workers. Lenders generally treat a well‑managed secured card similarly to an unsecured card when it comes to credit reporting and scoring. That is why secured credit cards for gig workers are commonly recommended as a starter tool.

How much deposit is required?

Many secured cards ask for a refundable deposit in the range of a few hundred dollars, and your credit limit is usually set equal to that deposit. Some lenders allow larger deposits, which can increase your limit, while others may later raise your limit based on strong payment history.

Can gig workers upgrade later?

In many cases, if you use the card responsibly for a period of time—often several months to a year—lenders may allow you to move to an unsecured card or close the secured card and return your deposit, though policies vary. The key is demonstrating consistent on‑time payments and controlled use of your available credit.

Does irregular income mean automatic rejection?

Irregular income does not automatically mean rejection, but it can make approval harder, especially for unsecured cards that rely on traditional income documentation. A secured card can sometimes improve your chances because the deposit reduces lender risk, but approval still depends on your full profile, including credit history and existing obligations.

Conclusion

For gig workers, income type often makes traditional applications more complicated, but it does not have to block access to credit entirely. Secured cards are tools, not shortcuts, and they work best when paired with careful planning, conservative spending, and a clear focus on long‑term financial health.

Over time, lenders tend to care more about how you handle the obligations you already have than about the specific way you earn your income. Whether you drive, deliver, or freelance, consistent on‑time payments and mindful use of your available credit can gradually open up more options, regardless of where you started. For more beginner‑friendly credit education guides, explore our full resource library.

Looking for the Complete Credit Card Guide?

If you want a broader explanation of how secured and unsecured credit cards work for gig workers and freelancers in the US, read our complete guide below:

👉 Complete Guide to Credit Cards for Gig Workers and Freelancers in the US

Disclaimer

This article is for general educational purposes only and is not financial, legal, or tax advice. Individual situations vary, and terms for any credit product depend on the specific lender and your personal financial profile. Before applying for or opening any credit account, consider reviewing the full terms and, if needed, consulting a qualified professional.