Introduction

Freelancers face a unique problem when it comes to credit cards: their work is a business, but their finances often run through personal accounts. That makes the choice between a personal vs business credit card for freelancers more confusing than it looks on the surface.

The line between “personal” and “business” expenses is blurry when you use the same phone, laptop, and internet connection for both work and life. Yet the card you choose affects how organized your taxes are, how your credit profile develops, and how likely you are to be approved in the first place. For a broader breakdown of approval structures and income considerations, you can review our complete guide to credit cards for gig workers and freelancers.

This guide walks through the structural differences between a business credit card for freelancers and a personal credit card for self-employed people, how lenders look at your income, and practical scenarios where one option may fit better than the other. The goal is not to push you toward a specific product, but to help you make a clear freelancer credit card choice based on how you earn, spend, and manage risk. choosing the right structure starts with understanding the personal vs business credit card for freelancers decision in practical terms.

On This Page

- Introduction

- What Is a Personal Credit Card?

- What Is a Business Credit Card?

- 7 Key Differences Freelancers Must Understand

- Secured vs Unsecured in Personal and Business Context

- How Lenders Evaluate Freelance Income

- When Freelancers Should Choose a Personal Credit Card

- When Freelancers Should Choose a Business Credit Card

- Can Freelancers Use Both Strategically?

- Common Mistakes Freelancers Make

- Frequently Asked Questions

- Final Recommendation

- Conclusion

- Disclaimer

What Is a Personal Credit Card?

A personal credit card is built around you as an individual, not around your freelance business. It is approved primarily based on your personal credit history, your stated income, and your existing obligations such as other loans or cards. You typically apply using your name, Social Security number, home address, and an estimate of your total individual income from all sources.

Once the card is open, almost all activity is reported to your personal credit file with the major consumer credit bureaus. That means your payment history, balance levels, and how close you are to the limit on that card can influence your overall credit profile. Late payments, going over the limit, or letting a balance grow too large relative to your limit can all work against you over time.

Personal cards also affect how lenders view your debt-to-income ratio, which compares what you owe each month to how much you earn. The higher that ratio, the riskier you may look when you apply for new credit, even if you have never missed a payment. Large revolving balances on personal cards can therefore make it harder to qualify for additional loans or lines of credit, especially if your freelance income is irregular.

For new freelancers, personal cards are often simpler to get because the approval process is familiar and does not require a long documented business history. You can typically qualify based on your own credit record and income, even if your freelance work is new, part-time, or still building up. That makes a personal card a common starting point for early-stage self-employed professionals and gig workers.

What Is a Business Credit Card?

A business credit card is designed to handle expenses tied to a trade or business activity, even if that “business” is just you working as an independent contractor or gig worker. You usually apply in the name of your business (even if that is simply your own name as a sole proprietor), and you may be asked for both your personal information and basic business details such as industry, years in operation, and estimated annual revenue.

For many freelancers operating as sole proprietors, the application will use a Social Security number and a business name, and approval will still rely heavily on your personal credit record. Some more established businesses may use a separate business tax ID number instead, but most solo freelancers qualify using their personal information and a simple description of their work.

A key concept with many small-business cards is the “personal guarantee.” This means that even though the card is branded for business use, you personally agree to repay the debt if the business cannot. From the lender’s point of view, this reduces risk, because they can still pursue you personally for repayment if the business cash flow dries up.

Reporting is where business vs personal credit card differences become more complex. Some business cards report activity only to business credit files, while others also report to your personal credit file or at least report serious delinquencies there. As a freelancer, that means a business card might or might not affect your personal utilization rates and personal score, depending on how the issuer handles reporting.

High-Level Feature Comparison

| Feature | Personal Credit Card | Business Credit Card |

|---|---|---|

| Primary purpose | Personal and household spending | Business and income-producing expenses |

| Application focus | Personal credit and income | Personal plus basic business information |

| Typical identifier used | Social Security number | Social Security or business tax ID |

| Who guarantees repayment | You, personally | You, personally, in most freelancer cases |

| Where activity is reported | Personal credit file | Business file, and sometimes personal file |

| Intended expense separation | Mixed or personal use | Separate, business-only spending |

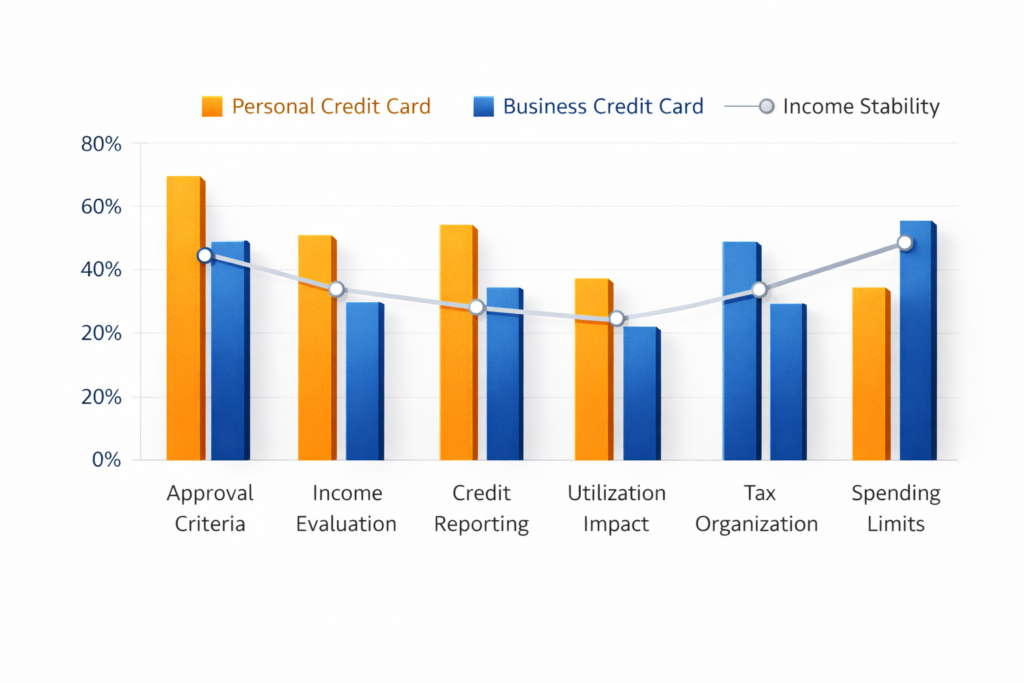

7 Key Differences Freelancers Must Understand

While personal and business cards both allow you to borrow and repay over time, they behave differently in ways that matter a lot for freelancers. Understanding these structural differences helps you match the card type to your current stage of self-employment. To properly evaluate the personal vs business credit card for freelancers debate, you need to understand how these two structures behave differently over time.

1. Approval Criteria

Personal cards typically look mainly at your personal credit history, stated income, and existing obligations. Business cards for freelancers often use that same personal profile, but also consider basic information about your freelance activity such as revenue estimates and time in business.

2. Income Evaluation

For freelancers, income can fluctuate, which makes evaluation less straightforward than for a salaried employee. Lenders may look at your average earnings over a period of time or consider multiple income streams together when reviewing your application.

3. Credit Reporting

Most personal cards report full activity to your personal credit file every month, including balances and payment history. Business cards might report only to business credit files, or report limited information to personal files unless there is a serious default. Most personal cards report activity through the consumer credit reporting system, which shapes how your payment history and balances affect your overall credit profile.

4. Utilization Impact

Because personal cards almost always show up on your personal reports, high balances can raise your overall utilization ratio, which is a key factor in many scoring models. Business cards that do not report regular balances to personal files can keep some utilization “off” your personal profile, although missed payments or collections can still appear.

5. Tax Organization

Using a personal card for mixed expenses forces you to sort out which charges were business-related at tax time, which can be time-consuming and error-prone. A dedicated business card can keep all work-related spending in one place, making it easier to track deductible expenses and support your tax records.

6. Legal Liability

With a personal card, the liability is clearly yours as an individual. With many freelancer-oriented business cards, the liability is effectively the same because of the personal guarantee, even though the card is used for business expenses.

7. Spending Limits

Business cards often come with higher potential credit limits to support larger project expenses, inventory purchases, or advertising campaigns. Personal cards may offer lower limits, especially early in your credit journey, which can constrain how much business spending you can comfortably place on them.

Key Factors and What They Mean for Freelancers

| Factor | Personal Card | Business Card | What It Means for Freelancers |

|---|---|---|---|

| Approval criteria | Personal credit and income | Personal credit plus basic business details | New freelancers may find personal cards easier, but simple freelance info often qualifies for business cards too. |

| Income evaluation | Total household or individual income stated | Personal income plus business revenue estimates | Irregular freelance income may be averaged or combined across gigs. |

| Credit reporting | Reports fully to personal file | Often to business file; sometimes to personal file | Some business cards keep routine activity separate from personal reports. |

| Utilization impact | Directly affects personal utilization ratio | May or may not affect personal utilization | Business cards can sometimes reduce pressure on personal utilization. |

| Tax organization | Mixed personal and business charges on one card | Business expenses concentrated on one account | Easier bookkeeping and documentation with a dedicated business card. |

| Legal liability | You personally owe the balance | You usually owe personally via guarantee | Card type does not eliminate personal responsibility for repayment. |

| Spending limits | Often lower, tied to personal profile | Often higher, built for business-level expenses | Growing freelancers may appreciate higher limits for project cash flow. |

Secured vs Unsecured in Personal and Business Context

Both personal and business cards can be either secured or unsecured. Secured cards require you to place a refundable cash deposit as collateral, which usually becomes your starting credit limit. Unsecured cards do not require a deposit and instead rely fully on your credit profile and income to set your limit.

For a freelancer with thin or damaged credit, a secured personal card can be a practical way to establish or rebuild a track record of on-time payments. Because the lender holds your deposit, approval may be more accessible, even if you have a short history or past mistakes. Used carefully, this can create a foundation that eventually supports better terms on other credit products.

Secured business cards exist as well, though they are less common. They may be useful if your freelance business has meaningful expenses but your personal credit is not yet strong enough for a standard unsecured business card. In that case, the deposit helps the lender manage risk while you demonstrate responsible use through your business spending.use.

The main trade-off with secured cards is tying up cash that could otherwise support your operations or emergency fund. On the other hand, an unsecured card exposes the lender to more risk, which can lead to stricter approval standards and lower starting limits if your profile is still developing. From a risk perspective, both secured and unsecured cards can harm your credit if mismanaged, but secured products may offer a gentler entry point for cautious, rebuilding freelancers. If you are rebuilding credit or need a lower-risk entry point, our detailed guide on secured credit cards for freelancers explains how deposits and approval criteria typically work.

How Lenders Evaluate Freelance Income

Freelance income is often uneven from month to month, so lenders rarely look at just a single recent deposit when deciding on approval. Instead, they tend to consider averages over time, along with the overall stability of your work and obligations. Lenders often rely on self-employed income documentation requirements when reviewing freelance earnings and verifying reported income. Freelancers with fluctuating monthly earnings may also benefit from reviewing the best credit cards for gig workers with variable income to understand which card types are more flexible with approval.

A common approach is income averaging, where the lender looks at your net profit over a one- or two-year period to estimate a sustainable monthly figure. For many self-employed applicants, that number is based on tax documents that summarize business income and expenses for the year. In some cases, lenders may also review bank statements to confirm that funds are actually flowing into your accounts in a pattern consistent with what you report.

Risk assessment goes beyond income alone. Lenders also look at your existing monthly debt payments relative to your income, which forms your debt-to-income ratio. A high ratio signals that a large portion of your earnings already goes toward debt service, which may make new borrowing less attractive from the lender’s perspective. They also weigh your credit history, including how reliably you have paid other obligations and whether any accounts have gone delinquent.

For freelancers, the key takeaway is that honesty and documentation matter more than trying to guess an “ideal” number. Clear records of invoices, deposits, and tax filings help show that your business is real and that your income, while variable, has a reasonable track record. Over time, consistent behavior on both personal and business credit accounts can reduce the risk perception attached to your self-employed status.

When Freelancers Should Choose a Personal Credit Card

There are many situations where a personal credit card for self-employed individuals is the more practical choice, at least initially. If you have just started freelancing and your income is still low or irregular, personal cards often offer a simpler approval path than business products.chase+1

A personal card can be a good fit if:

- Your freelance work is a side activity and most of your income still comes from wages or salary.

- Your monthly business expenses are modest, such as software subscriptions, occasional equipment, or small marketing costs.

- You are still figuring out whether your current freelance line of work will be long-term.

In these cases, the priority is often building or maintaining a strong personal credit history with manageable limits and clear repayment habits. You can still use a personal card for some business expenses, but you should keep good records and consider tagging those charges in your budgeting or accounting system to simplify tax preparation later.

For freelancers with very irregular income, a personal card can also feel more flexible because approval is not tied to formal business documents or a long operating history. As long as you keep balances low relative to your limit and pay on time, a single well-managed personal card can serve both your everyday life and your early-stage freelance needs.

When Freelancers Should Choose a Business Credit Card

As your freelance revenue grows and your expenses become more clearly business-related, a business credit card for freelancers can become the better structural fit. This is especially true if you regularly pay for advertising, specialized software, travel for client work, or subcontractor payments on your card. This is where the personal vs business credit card for freelancers decision becomes more strategic rather than simply practical.

A business card often makes sense when:

- You have consistent freelance income and expect the business to continue or expand.

- You want a clear separation between business and personal expenses for bookkeeping and tax purposes.

- Your monthly business spending is high enough that it strains the limits on your personal card.

- You are interested in building a distinct business credit profile over time.

Using a dedicated business card can simplify your books by collecting all work-related charges in one place, which is helpful when you or your tax professional prepare returns or financial statements. It can also keep some utilization off your personal reports if the card does not regularly report balances there, which may give you more breathing room on your personal credit profile.

Over the long term, responsible use of a business card—on-time payments, controlled balances, and stable activity—can help your business qualify for larger financing options, such as business lines of credit or installment loans. That can be valuable if you ever need to invest in equipment, expansion, or larger projects that go beyond what a single card can handle.

Can Freelancers Use Both Strategically?

Many established freelancers eventually use both personal and business cards together, each playing a distinct role in their financial system. Done thoughtfully, this separation strategy can improve organization, reduce risk, and support long-term credit building.

One common approach is to route all clearly deductible business expenses through a business card, while keeping personal and household spending on one or two personal cards. That creates a natural dividing line for bookkeeping and reduces the chance that you accidentally claim personal purchases as business deductions.

From a risk management standpoint, multiple cards allow you to spread utilization across several limits instead of concentrating it on one account. For example, you might keep your personal card balance low most of the time, while allowing your business card balance to rise temporarily during a project, then paying it down once a client pays an invoice. Over time, this framework can help you build both personal and business credit histories without overextending yourself on either side.

Scenarios and Best-Fit Card Types

| Scenario | Best Card Type (Often) | Why It Tends to Fit |

|---|---|---|

| New freelancer, low predictable income | Personal card | Simpler approval, relies mainly on personal credit and income. |

| Side gig with modest monthly expenses | Personal card (with tracking) | One card is manageable; tagging business charges can work fine. |

| Full-time freelancer with growing revenue | Business card | Clear separation and higher limits support business operations. |

| Freelance plus larger project-based spending | Business card plus personal | Business card handles project costs; personal card covers life expenses. |

| Rebuilding credit while freelancing | Secured personal, then business | Secured card establishes history; business card added once stable. |

Common Mistakes Freelancers Make

Because freelancers live at the intersection of personal and business finance, it is easy to make credit card mistakes without realizing it. Understanding these pitfalls can help you avoid setbacks that slow down your progress or create unnecessary risk.

One frequent mistake is mixing expenses randomly across multiple cards, with some client-related costs on a personal card and some personal spending on a business card. This makes it hard to prove which charges were truly business-related and can complicate tax documentation. Another misconception is assuming that business cards never affect personal credit; while some do not report regular activity, many still involve a personal guarantee and can show up on your personal file if payments are late.

Overstating or guessing your income on applications is another risk. Lenders may attempt to verify your figures through tax returns or bank statements, and inconsistencies can lead to denials or requests for more documentation. Finally, applying for many cards in a short period—especially when income is unstable—can send a signal of financial stress, which may reduce approval odds or lead to smaller limits.

Freelancer Mistakes, Why They Hurt, and Better Strategies

| Mistake | Why It Hurts | Better Strategy |

|---|---|---|

| Mixing personal and business expenses | Confuses tax records and weakens documentation of deductions. | Use one dedicated card for business and track charges clearly. |

| Assuming business cards never touch personal credit | Serious delinquencies can still harm your personal file. | Read terms, understand reporting, and treat all cards as your responsibility. |

| Overestimating or guessing income | Inconsistent information can trigger denials or extra scrutiny. | Use realistic, supportable income figures based on records. |

| Applying for too many cards quickly | Multiple inquiries suggest higher risk or urgent need for credit. | Space out applications and focus on managing existing accounts well. |

Frequently Asked Questions

Can freelancers qualify for business credit cards without formal registration?

Yes, many freelancers, independent contractors, and gig workers qualify for business cards as sole proprietors without forming a separate legal entity. You may be asked for your legal name as the business name, a description of what you do, and an estimate of your business revenue, along with your personal information.

Does a business card affect personal credit?

It can. In many cases, applying for a business card creates a hard inquiry on your personal credit file, and serious delinquencies on that business account may also appear on your personal reports. Some business cards additionally report regular balances and payment history to personal files, while others report only to business files, so the exact impact depends on the issuer’s reporting policies.

Is a personal card safer for irregular income?

A personal card may feel more predictable for freelancers with very uneven cash flow, because approval is based mainly on your overall personal situation rather than a detailed business history. However, “safer” really depends on how you use the card: keeping balances manageable, paying on time, and planning around slow months are more important than whether the plastic is labeled personal or business.

How much income is typically needed?

How much income is typically needed?

There is no single income number that guarantees approval for either personal or business cards. Lenders generally look at your overall profile—credit history, existing debts, and stability of income—rather than setting a universal cutoff, especially for self-employed applicants. Being able to document your earnings and show consistent deposits over time is often more important than the exact dollar amount.

Final Recommendation

For most freelancers, the personal vs business credit card for freelancers decision is not one-time and permanent. It is a progression. Many start with a personal card, move to a business card as income and expenses grow, and eventually use both in a disciplined way.

If you are early in your self-employment journey, with modest, variable income and simple expenses, starting with a personal card and strong habits is more important than rushing into a business product. Focus on paying on time, keeping utilization reasonable, and documenting which expenses are business-related. As your revenue stabilizes, your projects become larger, and your bookkeeping needs become more complex, adding a business card can help you separate expenses, access higher limits, and begin building a business credit profile.

Whichever path you take, your day-to-day behavior matters far more than the label on the card. Responsible use, realistic applications, thoughtful separation of expenses, and careful tracking will do more to protect your finances than any particular product feature.

Conclusion

Credit card approval is ultimately about risk, not job titles. Being a freelancer does not automatically disqualify you, but it can make lenders look more closely at your income stability, existing obligations, and track record. By understanding how personal and business cards work, you can choose tools that match your current stage rather than trying to force your finances into a structure that does not fit.

Freelancers who build habits of structure and discipline—separating expenses, keeping records, and staying within realistic limits—can absolutely build strong credit over time. With the right setup, your cards become a support system for your work, not a source of anxiety. In the end, the personal vs business credit card for freelancers choice is about aligning your credit structure with how your freelance income actually works. For more in-depth education on approval rules, credit structures, and freelancer-focused card strategies, explore UncoverCards for additional guides.

Disclaimer

This article is for educational purposes only and is not financial, legal, or tax advice. Individual situations vary, and card approval decisions are made by each issuer based on its own criteria. Before making decisions about credit cards, taxes, or legal structures, consider speaking with qualified professionals familiar with your personal circumstances.